MASS, the book (4th edition, page 110) advicesadvises against trying to estimate $\nu$, the degrees of freedom parameter in the t distribution$t$-distribution with maximum likelihood (with some literature references: Lange et al. (1989), "Robust statistical modeling Using the t distribution", JASA, 84, 408, and Fernandez & Steel (1999), "Multivariate Student-t regression models: Pitfalls and inference", Biometrika, 86, 1).

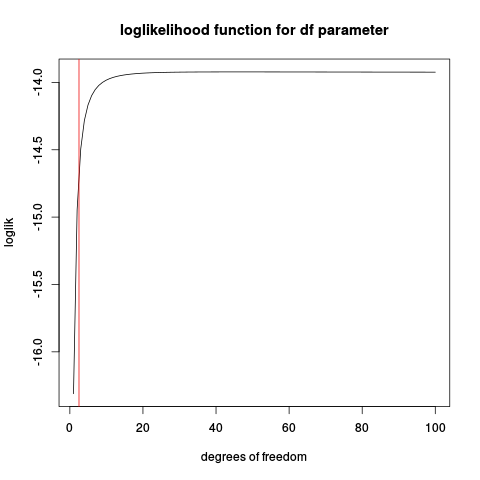

The reason is that the likelihood function for $\nu$ based on the t density function, may be unbounded! and will in those cases not give a well defined maximum. LetLet us seelook at an artificial example where location and scale is known (as the standard $t$-distribution) and only the degrees of freedom is unknown. BelowBelow is some R code, simulating some data, defining the loglikelihoodlog-likelihood function and plotting it:

set.seed(1234)

n <- 10

x <- rt(n, df=2.5)

make_loglik <- function(x)

Vectorize( function(nu) sum(dt(x, df=nu, log=TRUE)) )

loglik <- make_loglik(x)

plot(loglik, from=1, to=100, main="loglikelihood function for df parameter", xlab="degrees of freedom")

abline(v=2.5, col="red2")

If you play around with this code, you can find some cases where there is a well-defined maximum, especially withwhen the sample size $n$ is large. But is the maximum likelihood estimator then any good?

Let us try some simulations:

t_nu_mle <- function(x) {

loglik <- make_loglik(x)

res <- optimize(loglik, interval=c(0.01, 200), maximum=TRUE)$maximum

res

}

nus <- replicate(1000, {x <- rt(10, df=2.5)

t_nu_mle(x) }, simplify=TRUE)

> mean(nus)

[1] 45.20767

> sd(nus)

[1] 78.77813

Showing the estimation is very unstable (looking at the histogram, a sizeablesizable portion of the estimated values is at the upper limit given to optimize of 200).

Repeating with a larger sample size:

nus <- replicate(1000, {x <- rt(50, df=2.5)

t_nu_mle(x) }, simplify=TRUE)

> mean(nus)

[1] 4.342724

> sd(nus)

[1] 14.40137

which is much better, but the mean is stilstill way above the true value of 2.5.

Then remember that this is a simplified version of the real problem whenwhere location and scale parameters also have to be estimated.

If the reason of using the $t$-distribution is to "robustify", then estimating $\nu$ from the data well may well destroy the robustness.