I would like to generate a synthetic dataset where there are multiple records per ID, and self-consistency is maintained among records of each ID.

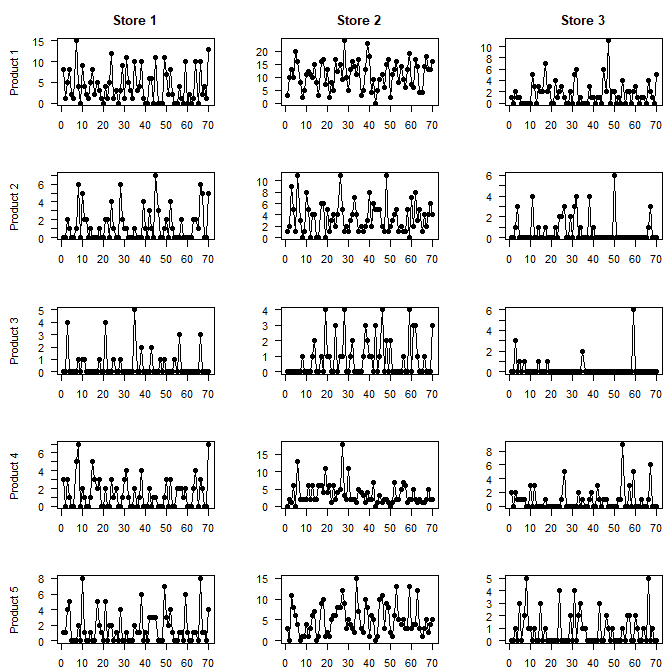

For example, imagine a dataset where the ID is a grocery store, and each record is the sales of various items for that store in a given day. In other words, multiple time series. You can imagine that while there are global trends across all stores, there are also store-level trends, and a realistic dataset must preserve not just global trends, but also store-level trends. Perhaps store A sells more chips on weekends, while store B sells less chips on weekends but more cookies.

A synthetic data model which samples fake records IID would only preserve the global trend of sales ("chips generally sell more than cookies on Fridays"). A model which is another step up in complexity, such as an LSTM, may preserve temporal trends which express across all stores ("if cookies sold less than chips at time t-1, they will sell generally more at time t"). But how would I make a model that also allows these trends to vary per-store ("chips generally outsell cookies on Saturdays at certain stores, but the opposite is true at other stores")?

One idea I had is to use domain-knowledge / clustering to assign stores to one of N "profiles," then use that profile as a feature. The model would naturally be able to capture the dependency. That said, this approach requires manual definition of N and creates a finite set of profiles. I am looking for something less limiting and which can detect more subtle profiles than I may be able to manually, if it exists.

Hopefully I've explained my problem well enough - feel free to ask for clarification. Links to relevant papers would be greatly appreciated. Thank you!