I am attempting to forecast percentage of churn. However, I am running into issues. The churn is fairly stable except at each year anniversary point.

For example, data looks like this for the first year

Month 9: 1.013770726

Month 10: 1.013770726

Month 11: 1.015761766

Month 12: 0.72113357 #big drop in first year

The next year looks fairly stable except the 2nd anniversary point:

Month 21: 0.7765050878

Month 22: 0.7844692491

Month 23: 0.7884513297

Month 24: 0.4732490503

I thought about simple exponential smoothing model or a simple weighted average. That will help me with normal months but not the expected large drop each year point.

I also tried an arima. That helped with the seasonal drop but well under-forecasted all the other months.

Is there an another option that is obvious that I am not considering?

Here is the completed data set

month churn

2016-09-01 0.9854712144

2016-10-01 1.000828964

2016-11-01 1.000828964

2016-12-01 1.000828964

2017-01-01 1.004811044

2017-02-01 1.006802085

2017-03-01 1.006802085

2017-04-01 1.009788645

2017-05-01 1.009788645

2017-06-01 1.013770726

2017-07-01 1.013770726

2017-08-01 1.015761766

2017-09-01 0.72113357

2017-10-01 0.7300932514

2017-11-01 0.7346932411

2017-12-01 0.7406663621

2018-01-01 0.7565946846

2018-02-01 0.7585857249

2018-03-01 0.7625678056

2018-04-01 0.7685409265

2018-05-01 0.7725230072

2018-06-01 0.7765050878

2018-07-01 0.7844692491

2018-08-01 0.7884513297

2018-09-01 0.4732490503

2018-10-01 0.4890469254

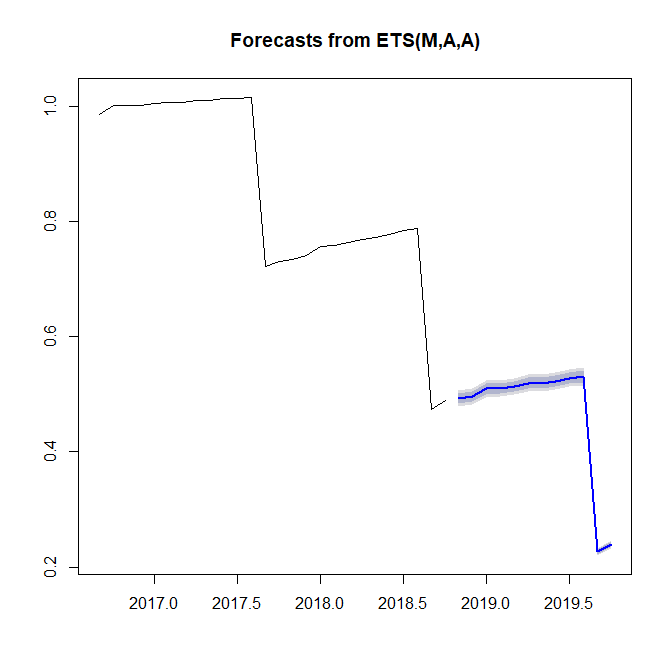

ets()in theforecastpackage for R? It might make sense to work on logged data, given that your data are percentages, i.e., multiplicative. It would be good if you could post a complete time series you want to forecast, not just a few months. $\endgroup$