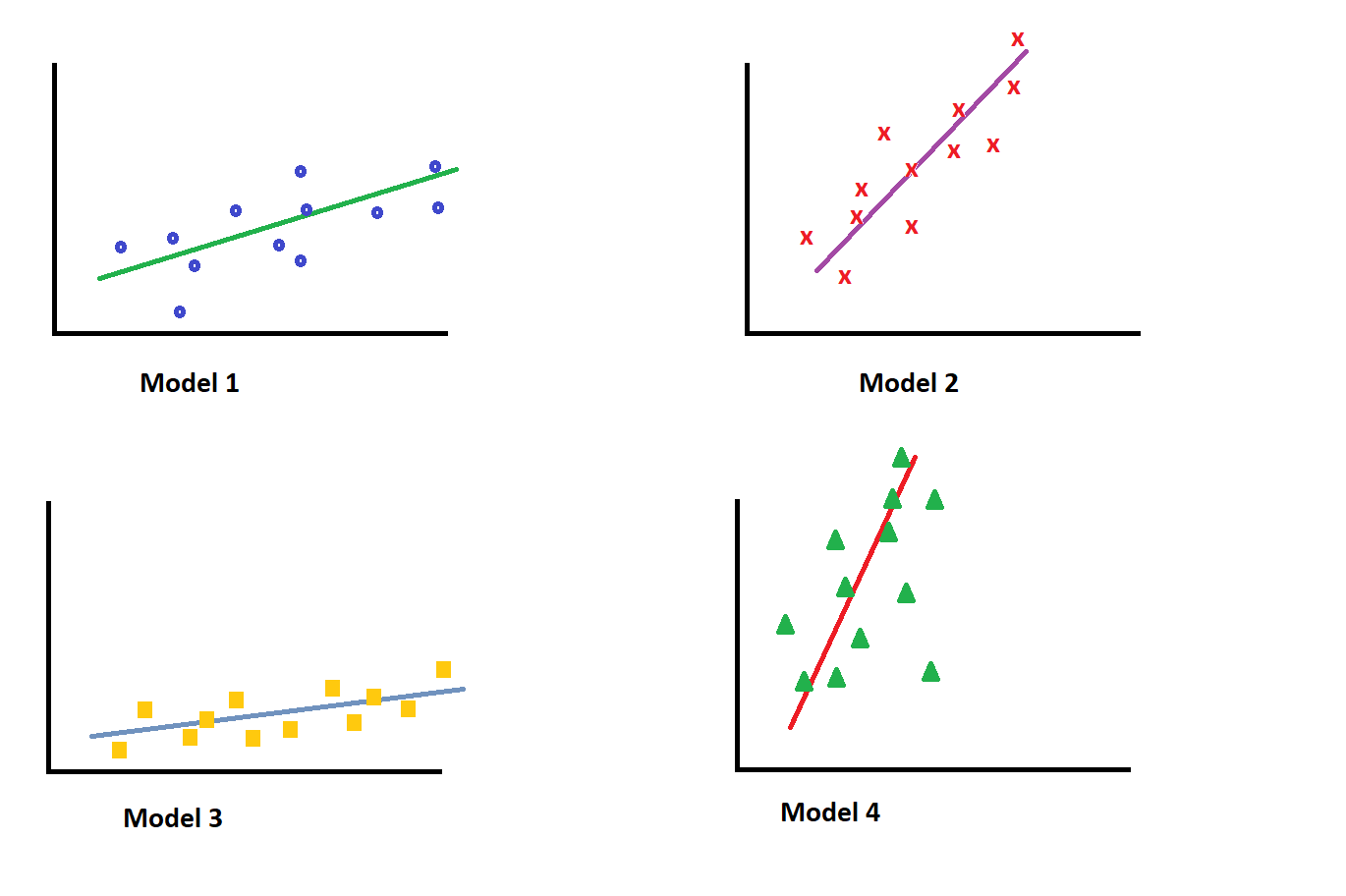

I have a dataset of 48,000 records

These records are divided equally into 4 groups

Blue Group, Yellow Group, Green Group, and Red Group

Each one of these groups has 12,000 records

My study has resulted in 4 regression models

Model 1 equation was $a_1 x + b_1$

Model 1 equation was $a_2 x + b_2$

Model 1 equation was $a_3 x + b_3$

Model 1 equation was $a_4 x + b_4$

The thing is that the dataset is not available anymore and I want the regression model for all dataset points

Can I get the average of all 4 models to get the regression for all data points?

So it will be $((a_1 + a_2 + a_3 + a_4)/4) x + (b_1 + b_2 + b_3 + b_4)/4$

is this model the right model for all data points?