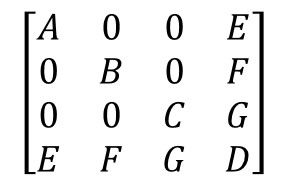

I have a sparsepostive definite symmetric covariance matrix which looks like this:

A 0 0 e

0 B 0 f

0 0 C g

h l m D

(All letters Note that all A,B,C,D,E,F,G are also poitive definite symmetric covariance matrices.)

Is there a closed form solution for I want to find an easy way were I can invert the matrix in parts instead of inverting such matrices? And if not, does R have a function for fast inversionall of such sparse matrices?it at one time. I would really appreciate an R code or any method in R that can solve my problem My main goal here is to find an efficient-fast way to invert this matrix and find its determinant