For "the" variance of a process $X_t$ to mean anything at all, we must suppose (at a minimum) that the variance of $X_t$ is the same for all $t.$ Let's call this common (finite) variance $\sigma^2.$

Almost always, such a constant-variance assumption goes along with the stronger assumption of second order stationarity, which adds that for any "lag" $s,$ the covariance of $(X_t, X_{t+s})$ is the same for all $t$ (but, of course, may vary with the lag).

The first-differenced process is, by definition, the most recent change

$$(\Delta X)_t = X_t - X_{t-1}.$$

Using the bilinearity of covariance we may compute

$$\begin{aligned}

\operatorname{Var}((\Delta X)_t) &= \operatorname{Var}(X_t - X_{t-1}) = \operatorname{Var}(X_t) + \operatorname{Var}(X_{t-1}) - 2 \operatorname{Cov}(X_t, X_{t-1}) \\

&= 2\sigma^2(1 - \operatorname{Cor}(X_t, X_{t-1})).

\end{aligned}$$

Writing $\rho$ for the lag-1 correlation that appears in this formula, the question asks us to compare $\sigma^2$ to $2\sigma^2(1-\rho).$ Their ratio (assuming $\sigma^2\ne 0$) is $2(1-\rho),$ which exceeds $1$ when $\rho \lt 1/2$ and otherwise is less than or equal to $1.$ Thus, the variance of the differenced series may be larger or smaller than the original variance, depending on the lag-one correlation.

When $X_t$ is a second-order stationary time series, the variance of its first difference increases when the lag-1 autocorrelation is less than $1/2$ (including all negative values); the variance decreases when the lag-1 autocorrelation is greater than $1/2$ ; and otherwise the variance remains the same when the lag-1 autocorrelation equals $1/2.$

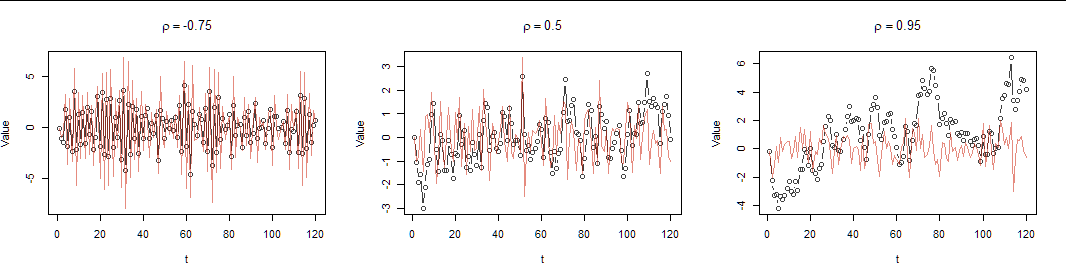

These plots illustrate the phenomenon. The black points and lines graph realizations of the original series $X_t$ while the red lines graph their first differences.

At the left, the negative correlation means $X_t$ tends to swing back and forth around an average of zero, causing the differences to be larger than $X_t.$ At the right, the positive correlation means each $X_{t+1}$ is close to its predecessor $X_t,$ whence the differences tend to vary less than the original values. The middle shows the boundary case $\rho=1/2$ where the differences tend to have the same sizes as the original values.

This analysis gives us a way to construct examples. The two extremes are the cases $\rho=\pm 1.$ When $\rho=1,$ each $X_{t+1}$ must be an (order-preserving) linear transformation of $X_t,$ so taking these transformations to be the identity, we obtain an example where all the $X_t$ are the same variable. Their common variance $\sigma^2$ is reduced to zero because $\Delta X_t = 0$ for all $t.$

At the other extreme, when $\rho=-1,$ again each $X_{t+1}$ must be an order reversing linear transformation of $X_t,$ of which the simplest is $X_{t+1}=-X_t.$ This leads to the example $X_t = (\pm 1)^t X$ where the series alternates between the value of a random variable $X$ and its negative. Now the differenced series alternates between twice $X$ and its negative, which has four times the original variance.

It is worth noticing that differencing a series with zero lag-1 autocorrelation (such as a series of independent variables) causes the variance to double. This is because each successive difference involves two variables and their variances add.