My question is related to the autocorrelation present in the mean-model (which is an ARMA process), which will be used in a GARCH model. Is it ok to have autocorrelations in the residuals of the mean-model, given that it will be used in a GARCH model, which by robust standard errors takes care of the residuals in the variance model?

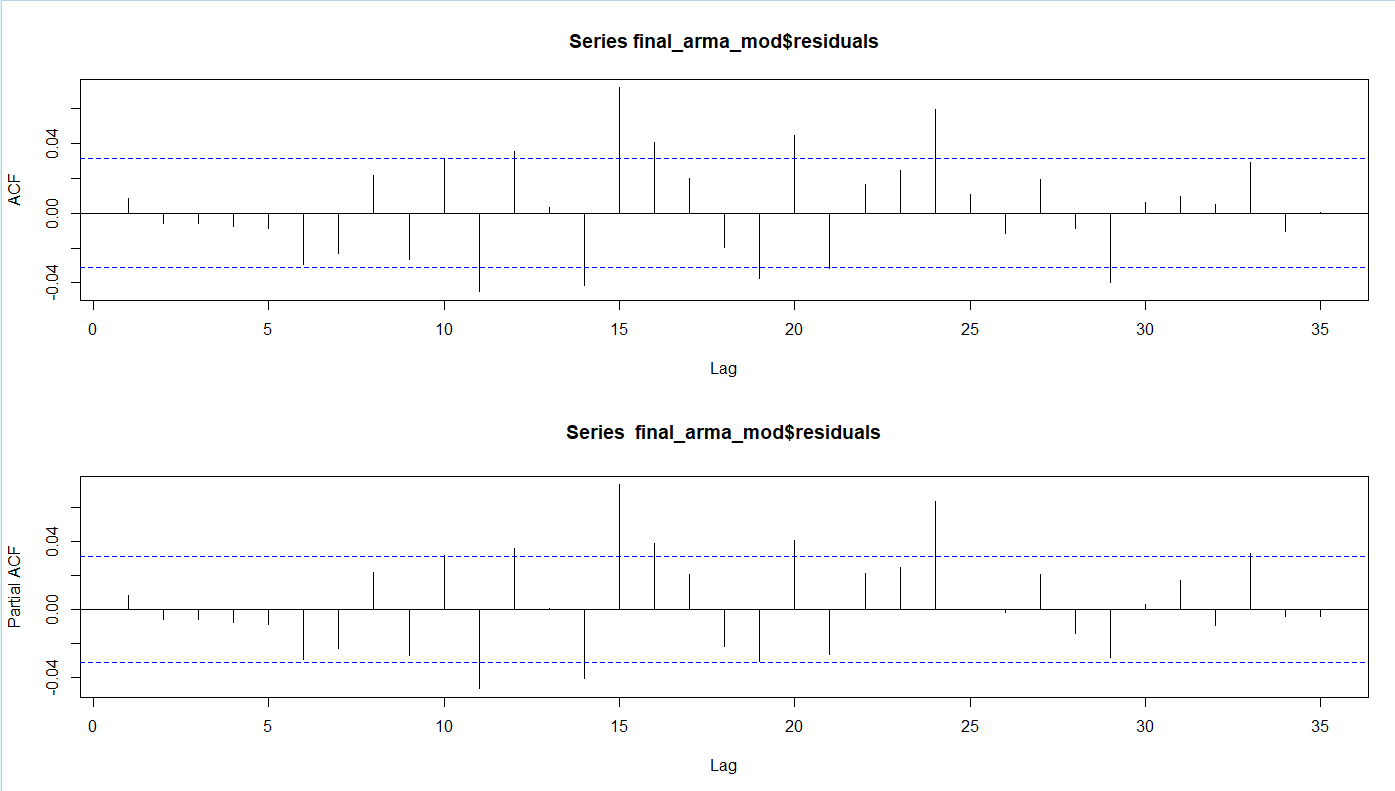

I have edited my question a bit and attached the ACF and PACF plots of the residuals of the ARMA process with AR=11, MA=6, and zero mean. Via an algorithm, this was the model with the lowest AIC value. Using checkresiduals in R, the Ljung-Box test figures are:

data: Residuals from ARIMA(11,0,6) with zero mean Q* = 23.228, df = 3, p-value = 3.619e-05

Model df: 17. Total lags used: 20

Based on this, there is autocorrelation present.

