I want to investigate, weather financial news have an influence on the volatility prediction of asset returns (daily data) when including them into the variance model/mean model.

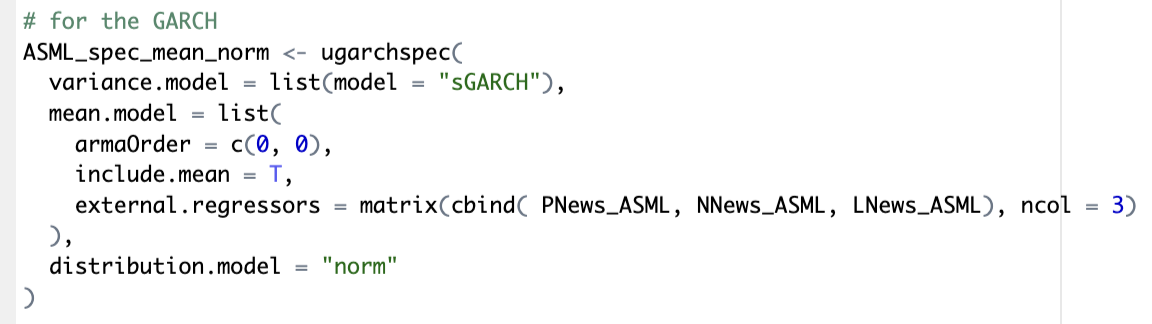

I have fit a GARCH/EGARCH/GJR-GARCH (1,1) model with 3 distributions (normal, student's t and GED) for 7 individual assets. One time without exogenous variables and one time including exogenous variables (a) into the mean eq. and (b)into the variance eq.

Mean:

Variance:

The exogenous variables are positive news (amount of news multiplied with a sentiment score), negative news, and lagged total amount of news.

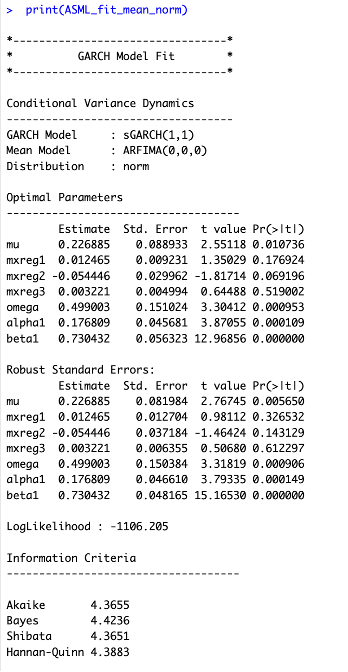

Including the mean is most of the time insignificant, the external regressors for conditional variance models are most of the time insignificant, the regressors for the mean models are sometimes significant.

Does including the external regressors into the mean model make the constant mean to a conditional mean?

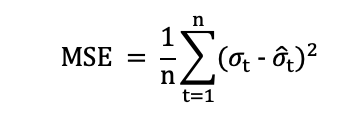

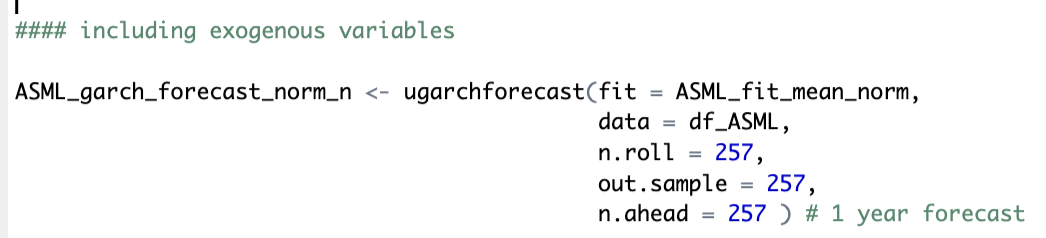

Second, if including the external regressors actually make the volatility forecast better. Therefore, I would compare the MSE of the forecasted (out-of-sample model) with what? Because, obviously there is no conditional variance of the real data, so I am not sure what the MSE is actually computed (see code). Do I only compare the estimates of the e.g. GARCH (1,1) incl. exogenous variables into the mean model with the forecasted estimates of the same model? (That would imply, that I need to have a very well fitted model, otherwise this comparison doesn't make sense).

My MSE assumption:

I use the rugarch package and R-studio.

Thank you!