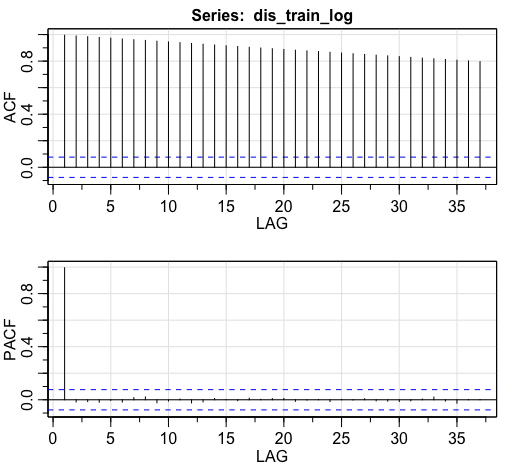

I am trying to find the correct ARIMA model for a time series without seasonality that produce the following ACF and PACF plots.

Looking at these plots my initial hypothesis is that an ARIMA(1,0,0) model is required due to the PACF dropping to 0 after lag 1, but the ACF is decaying too slowly for me to be sure about it.