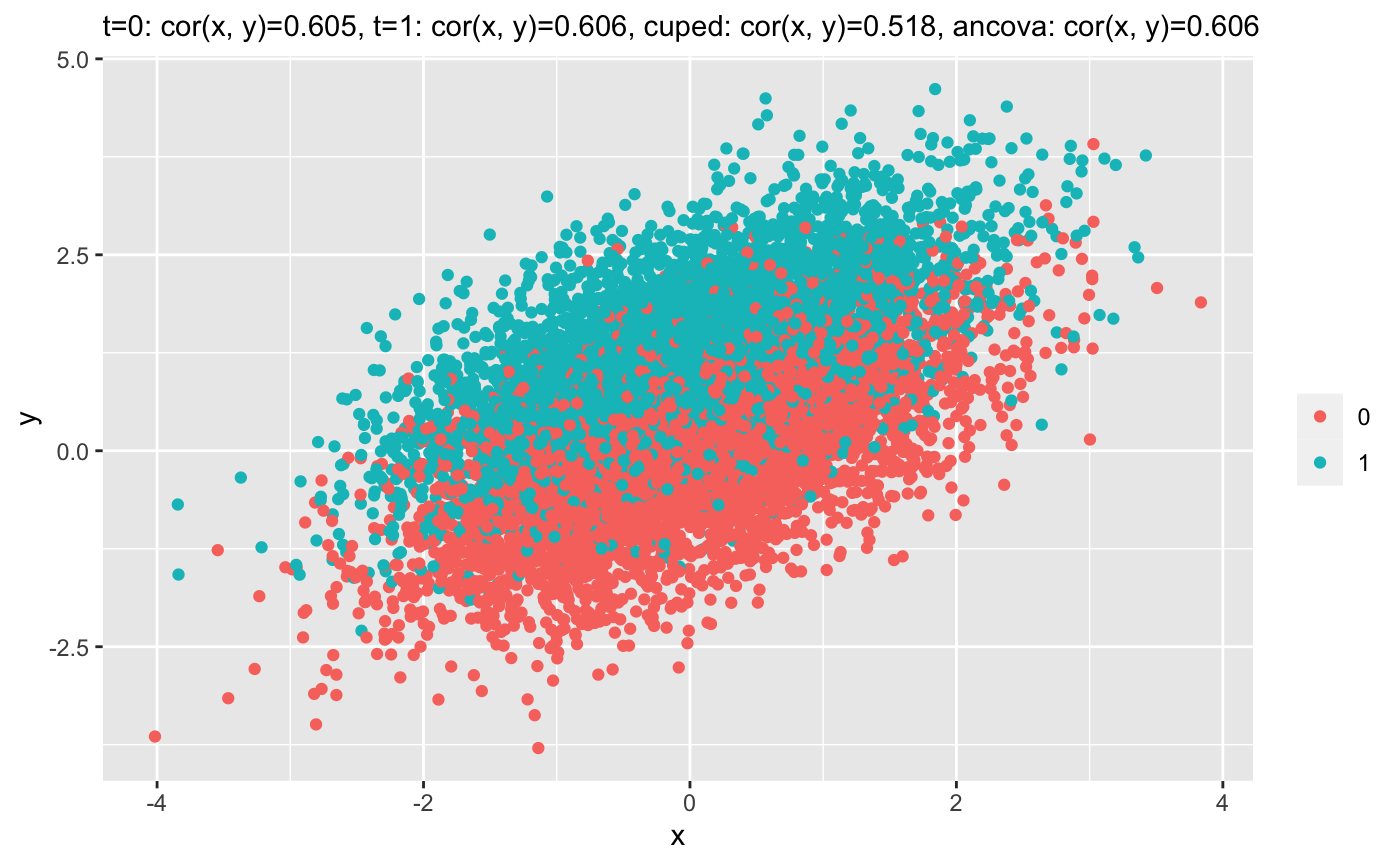

CUPED (Controlled-experiment Using Pre-Existing Data) is a variance reduction technique created by Microsoft in 2013 and widely used in technology companies. let Y is the target metrics and X is pretreatment covariate, T is treat variable(to simplify the discussion, we assume that there are only two treatment group, T = 0 is control group, T = 1 is treat group),the main idea of CUPED is:

- compute $\theta$

$$\theta = \frac{\operatorname{cov}(Y, X)}{\operatorname{var}(X)} = \operatorname{corr}(X, Y) \cdot \operatorname{var}(Y) = \rho \cdot \operatorname{var}(Y)$$

compute adjusted $Y_i^{cv} = Y_i - (X_i - \mu_X) \cdot \theta$ for each user

evaluate the AB test using $Y_i^{cv}$ instead of $Y_i$

the result cuped-adjusted estimate treat effect is

$$\tau = (\overline Y_1 - \theta \cdot (\overline X_1 - \mu_X)) - (\overline Y_0 - \theta \cdot (\overline X_0 - \mu_X)) \\= (\overline Y_1 - \overline Y_0) - \theta \cdot (\overline X_1 - \overline X_0)$$

Another widely used and long-established method for increase power and adjusting preexisting differences is ANCOVA(Analysis of covariance) or regression-adjustment.

The ANCOVA model assumes a linear relationship between the response (Y) and covariate (X):

$$ Y = b_0 + \tau \cdot T + \theta\cdot X $$

the result regression-adjusted estimate treat effect is same as above, the only difference seems to be how to estimate $\theta$, so My questions is which one is more reasonable ?