How would one convert the ATE Average Treatment Effect from a doubly robust model into Risk Ratio? Can this be done directly without having to convert to odds ratio first. If so, how is this done. Can the conversion be directly applied to the confidence intervals or would bootstrapping have to be done?

$\begingroup$

$\endgroup$

7

-

$\begingroup$ Clarifying question: if you’re talking about risk ratio here, I’m guessing that your Y’s are binary then? $\endgroup$– stats_modelCommented Oct 20, 2021 at 12:03

-

$\begingroup$ @stats_model The main outcomes are binary - this is more important. Although, it is also possible for outcome to be continuous (this is nice to have but optional). $\endgroup$– StatsBioCommented Oct 20, 2021 at 12:13

-

$\begingroup$ What is the reasoning for converting the risk difference (referred to as the ATE here) to the risk ratio? The doubly robust estimator you show above estimate the risk under A=1 and the risk under A=0. You could just manipulate those risks to get whatever transformation you want (i.e. replace $-$ with $/$ in the equation). $\endgroup$– pzivichCommented Oct 20, 2021 at 12:24

-

$\begingroup$ @pzivich Thanks, I think the risk ratio is more interpretable than risk difference, correct me if I am wrong, because for risk ratio risk (treatment = 1) / risk (treatment = 0), we could say that treatment 1 is 2.5 times more likely to result in the outcome than treatment 0. However, a risk difference ATE does not seem so easy to interpret. $\endgroup$– StatsBioCommented Oct 20, 2021 at 12:50

-

$\begingroup$ @pzivich What threw me here is typically for risk ratios, you would be comparing incidence, but with doubly robust model, we have "estimated incidence" subtracted by the inverse weighted propensity score. In addition, I think risk ratio is more interpretable than odds ratio, but I see a lot of use of odds ratio and ATEs and very little use of risk ratios. $\endgroup$– StatsBioCommented Oct 20, 2021 at 12:51

|

Show 2 more comments

2 Answers

$\begingroup$

$\endgroup$

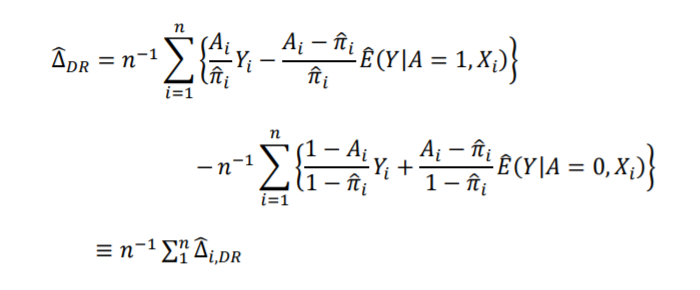

In the formula for the doubly robust estimator provided (augmented inverse probability weighting), it is shown for the ATE. The key piece to note is that

$$\hat{\theta}_{1} = n^{-1} \sum_{i=1}^n \frac{I(A_i=1)Y_i}{\hat{\pi}(W_i)} - \frac{A_i-\hat{\pi}(W_i)}{\hat{\pi}(W_i)} \hat{E}[Y|A=1,X_i]$$

is the estimator for the risk had everyone been given $A=1$. The second part similar follows for the risk had everyone been given $A=0$, which I indicated as $\hat{\theta}_0$. This estimator consists of 3 pieces, the inverse probability weighting part ($\frac{I(A_i=1)Y_i}{\hat{\pi}(W_i)}$), the predicted outcome ($\hat{E}[Y|A=1,X_i]$), and the 'glue' ($\frac{A_i-\hat{\pi}(W_i)}{\hat{\pi}(W_i)}$). Together these come together to estimate the risk. This form has the nice property of double robustness, but are still estimating the risk.

Once you have the two $\hat{\theta}$ or risks, you can calculate whatever contrast you prefer by manipulating those risks. For example the risk difference is just the difference in those risks (this is written out above without my $\theta$ shorthand) $$ \hat{\theta}_1 - \hat{\theta}_0$$ If you want the risk ratio, $$ \hat{\theta}_1 / \hat{\theta}_0$$ This second contrast for the risk ratio is equivalent to replacing the minus sign in the provided formula with a division.

The key piece is that the doubly robust estimator estimates each risk individually. The ATE is often frame as the estimand, so that's why it is usually presented in that form. However, the estimated risks from the doubly robust estimator can be transformed as desired.

For the estimator of the variance, influence curves are often used for the above doubly robust estimator. It is important to note that the form of the influence curve changes between the risk difference and risk ratio. Therefore, the variance estimator is a little more complicated. A simple solution is to bootstrap the variance.

$\begingroup$

$\endgroup$

1

You can split out the doubly robust estimator into two components: $$\hat \Delta_{DR} = \hat \Delta_{DR,1} - \hat \Delta_{DR,0}$$ where $$\hat\Delta_{DR,1} = \frac1n\sum_{i=1}^n \frac{Y_i}{\hat \pi_i} - \frac{A_i-\hat\pi_i}{\hat\pi_i}\hat E(Y|A = 1,X_i)$$ $$\hat\Delta_{DR,0} = \frac1n\sum_{i=1}^n \frac{Y_i}{1-\hat \pi_i} - \frac{A_i-(1-\hat\pi_i)}{1-\hat\pi_i}\hat E(Y|A = 0,X_i)$$ It is straightforward to show that (provided the substantive and regularity conditions motivating the DR estimator are true) that $\hat \Delta_{DR,1}, \hat \Delta_{DR,0}$ are separately consistent estimators of $E[Y_{i1}]$ and $E[Y_{i0}]$. Then by continuous mapping theorem, we know that $$\frac{\hat \Delta_{DR,1}}{\hat\Delta_{DR,0}}\overset p\to \frac{E[Y_{i1}]}{E[Y_{i0}]}$$ Moreover, supposing that $\hat \Delta_{DR,1}, \hat \Delta_{DR,0}$ are asymptotically normal, i.e. $$\sqrt n((\hat \Delta_{DR,1}, \hat \Delta_{DR,0})^T - \mu^T) \overset d\to \mathcal N(0,\Sigma)$$ where $\mu = (\mu_1,\mu_0) \equiv (E[Y_{i1}], {E[Y_{i0}]})$ and $\Sigma$ is the asymptotic variance matrix, then the delta method would yield $$\sqrt n\left(\frac{\hat \Delta_{DR,1}}{\hat\Delta_{DR,0}} - \frac{E[Y_{i1}]}{E[Y_{i0}]}\right)\overset d\to \mathcal N(0,g \Sigma g^T)$$ where $$g = \left(\frac{1}{\mu_0}, - \left(\frac{\mu_1}{\mu_0^2}\right)^2\right)$$ Finally, as usual, you can plug $\hat \Delta_{DR,1}, \hat\Delta_{DR,0}$ respectively for $\mu_1,\mu_0$ in the expression for $g$ and still obtain asymptotically valid inference.

-

$\begingroup$ I like this explanation as well (+1) since it covers a different aspect of the question, but I think pzivich's explanation is more comprehensive. $\endgroup$– StatsBioCommented Oct 20, 2021 at 13:40