I tried to solve this myself:

1) Discrete Time Markov Chain

A) First Step Analysis:

Let us consider a discrete-time Markov chain with state space $S = \{0, 1, 2, ..., N\}$ and transition probabilities $P_{ij} = P(X_{n+1} = j | X_n = i)$, where $X_n$ is the state at time $n$.

The concept of Absorption Time is closely related to the Hitting Time - i.e. when is the first time when the Markov Chain enters a certain state, conditional on it being in some state at some initial time.

Let's denote $T_i$ as the hitting time of state $N$, given that we started from state $i$, i.e., the first time the process reaches state $N$ when it starts from state $i$. We want to find $E[T_i]$, the expected hitting time. Or more generally, we can calculate this for starting in any state with respect to some initial distribution:

$$\pi = ( \pi_0, ..., \pi_{N-1})$$

It makes sense to write this as weighted sum of expectations [$\pi_i$ is the initial probability of starting in state $i$, i.e. $\pi_i$ is an element in the $\pi = ( \pi_0, ..., \pi_{N-1})$ vector].

The expected hitting time to state $j$, considering the initial distribution, can be calculated as (need to solve this system of equations):

$$E[T_j] = \sum_{i=1}^{n} \pi_i (1 + \sum_{k \neq j} P_{ik} E_k[T_j])$$

where:

- $\pi_i$ is the initial probability of being in state $i$,

- $P_{ik}$ is the transition probability from state $i$ to state $k$, and

- $E_k[T_j]$ is the expected hitting time to state $j$ starting from state $k$.

- note: if you want to do the analysis conditional on starting in a specific state (e.g. state 1), this is equivalent to an initial distribution with probability 1 of being in that state and all other probabilities are 0, i.e. $\pi = (1,0,0,...)$

I think the absorption probabilities can be expressed in the same way. The expected absorption probability to state $j$, considering the initial distribution, can be calculated as (need to solve this system of equations):

$$\phi_j = \sum_{i=1}^{n} \pi_i (P_{ij} + \sum_{k \neq j} P_{ik} \phi_k)$$

where:

- $\pi_i$ is the initial probability of being in state $i$,

- $P_{ij}$ is the transition probability from state $i$ to state $j$, and

- $\phi_k$ is the absorption probability to state $j$ starting from state $k$.

B) Fundamental Matrix Approach:

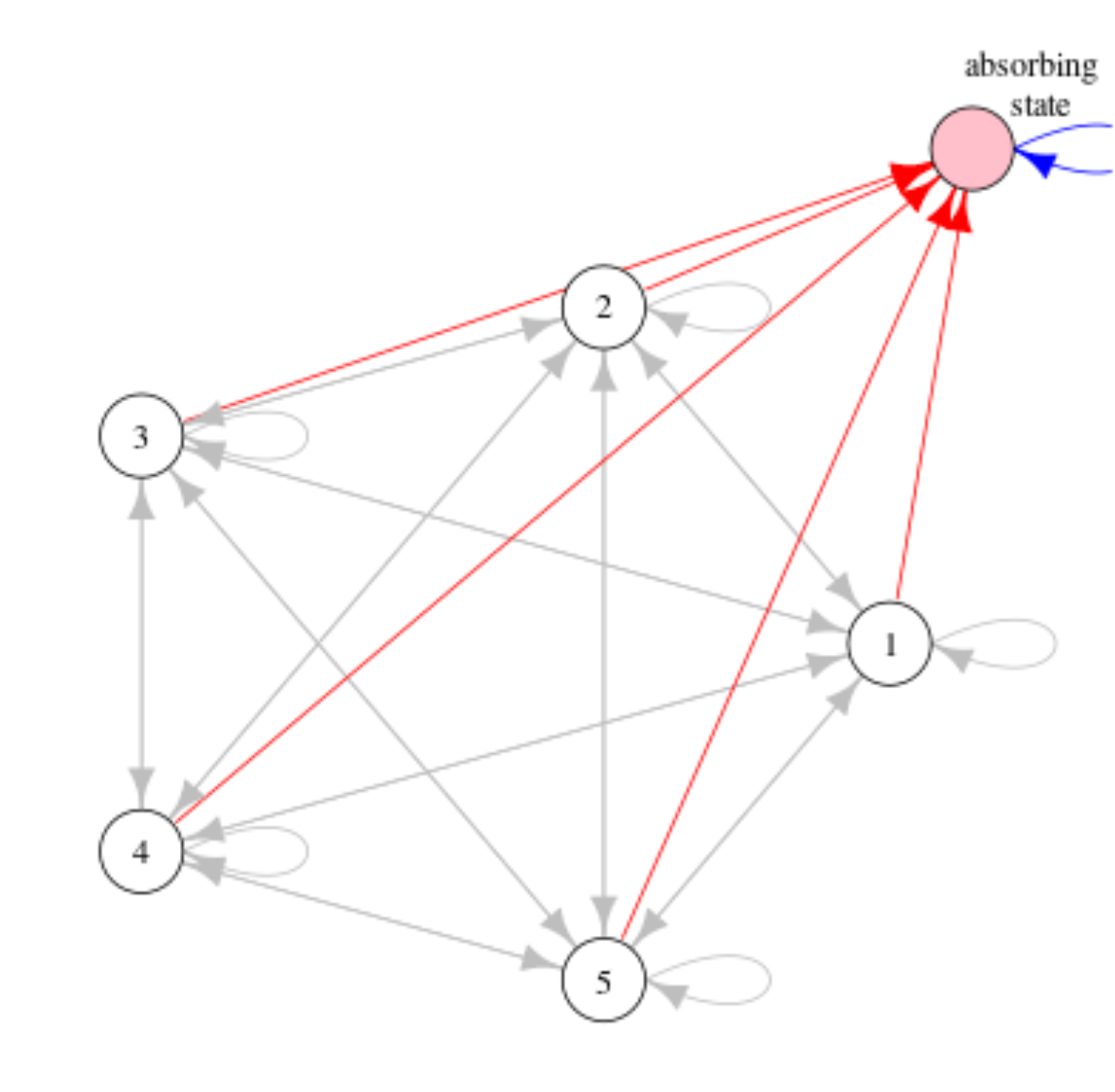

In a Discrete Time Markov Chain, all transition matrices (with an absorption state) can be re-written in the following form. For example, suppose we have a 5 state Markov Chain where the 5th state is an Absorbing State:

$$

P = \begin{bmatrix}

p_{11} & p_{12} & p_{13} & p_{14} & p_{15} \\

p_{21} & p_{22} & p_{23} & p_{24} & p_{25} \\

p_{31} & p_{32} & p_{33} & p_{34} & p_{35} \\

p_{41} & p_{42} & p_{43} & p_{44} & p_{45} \\

0 & 0 & 0 & 0 & 1

\end{bmatrix}

$$

We can re-write this matrix as:

$$ P =

\begin{bmatrix}

\color{red}{Q} & \color{blue}{R} \\

\color{green}{0} & I

\end{bmatrix} =

\begin{bmatrix}

p_{11} & p_{12} & p_{13} & p_{14} & p_{15} \\

p_{21} & p_{22} & p_{23} & p_{24} & p_{25} \\

p_{31} & p_{32} & p_{33} & p_{34} & p_{35} \\

p_{41} & p_{42} & p_{43} & p_{44} & p_{45} \\

0 & 0 & 0 & 0 & 1

\end{bmatrix} =

\begin{bmatrix}

p_{11} & p_{12} & p_{13} & p_{14} & | & p_{15} \\

p_{21} & p_{22} & p_{23} & p_{24} & | & p_{25} \\

p_{31} & p_{32} & p_{33} & p_{34} & | & p_{35} \\

p_{41} & p_{42} & p_{43} & p_{44} & | & p_{45} \\

- & - & - & - & - & - \\

0 & 0 & 0 & 0 & | & 1

\end{bmatrix} =

\begin{bmatrix}

\color{red}{p_{11}} & \color{red}{p_{12}} & \color{red}{p_{13}} & \color{red}{p_{14}} & \color{blue}{p_{15}} \\

\color{red}{p_{21}} & \color{red}{p_{22}} & \color{red}{p_{23}} & \color{red}{p_{24}} & \color{blue}{p_{25}} \\

\color{red}{p_{31}} & \color{red}{p_{32}} & \color{red}{p_{33}} & \color{red}{p_{34}} & \color{blue}{p_{35}} \\

\color{red}{p_{41}} & \color{red}{p_{42}} & \color{red}{p_{43}} & \color{red}{p_{44}} & \color{blue}{p_{45}} \\

\color{green}{0} & \color{green}{0} & \color{green}{0} & \color{green}{0} & \color{black}{1}

\end{bmatrix}

$$

- The red entries represent the $Q$ matrix (transitions between transient states).

- The blue entries represent the $R$ matrix (transitions from transient states to the absorbing state).

- The green entries represent the $0$ matrix (no transitions from the absorbing state to a transient state).

- The black entry represents the $I$ matrix (once the process enters the absorbing state, it stays there with probability

Based on this, we can observe the following pattern:

$$

P^2 = P \cdot P = \begin{bmatrix}

Q & R \\

0 & I

\end{bmatrix} \cdot \begin{bmatrix}

Q & R \\

0 & I

\end{bmatrix} = \begin{bmatrix}

Q^2 + R \cdot 0 & Q \cdot R + R \cdot I \\

0 \cdot Q + I \cdot 0 & 0 \cdot R + I \cdot I

\end{bmatrix} = \begin{bmatrix}

Q^2 & Q \cdot R + R \\

0 & I

\end{bmatrix}

$$

$$

P^3 = P^2 \cdot P = \begin{bmatrix}

Q^2 & Q \cdot R + R \\

0 & I

\end{bmatrix} \cdot \begin{bmatrix}

Q & R \\

0 & I

\end{bmatrix} = \begin{bmatrix}

(Q^2 \cdot Q) + ((Q \cdot R + R) \cdot 0) & (Q^2 \cdot R) + ((Q \cdot R + R) \cdot I) \\

(0 \cdot Q) + (I \cdot 0) & (0 \cdot R) + (I \cdot I)

\end{bmatrix} = \begin{bmatrix}

Q^3 & Q^2 \cdot R + Q \cdot R + R \\

0 & I

\end{bmatrix}

$$

$$

P^4 = P^3 \cdot P = \begin{bmatrix}

Q^3 & Q^2 \cdot R + Q \cdot R + R \\

0 & I

\end{bmatrix} \cdot \begin{bmatrix}

Q & R \\

0 & I

\end{bmatrix} = \begin{bmatrix}

(Q^3 \cdot Q) + ((Q^2 \cdot R + Q \cdot R + R) \cdot 0) & (Q^3 \cdot R) + ((Q^2 \cdot R + Q \cdot R + R) \cdot I) \\

(0 \cdot Q) + (I \cdot 0) & (0 \cdot R) + (I \cdot I)

\end{bmatrix} = \begin{bmatrix}

Q^4 & Q^3 \cdot R + Q^2 \cdot R + Q \cdot R + R \\

0 & I

\end{bmatrix}

$$

$$

P^k = \begin{bmatrix}

Q^k & (I + Q + Q^2 + .... + Q^{k-1}) R \\

0 & I

\end{bmatrix}

$$

In the $P^k$ case, we can see that :

$\lim_{{k \to \infty}} Q^k = 0$ . This is because $Q$ is a matrix of probabilities (i.e. numbers between 0 and 1), thus repeatedly raising these numbers to increasing powers will bring them closer to 0.

$I + Q + Q^2 + .... + Q^{k-1}$ is a Geometric Series:

$\text{If } 0 \leq x < 1, \text{ then } \sum_{n=0}^{\infty} x^n = 1 + x + x^2 + x^3 + ... = \frac{1}{1-x}$

Thus, $I + Q + Q^2 + .... + Q^{k-1}$ can be written as : $(I-Q)^{-1} = \frac{I}{I-Q}$

Let's call define $N = (I-Q)^{-1}$

We can define the "Fundamental Matrix" as : $$N = (I - Q)^{-1}$$ .

This matrix tells us the number of steps that the Markov Chain spends in transient states, i.e. each element in the Funfamental Matrix $N$ can be thought of as $N_{i,j} = E(T_{i,j})$

Now, we can again write (these formulas make sense practically, but I not am completely sure why they are true):

- Expected Time until Absorption with Initial Distribution:

$$t = \sum_{i=1}^{n} \pi_i t_i = \sum_{i=1}^{n} \pi_i \sum_{j=1}^{n} N_{ij}$$

where $t_i$ is the expected time until absorption from state $i$ and $N_{ij}$ is the $(i, j)$-th entry of the fundamental matrix $N$.

- Absorption Probabilities with Initial Distribution

$$\phi_{j} = \sum_{i=1}^{n} \pi_i \phi_{ij} = \sum_{i=1}^{n} \pi_i \sum_{k=1}^{n} N_{ik} R_{kj}$$

where $\phi_{ij}$ is the probability that the chain will be absorbed in state $j$ given that it started in state $i$, $N_{ik}$ is the $(i, k)$-th entry of $N$, and $R_{kj}$ is the $(k, j)$-th entry of $R$.

Although I have not verified this myself, I think that expected times and probabilities obtained from the Fundamental Matrix approach will be equivalent to the times and probabilities obtained from the First Step Analysis (?). The main advantage being that the Fundamental matrix approach is easier to calculate compared to First Step Analysis (i.e. computing $ (I-Q)^{-1}$ is easier than solving the system of linear equations from First Step Analysis )

C) Distribution of Absorption Times

This is a very "hand-wavy" way I thought of to explain why the Distribution of Absorption Times: Absorption depends on:

- the initial conditions of the Markov Chain

- the probabilities of going from the initial conditions to the non-absorbing part of the Markov Chain (and remaining in the non-absorbing part of the Markov Chain)

- the probabilities of moving from the non-absorbing part of the Markov Chain to the absorbing part of the Markov Chain

Thus, if we want to find out the probability of being absorbed in $k$ steps -

this is equivalent to spending $k-1$ steps in the non-absorbing part of the Markov Chain ($Q$) and $1$ step in the absorbing part of the Markov Chain ($R$). Using the notation from the Fundamental Matrix, we can write the probability distribution of being absorbed in $k$ steps (i.e. $k = k -1 + 1$):

$$\sum_{k=1}^{n} P(K=k) = \pi_0 \cdot \sum_{k=1}^{n} \cdot Q^{k-1} \cdot R^1$$

And we can see that the above formula is in the same form as the formula provided here https://math.stackexchange.com/questions/3281928/what-is-the-distribution-of-time-to-absorption-for-an-absorbing-markov-chain (i.e. Discrete Phase Type Distribution). I am not sure how to calculate the variance of this distribution yet.

2) Continuous Time Markov Chains

I will try to keep this short. Define the basics equations of a Continuous Time Markov Chain (Here $Q$ is not referring to the same thing as in the Fundamental Matrix used in the Discrete Markov Chain above).

- Rate Matrix (note: for all absorbing states $i$, the associated rate $q_{i,}$ will be 0 by definition - this is because there is no emission from an absorbing state):

$$

Q_{ij} =

\begin{bmatrix}

q_{11} & q_{12} & \cdots & q_{1m} \\

q_{21} & q_{22} & \cdots & q_{2m} \\

\vdots & \vdots & \ddots & \vdots \\

q_{m1} & q_{m2} & \cdots & q_{mm}

\end{bmatrix}

$$

$$q_{ii} = -\sum_{\substack{j=1 \\ j \neq i}}^{m} q_{ij}$$

- Kolmogorov Equation

$$

\lim_{{t \to 0}} \frac{{P_{ij}(t)}}{t} =

\begin{cases}

q_i & \text{if } i = j \\

q_{ij} & \text{if } i \neq j

\end{cases}

$$

$$\frac{dP(t)}{dt} = P(t)Q$$

$$P(t) = P(t=0) \cdot e^{Qt}$$

$$\exp(Qt) = \sum_{n=0}^{\infty} \frac{(Qt)^n}{n!} = I + Qt + \frac{1}{2!} Q^2t^2 + \frac{1}{3!} Q^3t^3 + \ldots$$

- Embedded Discrete Jump Process:

Holding Rates: $\lambda_i = \lambda_1, \lambda_2, ... \lambda_m$, such that $\lambda_i = \sum_{j} q_{ij}$

(Exponential) Distribution of Holding Times (i.e. Memoryless Property): $f_T(t) = \lambda_i e^{-\lambda_i t}$

Jump Process Probabilities: $P_{ij} = \frac{q_{ij}}{\sum_{j} q_{ij}}$

As an example, for a 4 state Continuous Time Markov Chain with one absorbing state, we can write:

$$

Q = \begin{bmatrix}

-q_{11} & q_{12} & q_{13} & q_{14} \\

q_{21} & -q_{22} & q_{23} & q_{24} \\

q_{31} & q_{32} & -q_{33} & q_{34} \\

0 & 0 & 0 & 0

\end{bmatrix}

= \left[\begin{array}{ccc|c}

-q_{11} & q_{12} & q_{13} & q_{14} \\

q_{21} & -q_{22} & q_{23} & q_{24} \\

q_{31} & q_{32} & -q_{33} & q_{34} \\

\hline

0 & 0 & 0 & 0

\end{array}\right]$$

$$T = \begin{bmatrix}

-q_{11} & q_{12} & q_{13} \\

q_{21} & -q_{22} & q_{23} \\

q_{31} & q_{32} & -q_{33} \\

\end{bmatrix}$$

$$r = -T \cdot \mathbf{1} = \begin{bmatrix}

q_{14} \\

q_{24} \\

q_{34} \\

\end{bmatrix}$$

$$

Q = \begin{bmatrix}

T_{n \times n} & r_{n \times 1} \\

0 & 0

\end{bmatrix}

$$

As is typically done in Continuous Time Markov Chains, we want to use the Rate Matrix $Q$ to determine the time dependent probabilities of transitioning between states (via the Kolmogorov Equation).

