I am holding a coin, of unknown bias, in my hand. I flip it once, and it comes down heads. A friend asks me what a fair bet would be for the next flip to be heads.

What's the frequentist point estimate of the probability that the next flip is heads?

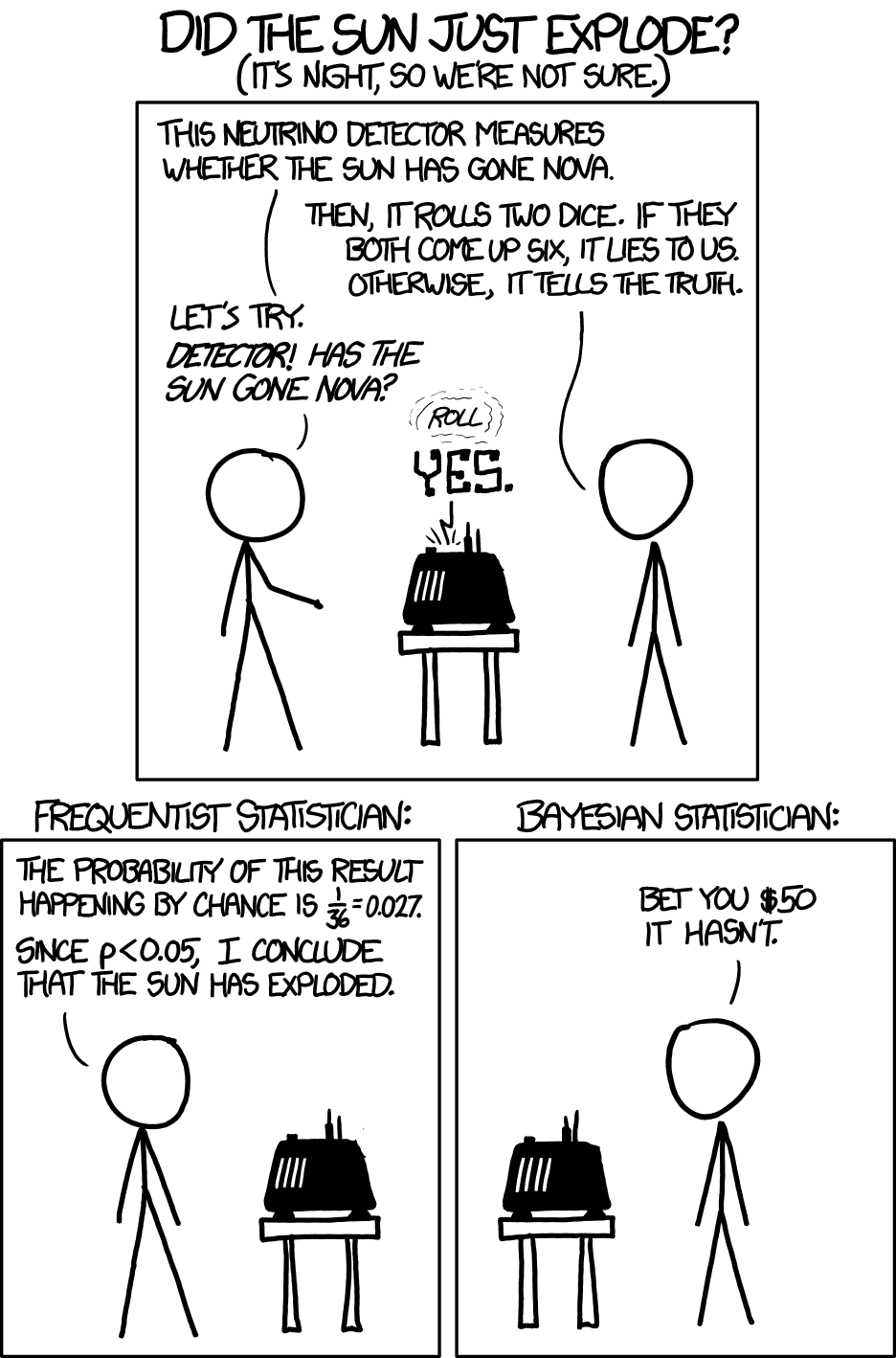

(The answer is less obvious than it may appear, as "frequentist" does not specify the estimation procedure.)

As a Bayesian, this is straightforward. Because a vast amount of randomness in the result is due to my erratic coin-flipping procedure and the symmetry induced by having the coin either face up or face down when flipping it, I find it extremely unlikely that a coin flip will be biased by more than 1% (49%-51%). I put a Beta(10,000, 10,000) prior on the probability of a head, which gives me a prior mean of 50% and a prior standard deviation of 0.005. My posterior is therefore a Beta(10,001, 10,000) distribution, and the posterior mean is 10,001 / 20,001 or 0.500025.

Edit in response to comments:

Bayesian statistics is focused on "small" samples, as asymptotically in (most) situations Bayesian and MLE results become the same. However, in my past applied work - estimating degradation rates of solar panels based on a limited number of years of experimentation - even sample sizes of 100 (application specific) aren't as informative as you might think they would be, and prior information can really make a difference.

Also, why limit yourself to a small experimental group when you have sufficient prior information available to, indirectly, allow you to have a large experimental group? In a way, it's the experimental group you're really interested in, after all.