So what we did with the code is as follows. First, we have created a time-series example (from the ARIMA model). After that we have decoupled/sliced the time-series example into inputs of the form (sw previous points, next point) for all pairs except the last one (with the next point as the last point of the time-series example). The parameter sw is used to define the "sliding window". I won't debate here what is the proper size for the sliding-window but just note that due to Elman networks having memory the sliding-window of size one is more than a reasonable approach (also, take a look at this postpost).

replaced http://stats.stackexchange.com/ with https://stats.stackexchange.com/

library(RSNNS)

#

# simulate an arima time series example of the length n

#

set.seed(10001)

n <- 100

ts.sim <- arima.sim(list(order = c(1,1,0), ar = 0.7), n = n-1)

#

# create an input data set for ts.sim

# sw = sliding-window size

#

# the last point of the time series will not be used

# in the training phase, only in the prediction/validation phase

#

sw <- 1

X <- lapply(sw:(n-2),

function(ind){

ts.sim[(ind-sw+1):ind]

})

X <- do.call(rbind, X)

Y <- sapply(sw:(n-2),

function(ind){

ts.sim[ind+1]

})

# used to validate prediction properties

# on the last point of the series

newX <- ts.sim[(n-sw):(n-1)]

newY <- ts.sim[n]

# build an elman network besdbased on the input

model <- elman(X, Y,

size = c(10, 10),

learnFuncParams = c(0.001),

maxit = 500,

linOut = TRUE)

#

# plot the results

#

limits <- range(c(Y, model$fitted.values))

plot(Y, type = "l", col="red",

ylim=limits, xlim=c(0, length(Y)),

ylab="", xlab="")

lines(model$fitted.values, col = "green", type="l")

points(length(Y)+1, newY, col="red", pch=16)

points(length(Y)+1, predict(model, newdata=newX),

pch="X", col="green")

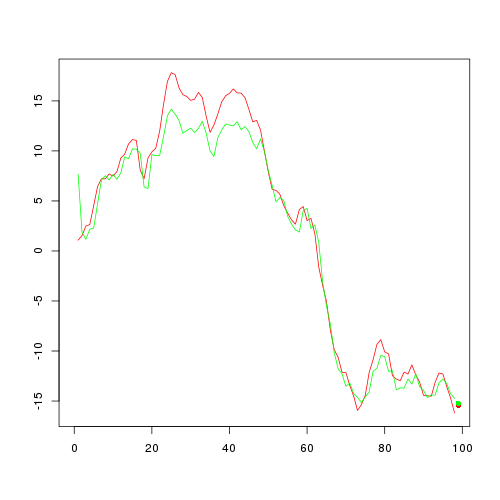

This code should resultsresult in the following figure

library(RSNNS)

#

# simulate an arima time series example of the length n

#

set.seed(10001)

n <- 100

ts.sim <- arima.sim(list(order = c(1,1,0), ar = 0.7), n = n-1)

#

# create an input data set for ts.sim

# sw = sliding-window size

#

# the last point of the time series will not be used

# in the training phase, only in the prediction/validation phase

#

sw <- 1

X <- lapply(sw:(n-2),

function(ind){

ts.sim[(ind-sw+1):ind]

})

X <- do.call(rbind, X)

Y <- sapply(sw:(n-2),

function(ind){

ts.sim[ind+1]

})

# used to validate prediction properties

# on the last point of the series

newX <- ts.sim[(n-sw):(n-1)]

newY <- ts.sim[n]

# build an elman network besd on the input

model <- elman(X, Y,

size = c(10, 10),

learnFuncParams = c(0.001),

maxit = 500,

linOut = TRUE)

#

# plot the results

#

limits <- range(c(Y, model$fitted.values))

plot(Y, type = "l", col="red",

ylim=limits, xlim=c(0, length(Y)),

ylab="", xlab="")

lines(model$fitted.values, col = "green", type="l")

points(length(Y)+1, newY, col="red", pch=16)

points(length(Y)+1, predict(model, newdata=newX),

pch="X", col="green")

This code should results in the following figure

library(RSNNS)

#

# simulate an arima time series example of the length n

#

set.seed(10001)

n <- 100

ts.sim <- arima.sim(list(order = c(1,1,0), ar = 0.7), n = n-1)

#

# create an input data set for ts.sim

# sw = sliding-window size

#

# the last point of the time series will not be used

# in the training phase, only in the prediction/validation phase

#

sw <- 1

X <- lapply(sw:(n-2),

function(ind){

ts.sim[(ind-sw+1):ind]

})

X <- do.call(rbind, X)

Y <- sapply(sw:(n-2),

function(ind){

ts.sim[ind+1]

})

# used to validate prediction properties

# on the last point of the series

newX <- ts.sim[(n-sw):(n-1)]

newY <- ts.sim[n]

# build an elman network based on the input

model <- elman(X, Y,

size = c(10, 10),

learnFuncParams = c(0.001),

maxit = 500,

linOut = TRUE)

#

# plot the results

#

limits <- range(c(Y, model$fitted.values))

plot(Y, type = "l", col="red",

ylim=limits, xlim=c(0, length(Y)),

ylab="", xlab="")

lines(model$fitted.values, col = "green", type="l")

points(length(Y)+1, newY, col="red", pch=16)

points(length(Y)+1, predict(model, newdata=newX),

pch="X", col="green")

This code should result in the following figure