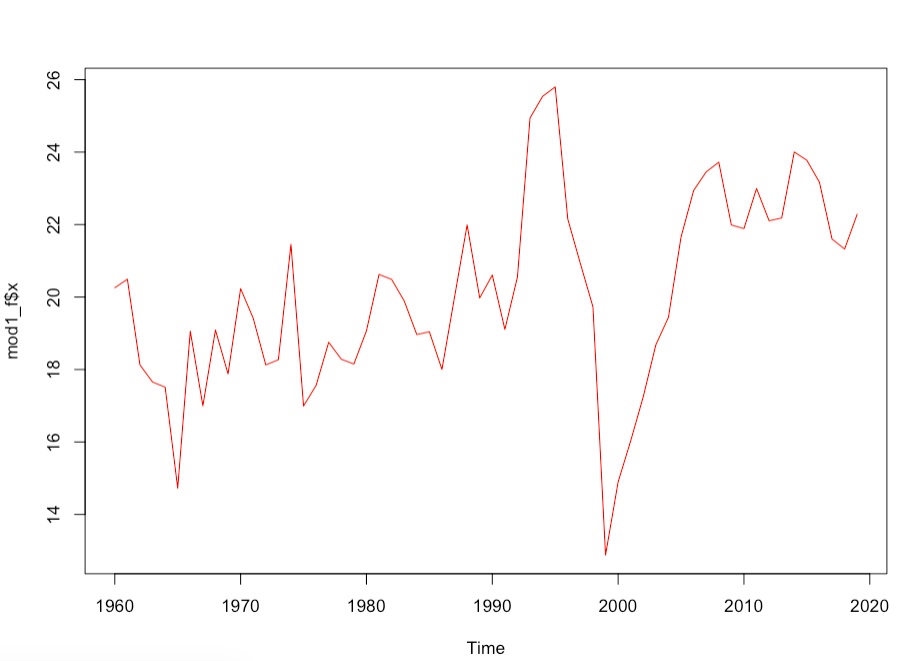

I estimated an AR(1) process, my data looks like this:

Making usual unit root test, they suggest that an estimated AR(1) from this data is stationary. Estimating the AR(1) over this data, these are the results:

z test of coefficients:

Estimate Std. Error z value Pr(>|z|)

ar1 0.728652 0.085601 8.5121 < 2.2e-16 ***

intercept 20.176618 0.809543 24.9235 < 2.2e-16 ***

The purpose of this estimation is to get the stationary mean of the process, i.e.:

$x_t=c+\phi x_{t-1}+\varepsilon_t$

$E\{x_t\}=\frac{c}{1-\phi}$

With the estimated values this turns out to be, given the significance of estimators:

$E\{x_t\}=\frac{20.176618}{1-0.728652}\approx74.3569$

Which clearly is outside the range the values data take, and is much larger than expected. What is wrong? Maybe I misinterpreted the unit root tests or something similar?

arima()fromstatspackage, and also checked withArima()fromforecast, do you know if those have the mentioned by you representation? Also if that's the case, then $\hat\mu=20.176618$? $\endgroup$