I'm trying to produce one-day ahead volatility forecasts for Bitcoin with Realized GARCH(1,1) using the rugarch package in R. The realized variance(data$rv5) is aggregated based on a 5 minute frequency, and the returns(data.xts$ret) are close-to-close. Here's the specs and result:

rgarch.spec<- ugarchspec(mean.model = list(armaOrder= c(0,0),

include.mean = FALSE),

variance.model = list(model= 'realGARCH',

garchOrder= c(1,1)),

distribution.model = 'norm')

rgarchroll<- ugarchroll(spec = rgarch.spec,

data= data.xts$ret,

n.ahead = 1,

forecast.length = forecast_len,

refit.every = 5,

solver= 'hybrid',

realizedVol= data.xts$rv5,

VaR.alpha = c(0.01, 0.05, 0.10))

where

realized_vol= sqrt(tail(data.xts$rv5, forecast_len)),

rgarch.prediction_vol= rgarchroll@forecast$density$Sigma)

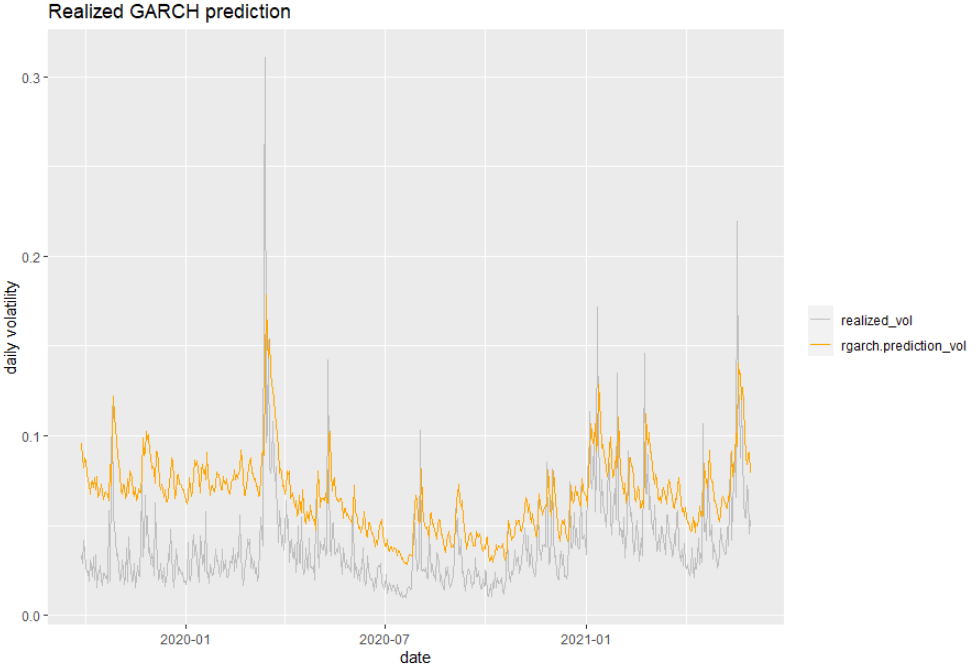

As you can see, the predicted volatility is consistently higher than the realized volatility. Needless to say, the VaR predictions are not accurate at all. However, the standard GARCH(1,1) model works fine using the same return data. So what could possibly be the issue?

Also, I found a another tread discussing a similar problem(GARCH(1,1) volatility forecast looks biased, it is consistently higher than Parkinson's HL vol). However, I don't really see how the answer applies to this case as there are no non-trading hours for Bitcoin.