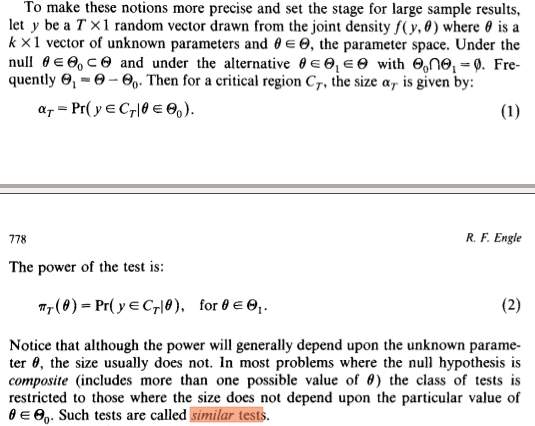

From Wald. Likelihood ratio, and lagrange multiplier tests in econometrics by Robert f. Engle:

(Tests whose) size does not depend upon the particular value of $\theta \in$ null $\Theta_0$ are called similar tests.

I don't quite understand the definition. Isn't the size of a test the sup of false positive rate over null $\Theta_0$? So it doesn't depend on a single $\theta \in \Theta_0$, but on $\Theta_0$?

Following provides more context from the source. Thanks and regards!