Based on these plots, can I consider the model good for a statistically adequate descriptive model and ignore the Ljung-Box result?

EDIT: 2

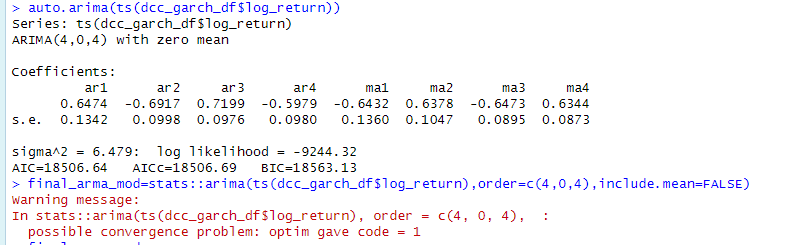

Based on discussions and advice, I am attaching the screen-shot of the output of the model, prescribed by auto.arima. It gives an optimum model of (4,0,4). But when I run the model in the ARIMA function, it shows a convergence problem. The screenshot is given below:

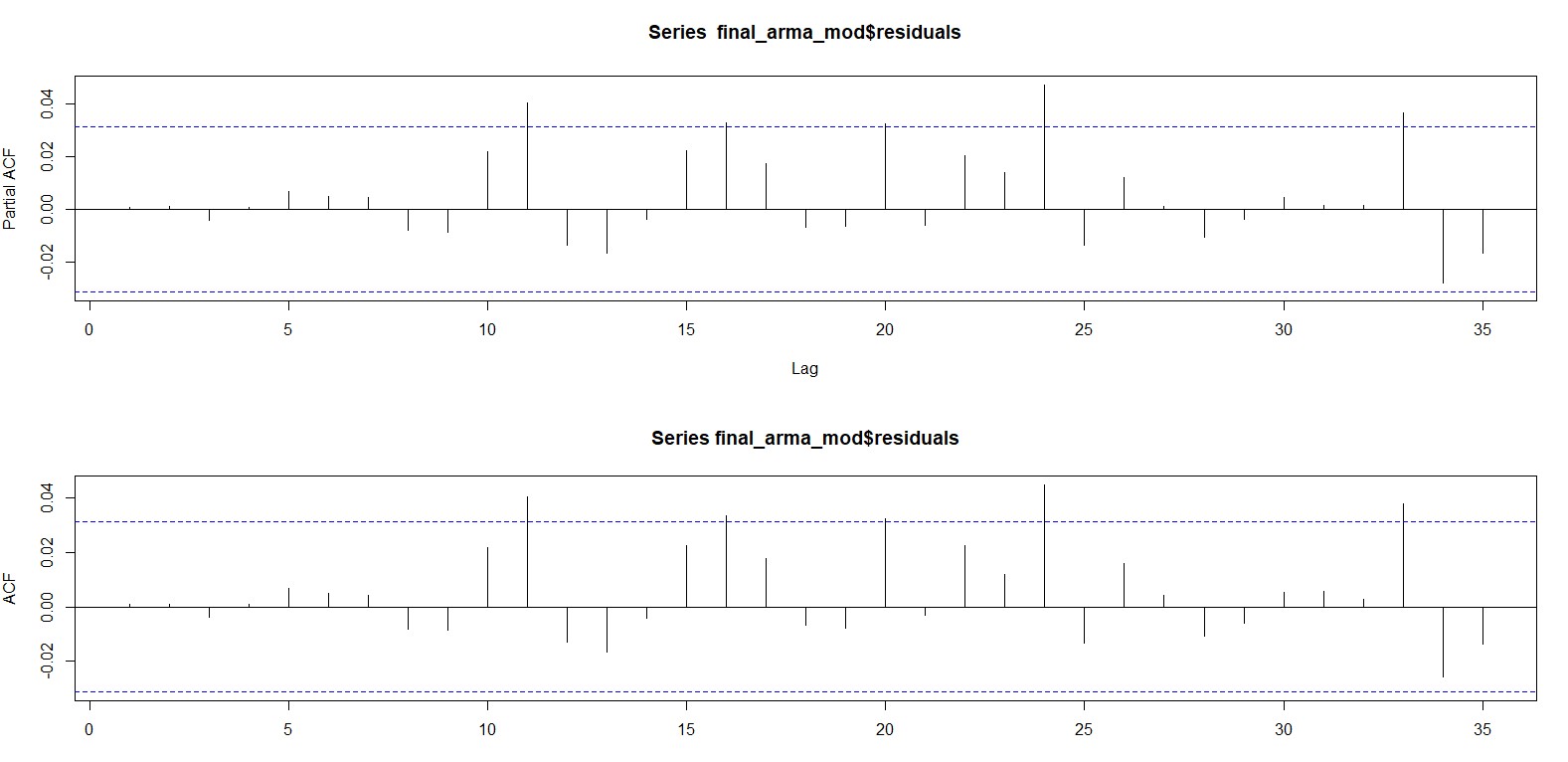

The ACF and PACF plots for (4,0,4) are:

How do we take care of the convergence issue? Is it ok to accept the model?

The original log return series is:

EDIT: 3

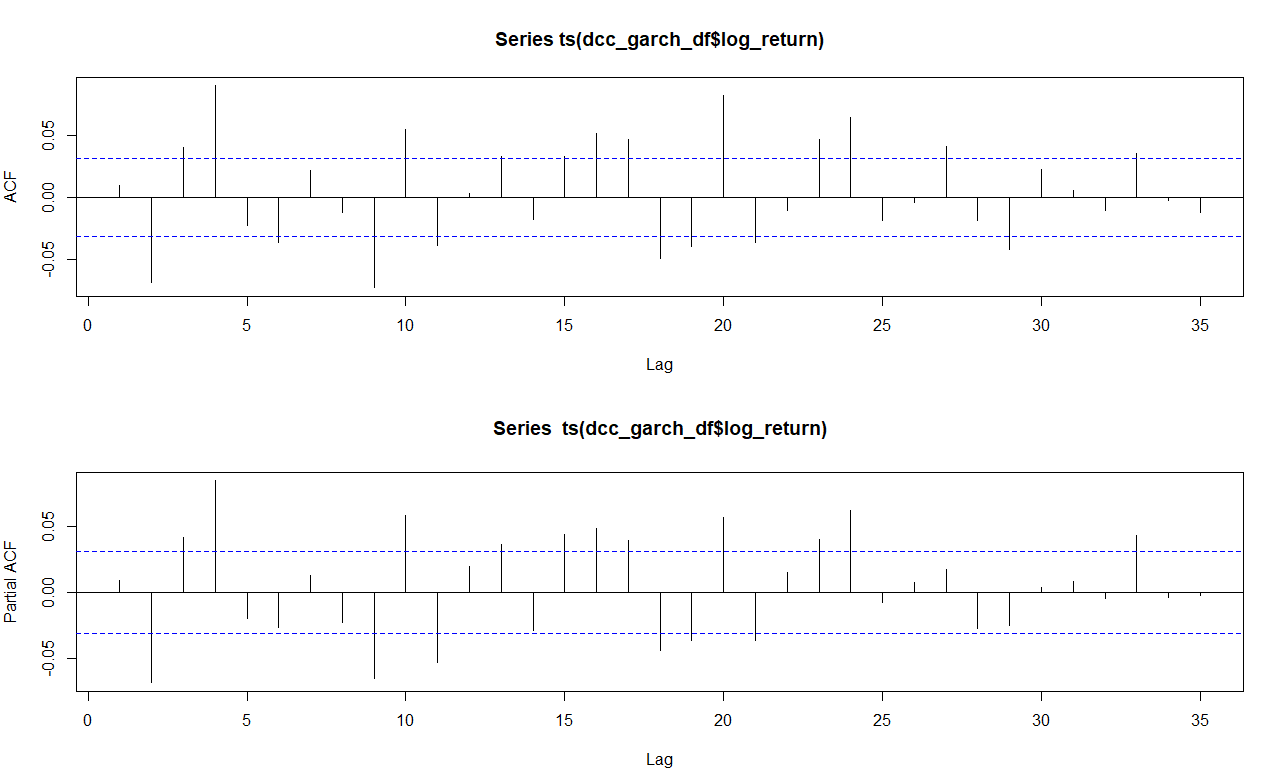

The ACF & PACF of the return series is given below: