I'm a bit confused about the definition of weakly stationarity

from looking at the definition of weakly stationarity, it requires: E(xt) = E(xt−j ) = µ ∀ j var(xt) = var(xt−j ) = σ^2 ∀ j cov(xt, xt−j ) = γj ∀ t

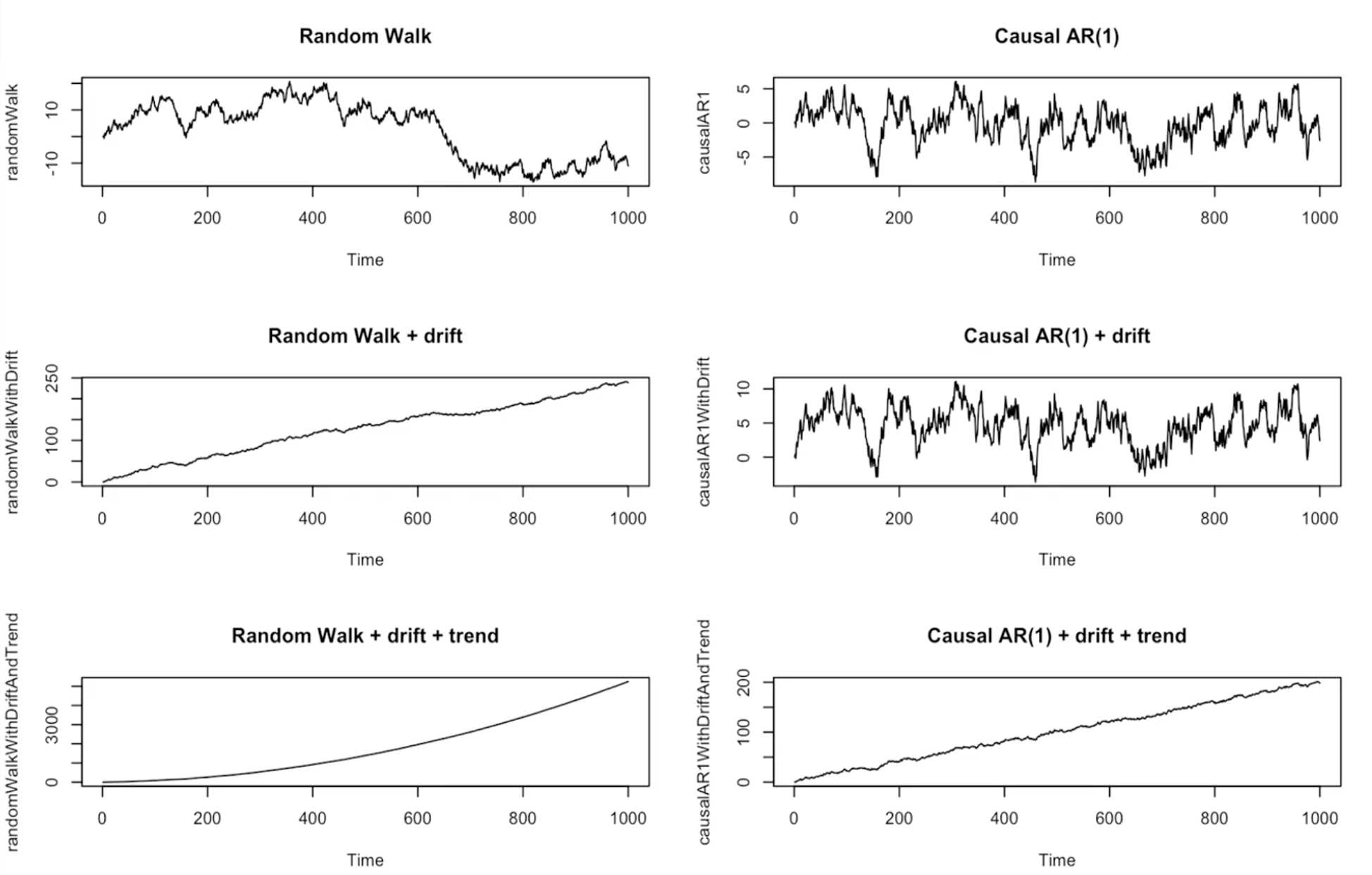

But from looking at the graph of causal AR(1) + drift + trend,

I don't think the E(xt) is constant (mean is increasing as t increases),

also the variance is not constant from the graph,

so why is causal AR(1) + drift + trend weakly stationary?