I am looking for methods to detect univariate contextual outliers in time series data. One example application is data from industrial plants in different (unknown) operation modes or slow trends or shifts but no seasonal effects.

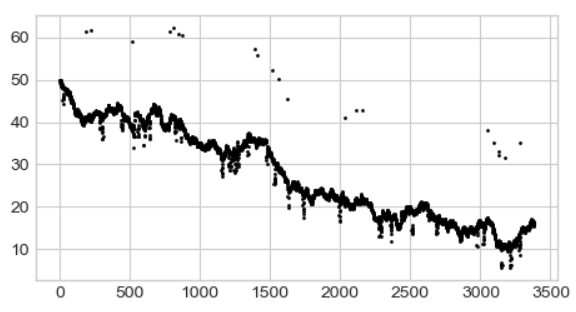

In the following graph visually the contextual outliers above and below the trend can be identified clearly.

Most global outlier detection methods can be used with a sliding window approach. But a method, that automatically derives the optimal window size from the data or even provides an adaptive window size would be beneficial.