You can solve this with techniques from The magic money tree problem which is about a single player/gambler, but you can consider the bank as the opponent player.

Different is that in your case the win probability between two players is different, whereas in the link case the payout between two players is different. Yet the techniques are the same like using a martingale or expressing the distribution as a normal distribution that spreads like a diffusion process.

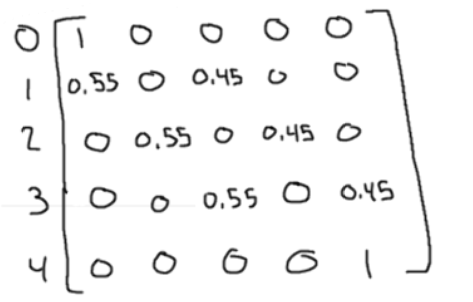

If you want to solve your problem with your transition matrix then you can write a little computer program that solves the evolution of the game and the probabilities to be in a particular state.

You might also solve this considering an itterative scheme like is used here: The Dead Drunk Man

Let's define p(n) the probability for the player A to ever reach the $n+1$ dollars state when they currently have $n$ dollars (and the game ends at 0 or 20). Then

$$p(n) = 0.45 + 0.55p(n) p(n-1)$$

or

$$p(n) = \frac{ 0.45}{1- 0.55 p(n-1)} $$

and we have $p(1) = 0.45$, because after a loss in that state the game ends and there is no return. With this you can compute all $p$ and use a product to compute the probability to ever reach 20 dollars starting from 10 dollars.

Another approach in that post is the use of simulations.

So this gives you 5 approaches

- Martingale.

- normal approximation and diffusion (actually not easy with two absorption boundaries).

- Compute Markov chain for a very long time.

- Use an itterative scheme relating different probabilities.

- Run several simulations