Wikipedia defines a p-value as follows:

the p-value is the probability of obtaining test results at least as extreme as the result actually observed, under the assumption that the null hypothesis is correct.

And to compute a p-value, we need a sampling distribution.

My question is: when we talk about the null hypothesis here, are we referring to the sampling distribution constructed:

- Before any data is collected (a priori), or

- After data has been collected (a posteriori)?

Bonus points for providing any reference which speaks to this explicitly.

I think the correct answer is the a priori version, otherwise our type 1 and 2 error rates may deviate from the rates specified during the power analysis. However, I believe most A/B test software calculates the p-value from the sampling distribution generated directly from the sample data collected - so I'm confused.

Quick example

Suppose that I am planning to test a new website landing page, with the aim of improving conversion rates. Applying the Null Hypothesis Significance Testing framework (NHST), I lay out my hypotheses a priori:

- Null hypothesis (H0): treatment and control samples are drawn from populations with identical proportions: 6% conversion rates

- Alternate hypothesis (HA): treatment and control samples are drawn from populations with different proportions: 7% and 5% conversion rates, respectively

To achieve a significance level of 0.05 and a power of 0.8, I calculate a minimum required sample size of 2213:

# R code

prop_baseline <- 0.05

prop_treatment <- 0.07

alpha <- 0.05

beta <- 0.2

n <- ceiling(

power.prop.test(

p1 = prop_baseline,

p2 = prop_treatment,

sig.level = alpha,

power = 1-beta,

alternative = c("two.sided")

)$n

)

n

# [1] 2213

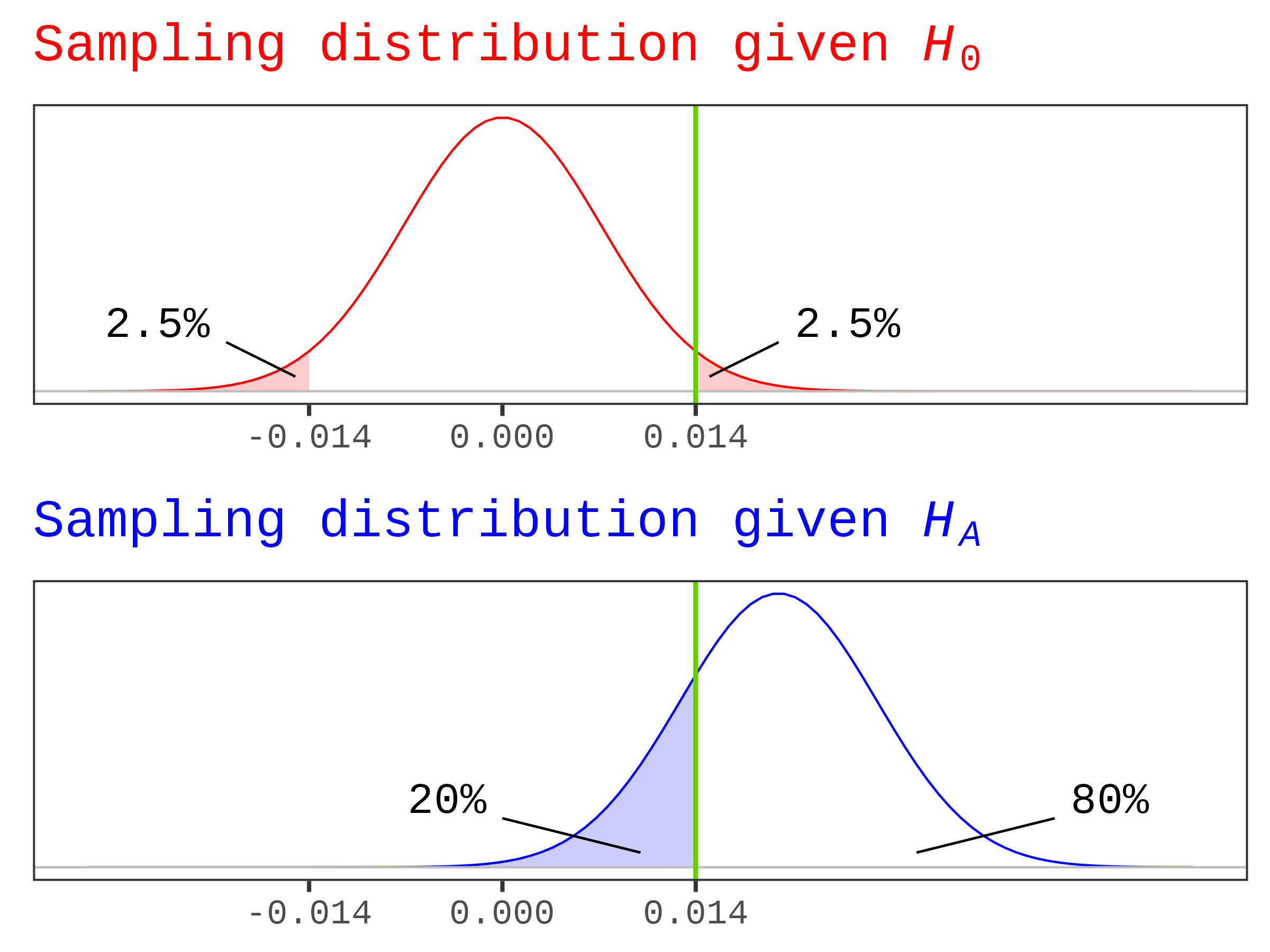

I also determine the a priori critical value (= 1.4%):

prop_pooled <- (prop_baseline+prop_treatment)/2

se_h0 <- sqrt(prop_pooled * (1-prop_pooled) * (1/n + 1/n))

se_ha <- sqrt((prop_baseline*(1-prop_baseline))/n +

(prop_treatment*(1-prop_treatment))/n)

critical_value <- qnorm(alpha / 2, mean = 0, sd = se_h0,

lower.tail = FALSE)

critical_value

# [1] 0.0139930354339993

We can visualize the sampling distributions for both hypotheses like so:

At the conclusion of the test, the results are:

The a priori decision framework:

The effect size (= 0.0154) is greater than the critical value (= 0.0140).

And so, the p-value < 0.05:

2*(1 - pnorm(0.01536376, mean = 0, sd = se_h0))

# [1] 0.0314007090609361

So, we reject the null hypothesis in favor of the alternate hypothesis.

The a posteriori decision framework:

The p-value > 0.05:

prop.test(x=c(141, 175), n=c(n,n))$p.value

# [1] 0.0540496200600176

So, we DO NOT reject the null hypothesis.

What's the correct approach?