Using the expansion $\exp(Qt) = \sum_{n=0}^{\infty} \frac{(Qt)^n}{n!} = I + Qt + \frac{1}{2!} Q^2t^2 + \frac{1}{3!} Q^3t^3 + \ldots$, we should be able to compactly write (I haven't verified this, its from the youtube video in the references) the Kolmogorov Equation as ($\pi_0$ is the initial distribution):

$$

\pi(t) = \pi_0 \left[ I + \begin{bmatrix} Tt & rt \\ 0 & 0 \end{bmatrix} + \frac{1}{2!} \begin{bmatrix} (Tt)^2 + Ttrt & 0 \\ 0 & 0 \end{bmatrix} + \frac{1}{3!} \begin{bmatrix} (Tt)^3 & (Tt)^2 rt \\ 0 & 0 \end{bmatrix} + \ldots \right]

$$

$$

\pi_(t) = \pi_0 \left\{ I_{n \times n} + \begin{bmatrix} \left(Tt + \frac{(Tt)^2}{2!} + \frac{(Tt)^3}{3!} + \ldots\right) & \left(rt + Tt \cdot rt + (Tt)^2 \cdot rt + \ldots\right) \\ 0 & 0 \end{bmatrix} \right\}

$$

$$\pi(t) = \pi_0 \left\{ \begin{bmatrix}

1 & 0 & \cdots & 0 \\

0 & 1 & \cdots & 0 \\

\vdots & \vdots & \ddots & \vdots \\

0 & 0 & \cdots & 1

\end{bmatrix}_{n \times n} + \begin{bmatrix} \left(Tt + \frac{(Tt)^2}{2!} + \frac{(Tt)^3}{3!} + \ldots\right) & \left(rt + Tt \cdot rt + (Tt)^2 \cdot rt + \ldots\right) \\ 0 & 0 \end{bmatrix} \right\}

$$

$$

\pi_(t) = \pi_0 \left\{ \begin{bmatrix} \left(1+ Tt + \frac{(Tt)^2}{2!} + \frac{(Tt)^3}{3!} + \ldots\right) & \left(rt + Tt \cdot rt + (Tt)^2 \cdot rt + \ldots\right) \\ 0 & 0 \end{bmatrix} \right\}

$$

$$ \pi_(t) = \pi_0 e^{Qt} =

\pi_0 \cdot \begin{bmatrix}

\sum_{k=0}^{\infty} \frac{(Tt)^k}{k!} & \sum_{k=1}^{\infty} \frac{T^{(k-1)} (t^k) r}{k!} \\

0 & 1

\end{bmatrix}

$$

$$e^{Tt} = \sum_{k=0}^{\infty} \frac{(Tt)^k}{k!}$$

Again, the top left of this matrix refers to transition rates within the transient states, the top right of this matrix refers to transition rates between transient to absorbing states, and the bottom left/right refer to the activity of the Markov Chain once within the absorbing states (i.e. 0 emission rates)

Finally, let's define the initial distribution $\pi_0 = [\alpha, 0]$, where $\alpha = (\alpha_1, \alpha_2, ...., \alpha_m)$ itself is a sub-vector for the probabilities of being in the set of all $m$ number of non-absorbing state at time=0. After some more manipulation (have not fully confirmed this yet), we can define:

The probability of being in any state at time=t (note: this vector should sum to 1, since it contains probabilities):

$$\pi(t) = \begin{bmatrix} \alpha e^{Tt} \quad , \quad 1 - \alpha e^{Tt} \end{bmatrix}$$

Thus, the probability distribution of being absorbed at time = t

$$\Pi(t) = 1 - \alpha e^{Tt}$$

However, the variance still remains unknown to me.

Conclusion: Thus after much struggle and heartache, I have tried to understand parts of the analysis needed to derive the probability distributions of the absorption times in Discrete Time Markov Chains and Continuous Time Markov Chains. I am open to any feedback/criticism and would love to hear all thoughts and ideas.

References: