I'm reading about Robust Standard Error Estimators for Panel Models from the developer of plm R package (Millo, 2017: 21). But my question is not about software.

In the example I see that some heteroscedasticity robust standard errors are in fact less than those in benchmark OLS. I thought that we normaly expected robust errors to be at least as large as their OLS counterparts.

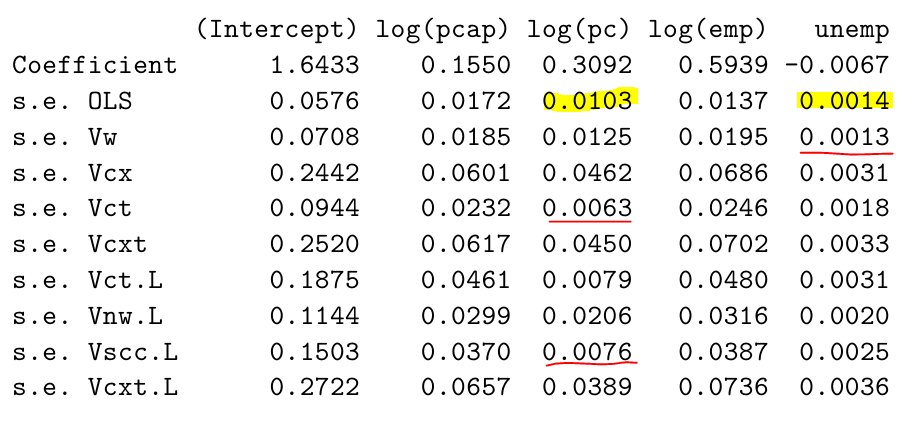

Below you see the comparison of different HC procedures, for the same model with coefficients arranged by columns.

My question concerns this situation. Is it fine in general and how to interpret this fact if, i.e. in real model, such a change in s.e. changes the significance of a coefficient?