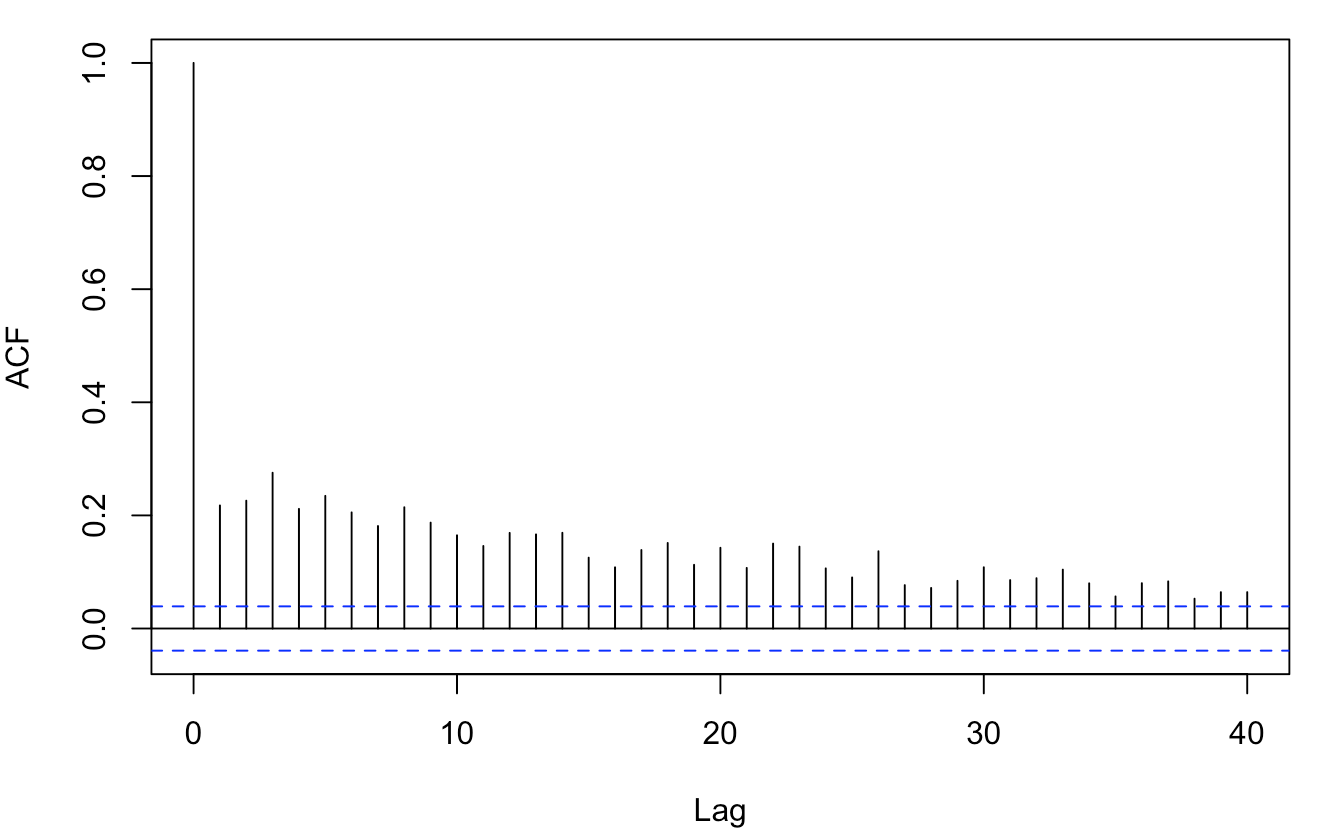

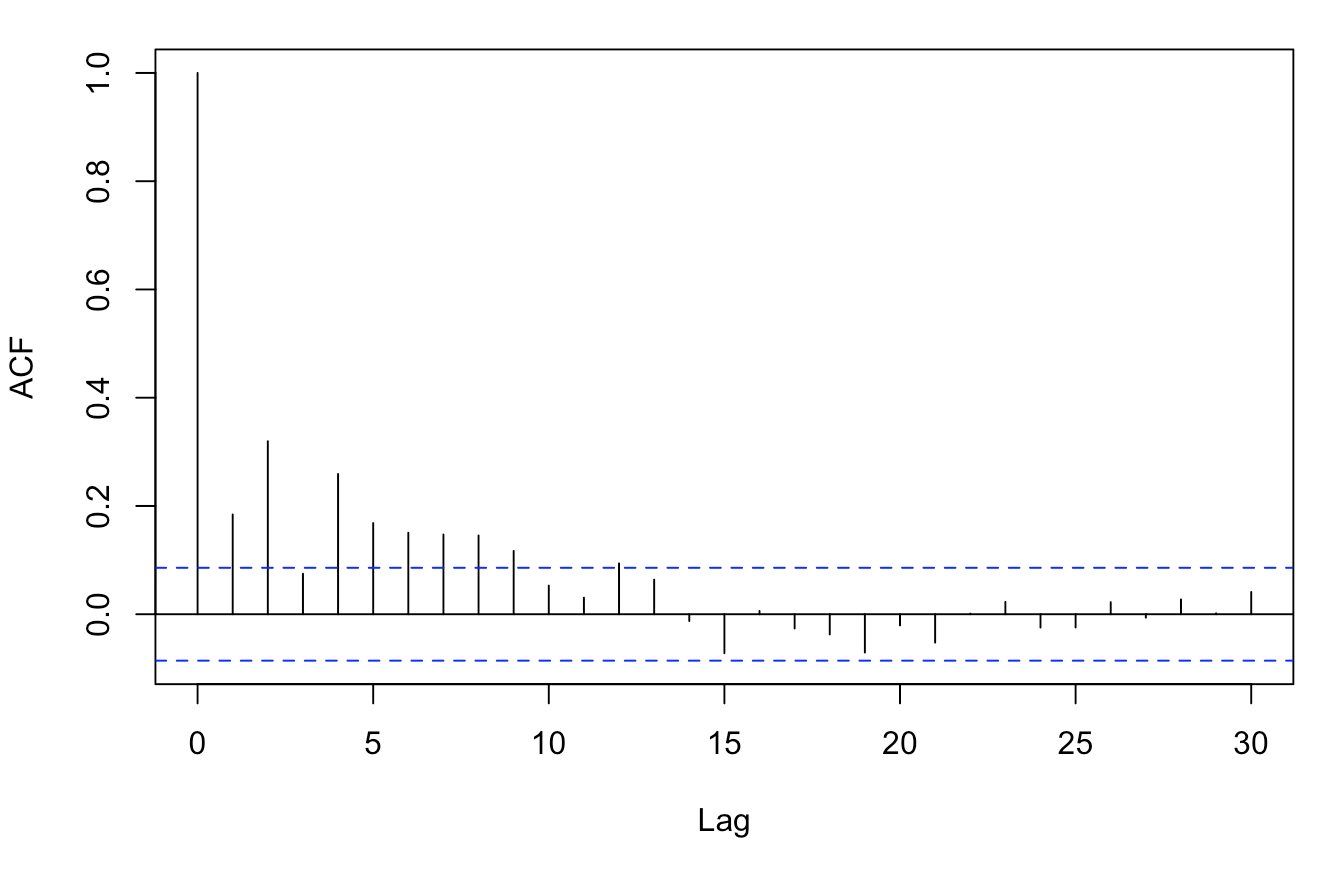

Can someone explain me the interpretation of volatility clustering from ACF of the absolute returns?

I got two graphs of ACF of the absolute returns (first one for daily returns, second one for weekly returns):

Can someone explain me the interpretation of volatility clustering from ACF of the absolute returns?

I got two graphs of ACF of the absolute returns (first one for daily returns, second one for weekly returns):

Volatility clustering means that high returns - in an absolute sense - at time $t$ tend to be followed by high returns in - an absolute sense - at time $t+1$ and vice versa. In other words, if volatility is high today, we expect volatility to be high tomorrow and vice versa. The ACF plots suggest that your time series exhibits volatility clustering as there is a significant auto-correlation between absolute returns, even at higher order lags. In addition, note that that this relationship is much stronger for daily returns than for weekly returns. You will observe this phenomenon in almost all return time series.