I'm using glmnet to fit a ridge regression model on some data and evaluate the model's test MSE. The lambda value I select is derived from cross-validation. I'm using the College dataset from ISLR2, predicting applications to each college.

I have tried the following two approaches, and while in theory I should have the same result, I don't and I'm not sure why.

First way

- I use

cv.glmnet()to perform cross validation on the data, extracting the lambda with the lowest validation MSE - Then I fit a ridge regression model using

glmnet()on the data with the previously computed lambda - Predict response on the test data using the fitted model and compute the test MSE

# Perform the cross validation

cv.ridge <- cv.glmnet(model.matrix(Apps~.,train), train$Apps, alpha=0, nfold=100)

# Store the best lambda value

best.lambda <- cv.ridge$lambda.min

# Fit ridge regression model with that lambda

ridge.fit <- glmnet(model.matrix(Apps~.,train), train$Apps, alpha=0, lambda=best.lambda)

# Predict the test response

pred.out <- predict(cv.ridge, newx = model.matrix(Apps~.,test), s=best.lambda)

# Compute test MSE

mean((pred.out- Y_test)^2)

>> 2206587

Second Way

- Once again I use

cv.glmnet()to perform cross validation on the data - I then predict the response on the test data directly with the

cv.glmnetobject, using the lambda value with the lowest validation MSE - Compute the test MSE

# Perform the cross validation

cv.ridge <- cv.glmnet(model.matrix(Apps~.,train), train$Apps, alpha=0, nfold=100)

# Store the best lambda value

best.lambda <- cv.ridge$lambda.min

# Predict the test response

pred.out <- predict(cv.ridge, newx = model.matrix(Apps~.,test), s=best.lambda)

# Compute test MSE

mean((pred.out- Y_test)^2)

>>> 2204831

Why do these two approaches have different test MSE's? The only difference between the two ways is that in the second way I use the cv.glmnet object instead of the glmnet object in the predict() call.

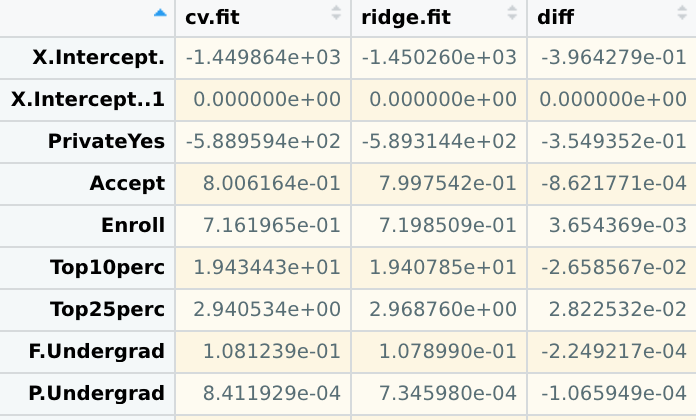

I checked the coefficients of the models and they are not the same either.

# Coefficients from the glmnet() call on the specified lambda

coef(ridge.fit)

# Coefficients of the cv.glmnet() call given the same specified lambda

predict(cv.ridge, type='coefficients', s=best.lambda)

The coefficients are slightly different. Which I guess is why the test MSE's differ. But I'm not sure why this should be the case.

In both ways, since the lambda constraint specified is identical and the data used to fit the model is identical, shouldn't the resulting two ridge regression models be the same?

Follow up :

I have tried setting the s parameter in the predict call but that doesn't seem to work either.

cv.ridge MSE :

# Fit cross-validated ridge regression model

cv.ridge <- cv.glmnet(model.matrix(Apps~.,College), College$Apps, alpha=0, nfold=100)

# Make prediction using lambda that minimizes cross-val MSE

pred.out <- predict(cv.ridge, model.matrix(Apps~.,College), s="lambda.min")

# Compute MSE

mean((pred.out- College$Apps)^2)

>> 1358455

glmnet way :

# Explicitly fit a ridge regression model on the same data using the previously computed lambda that minimizes CV mse

ridge.fit <- glmnet(model.matrix(Apps~.,College), College$Apps, alpha=0, lambda=cv.ridge$lambda.min)

# Make prediction

pred.out <- predict(ridge.fit, model.matrix(Apps~.,College))

# Compute MSE

mean((pred.out- College$Apps)^2)

>> 1359837

The issue persists.

Note that in the glmnet way I didn't set any s parameter since the provided glmnet object only contains the fitted model with the lambda which minimizes CV MSE. The same lambda value used when the cv.ridge object does the prediction as well.

Setting s='lambda.min' doesn't change the result either.