I have two random variables $s\sim \mathcal{N}(\nu,\sigma)$ and $a\sim \mathcal{U}(0,A)$, $0<A<1$, calculate a third r.v. $t=(1-a)/s$ and want to find its distribution $p(t|\nu,\sigma,A)$.

My reasoning is, that for any value of $a$, there is exactly one $s=(1-a)/t$ such that the $(a,s)$ pair will produce $t$ and I will therefore have to integrate over the probabilities for these values:

$$p(t|\nu,\sigma,A) = \int_0^A p_a(x)p_s((1-x)/t)\,\mathrm dx\\$$

which can be expressed as the sum of two error functions.

But already when checking this step numerically, I get a discrepancy between estimated (by sampling) and calculated distribution:

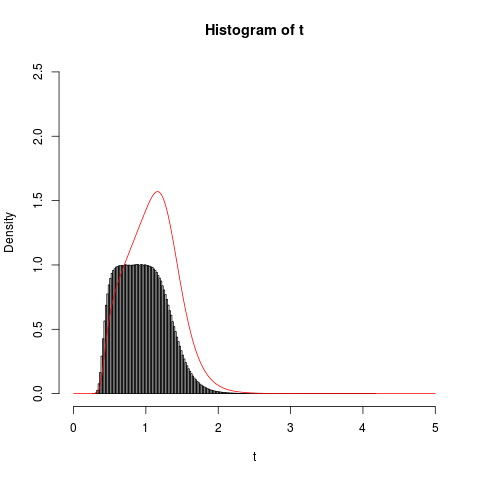

*Why do the histogram and the calculated distribution do not match?*

This is the code I used:

n=10000000

A=0.7

nu=.7

sigma=.1

# sampling from the target distribution

s=rnorm( n, mean=nu, sd=sigma )

a=runif( n, min=0, max=A )

t=(1-a)/s

hist(t,200, freq=F, xlim=c(0,5), ylim=c(0,2.5))

# plot the analytical result

analytic <- function(t, A, nu, sigma ){

tmp <- function(x, A, t, nu, sigma){

return (1/A*dnorm( (1-x)/t, mean=nu, sd=sigma) )

}

return( integrate( tmp, 0, A, A=A, t=t, nu=nu, sigma=sigma)$value)

}

x=seq(0,5,by=.01)

y=rep(0,length(x))

for( i in seq(1,length(x)) ){

y[i]=analytic(x[i], A, nu, sigma)

}

lines( x, y, col="red", type="l")