(Because this is approach is independent of the other solutions posted, including one that I have posted, I'm offering it as a separate response).

You can compute the exact distribution in seconds (or less) provided the sum of the p's is small.

We have already seen suggestions that the distribution might approximately be Gaussian (under some scenarios) or Poisson (under other scenarios). Either way, we know its mean $\mu$ is the sum of the $p_i$ and its variance $\sigma^2$ is the sum of $p_i(1-p_i)$. Therefore the distribution will be concentrated within a few standard deviations of its mean, say $z$ SDs with $z$ between 4 and 6 or thereabouts. Therefore we need only compute the probability that the sum $X$ equals (an integer) $k$ for $k = \mu - z \sigma$ through $k = \mu + z \sigma$. When most of the $p_i$ are small, $\sigma^2$ is approximately equal to (but slightly less than) $\mu$, so to be conservative we can do the computation for $k$ in the interval $[\mu - z \sqrt{\mu}, \mu + z \sqrt{\mu}]$. For example, when the sum of the $p_i$ equals $9$ and choosing $z = 6$ in order to cover the tails well, we would need the computation to cover $k$ in $[9 - 6 \sqrt{9}, 9 + 6 \sqrt{9}]$ = $[0, 27]$, which is just 28 values.

The distribution is computed recursively. Let $f_i$ be the distribution of the sum of the first $i$ of these Bernoulli variables. For any $j$ from $0$ through $i+1$, the sum of the first $i+1$ variables can equal $j$ in two mutually exclusive ways: the sum of the first $i$ variables equals $j$ and the $i+1^\text{st}$ is $0$ or else the sum of the first $i$ variables equals $j-1$ and the $i+1^\text{st}$ is $1$. Therefore

$$f_{i+1}(j) = f_i(j)(1 - p_{i+1}) + f_i(j-1) p_{i+1}.$$

We only need to carry out this computation for integral $j$ in the interval from $\max(0, \mu - z \sqrt{\mu})$ to $\mu + z \sqrt{\mu}.$

When most of the $p_i$ are tiny (but the $1 - p_i$ are still distinguishable from $1$ with reasonable precision), this approach is not plagued with the huge accumulation of floating point roundoff errors used in the solution I previously posted. Therefore, extended-precision computation is not required. For example, a double-precision calculation for an array of $2^{16}$ probabilities $p_i = 1/(i+1)$ ($\mu = 10.6676$, requiring calculations for probabilities of sums between $0$ and $31$) took 0.1 seconds with Mathematica 8 and 1-2 seconds with Excel 2002 (both obtained the same answers). Repeating it with quadruple precision (in Mathematica) took about 2 seconds but did not change any answer by more than $3 \times 10^{-15}$. Terminating the distribution at $z = 6$ SDs into the upper tail lost only $3.6 \times 10^{-8}$ of the total probability.

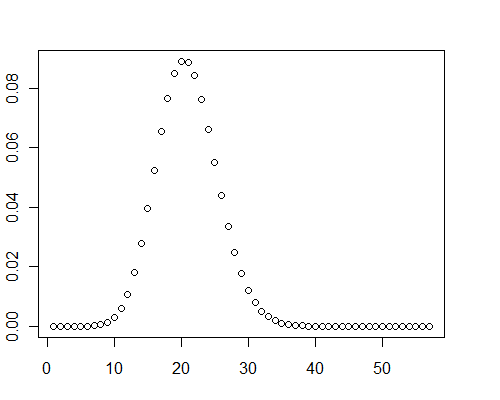

Another calculation for an array of 40,000 double precision random values between 0 and 0.001 ($\mu = 19.9093$) took 0.08 seconds with Mathematica.

This algorithm is parallelizable. Just break the set of $p_i$ into disjoint subsets of approximately equal size, one per processor. Compute the distribution for each subset, then convolve the results (using FFT if you like, although this speedup is probably unnecessary) to obtain the full answer. This makes it practical to use even when $\mu$ gets large, when you need to look far out into the tails ($z$ large), and/or $n$ is large.

The timing for an array of $n$ variables with $m$ processors scales as $O(n(\mu + z \sqrt{\mu})/m)$. Mathematica's speed is on the order of a million per second. For example, with $m = 1$ processor, $n = 20000$ variates, a total probability of $\mu = 100$, and going out to $z = 6$ standard deviations into the upper tail, $n(\mu + z \sqrt{\mu})/m = 3.2$ million: figure a couple seconds of computing time. If you compile this you might speed up the performance two orders of magnitude.

Incidentally, in these test cases, graphs of the distribution clearly showed some positive skewness: they aren't normal.

For the record, here is a Mathematica solution:

pb[p_, z_] := Module[

{\[Mu] = Total[p]},

Fold[#1 - #2 Differences[Prepend[#1, 0]] &,

Prepend[ConstantArray[0, Ceiling[\[Mu] + Sqrt[\[Mu]] z]], 1], p]

]

(NB The color coding applied by this site is meaningless for Mathematica code. In particular, the gray stuff is not comments: it's where all the work is done!)

An example of its use is

pb[RandomReal[{0, 0.001}, 40000], 8]

Edit

An R solution is ten times slower than Mathematica in this test case--perhaps I have not coded it optimally--but it still executes quickly (about one second):

pb <- function(p, z) {

mu <- sum(p)

x <- c(1, rep(0, ceiling(mu + sqrt(mu) * z)))

f <- function(v) {x <<- x - v * diff(c(0, x));}

sapply(p, f); x

}

y <- pb(runif(40000, 0, 0.001), 8)

plot(y)

p_is are fixed. $\endgroup$sinibpackage. journal.r-project.org/archive/2018/RJ-2018-011/RJ-2018-011.pdf $\endgroup$