No, Bessel's correction is not required for the sample mean

The reason Bessel's correction is required for the sample variance is that estimation of the variance also requires us to use the sample mean to estimate the true mean (around which this variance is formed). This is evident when we compare the the differences in the formulae for the sample variance versus the true varriance (see the little arrows in the following formulae for the relevant difference here):

$$s^2 = \frac{1}{n-1} \sum_{i=1}^n (X_i - \underset{\uparrow}{\bar{X}_n})^2

\quad \quad \quad

\mathbb{V}(X) = \mathbb{E}[(X-\underset{\uparrow}{\mathbb{E}(X)})^2].$$

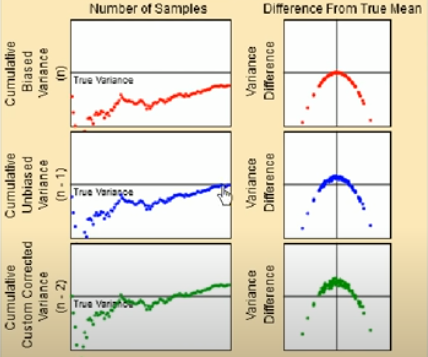

Observe that in the sample variance estimator, the true mean around which the variance is formed is estimated with the sample mean $\bar{X}_n$. The sample mean will tend to be closer to the middle of the data values than the true mean, so the squared deviations of the data values from the sample mean will tend to be smaller than the squared deviations from the true mean ---i.e., we have:

$$\sum_{i=1}^n (X_i - \bar{X}_n)^2 \leqslant \sum_{i=1}^n (X_i - \mathbb{E}(X))^2.$$

(In most actual data sets, this inequality is strict, but it is possible that the sample mean is equal to the true mean, in which case they are equal.) This means that taking a straight average will tend to underestimate the true variance. Bessel's correction accounts for this, and gives a sample variance that is an unbiased estimator of the true variance.