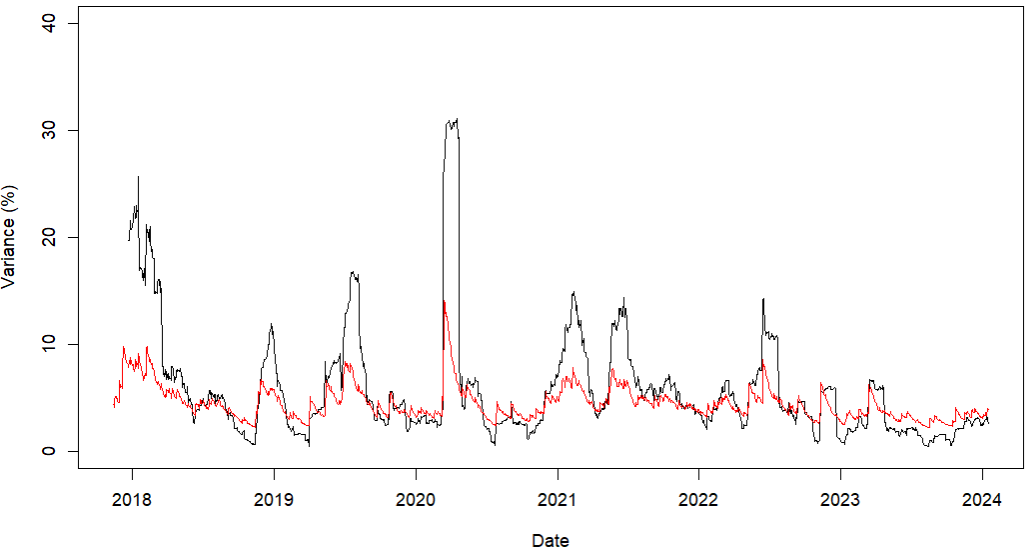

I estimated the variance of Bitcoin in several ways using the var command in R, and within a GARCH model. I get series that look a bit similar, but the y-axis gives different results. Is this normal?

Here, the variance is estimated within a GARCH model (in red) and as the realized variance (in black), i.e the sum of past squared returns (over 30 days).

var, this is not the sum of past squared returns, it is the variance of past returns. $\endgroup$varmeasure is even more different with the GARCH modelized variance ! $\endgroup$