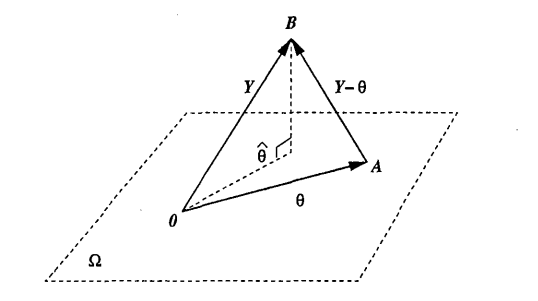

Suppose we have a linear model $Y=X \beta + \epsilon$ where $\epsilon \sim N(0, \sigma^2 I)$ and let $H$ be the projection matrix into the column space of $X$. We define the residual $e$ as the projection of $Y$ into span$(X)$ (i.e. $e=(I-H)\epsilon \text{ }$).

A statement says that : by construction, $X^T e=0$ and it implies that no correlation should appear between explanatory variables and residuals.

I can convince myself that the statement is true by saying that if $X_i$ is a column of $X$, then using the fact that $E(e)=0$, we have $Cov(X_i,e)=\Bbb E(X_i. e)- \Bbb E(X_i )\Bbb E(e)=0 \implies Corr(X_i,e)=0$.

However, I don't really intuitively see why there should or not be any correlation between explanatory variables and residuals. Can someone explain the intuition behind the statement ?