My question builds on a previous postprevious post on outlier detection in generic time series, and specifically on the answer provided by the always great Rob H.

I work for a small-sized manufacturing company that currently handles the issue, i.e. detecting outliers in sales data time series, employing a (dubious) automated off-the-shelf software procedure.

I think this kind of approach is questionable at best and, more often than not, I'm not happy with the results I get. I would therefore like to "double check" the output from our software using some alternative method.

Rob's idea seemed reasonable, straightforward and easy to implement, so I decided to give it a try. Question is: what if my time series are not "generic"?

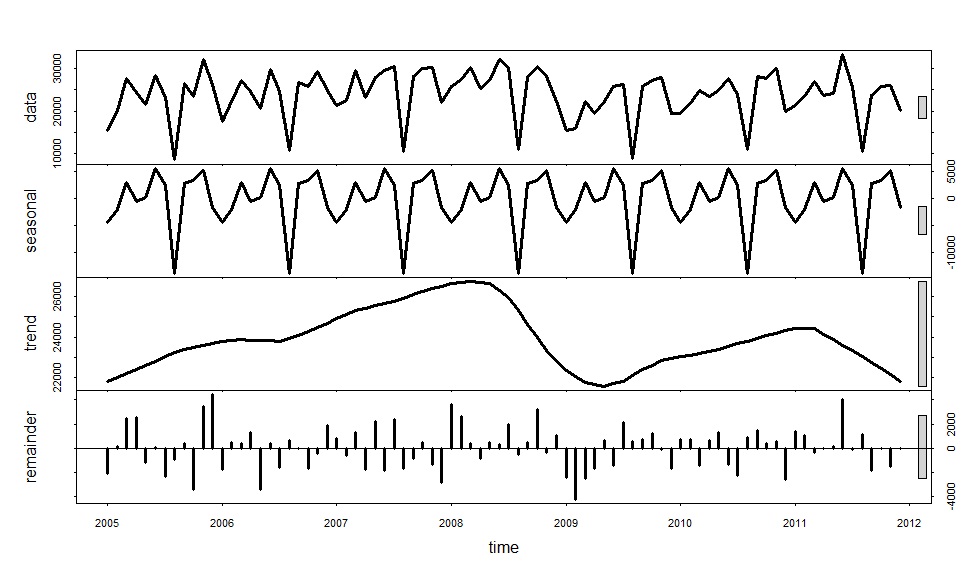

Stl decomposition highlights a strong seasonality and a varying trend in my data:

(BTW I used stl(x,s.window="periodic") like Rob suggested, but IMHO stl(x,s.window="periodic",robust=TRUE) would be a better choice since outlier detection is the issue at hand here. Also I'm not really sure about the s.window="periodic" part, I tried experimenting with different values a bit, but I don't know how to interpret results. Maybe someone can point me in the right direction?).

Back to my question, mine being sales data, the seasonal pattern is (or I think it is) strongly affected by calendar effects. Also I have reason to believe the big level shift in 2009 is due to the financial crisis and it has nothing to do with trend.

What do I do here? Should I let the model handle this, or should I pre-process data? Do I perform working-day adjustment and re-allign (is there such a thing?) before-2009 and after-2009 data, or do I let STL decomposition do the work?

I could write another 1000 lines, but I think this should be enough to get the message through. I apologize for the WOT and for my bad english. Also I hope I did not break too many forum rules...

I hope someone out there can help!