So, after some research on the topic... I came to realise that if you execute the following code:

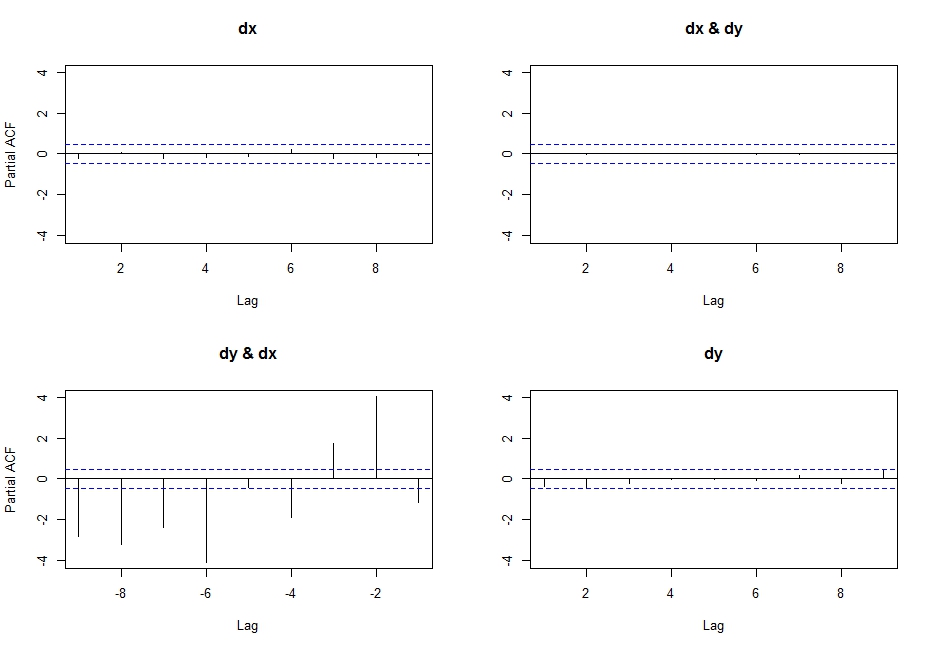

pacf(ts(cbind(dx,dy)),lag.max=10)

You get the partial cross correlations between x & y.

So I researched a little, and found this link where Simone Giannerini creates a corrected version of the multivariate pacf. Here is the code:

pacf.mts <- function(x,lag.max){

## Partial autocorrelation function for multivariate time series

## implements a generalization of the Durbin-Levinson Algorithm

## as described in

## Wei(1990) Time Series Analysis, Univariate and Multivariate methods

## Addison Wesley.

## Simone Giannerini 2007

# The author of this software is Simone Giannerini, Copyright (c) 2007

# Permission to use, copy, modify, and distribute this software for any

# purpose without fee is hereby granted, provided that this entire notice

# is included in all copies of any software which is or includes a copy

# or modification of this software and in all copies of the supporting

# documentation for such software.

# This program is free software; you can redistribute it and/or modify

# it under the terms of the GNU General Public License as published by

# the Free Software Foundation; either version 2 of the License, or

# (at your option) any later version.

#

# This program is distributed in the hope that it will be useful,

# but WITHOUT ANY WARRANTY; without even the implied warranty of

# MERCHANTABILITY or FITNESS FOR A PARTICULAR PURPOSE. See the

# GNU General Public License for more details.

#

# A copy of the GNU General Public License is available at

# http://www.r-project.org/Licenses/

nser <- ncol(x);

snames <- colnames(x)

alpha.c <- array(0,c(nser, nser,lag.max,lag.max));

beta.c <- array(0,c(nser, nser,lag.max,lag.max));

P <- array(0,c(lag.max, nser, nser));

cov.x <- acf(x,plot=FALSE,type="covariance",lag.max=lag.max)$acf;

Vu <- array(0,dim=c(nser,nser,lag.max));

Vv <- Vu;

Vvu <- Vu;

Vu[,,1] <- cov.x[1,,]; ## Gamma[0]

Vv[,,1] <- cov.x[1,,]; ## Gamma[0]

Vvu[,,1] <- cov.x[2,,]; ## Gamma[1]

alpha.c[,,1,1] <- t(Vvu[,,1])%*%solve(Vv[,,1])

beta.c[,,1,1] <- Vvu[,,1]%*%solve(Vu[,,1])

Du <- diag(sqrt(diag(Vu[,,1])),nser,nser);

Dv <- diag(sqrt(diag(Vv[,,1])),nser,nser);

P[1,,] <- solve(Dv)%*%Vvu[,,1]%*%solve(Du);

if(lag.max>=2) {

for(s in 2:lag.max) {

dum.u <- 0;

dum.v <- 0;

dum.vu <- 0;

for(k in 1:(s-1)) {

dum.u <- dum.u + alpha.c[,,s-1,k]%*%cov.x[(k+1),,];

dum.v <- dum.v + beta.c[,,s-1,k]%*%t(cov.x[(k+1),,]);

dum.vu<- dum.vu + cov.x[(s-k+1),,]%*%t(alpha.c[,,s-1,k]);

}

Vu[,,s] <- cov.x[1,,] - dum.u;

Vv[,,s] <- cov.x[1,,] - dum.v;

Vvu[,,s] <- cov.x[(s+1),,] - dum.vu;

alpha.c[,,s,s] <- t(Vvu[,,s])%*%solve(Vv[,,s]);

beta.c[,,s,s] <- Vvu[,,s]%*%solve(Vu[,,s]);

for(k in 1:(s-1)) {

alpha.c[,,s,k] <- alpha.c[,,s-1,k]-alpha.c[,,s,s]%*%beta.c[,,s-1,s-k]

beta.c[,,s,k] <- beta.c[,,s-1,k] - beta.c[,,s,s]%*%alpha.c[,,s-1,s-k]

}

Du <- diag(sqrt(diag(Vu[,,s])),nser,nser);

Dv <- diag(sqrt(diag(Vv[,,s])),nser,nser);

P[s,,] <- solve(Dv)%*%Vvu[,,s]%*%solve(Du);

}

}

colnames(P) <- snames;

return(P)}

Which follows the recursive algorithm described in pp. 402-414 in Wei (2005) Time Series Analysis, and actually yields the same output as the first line of code I wrote above (probably the pacf function was corrected on CRAN after he posted this new function)

I think this is what I am looking for, but why isn't it called partial cross correlation, if that's what it (seems) to be?

WARNING:

I realised that doing:

pacf(cbind(dx,dy))

Yields highly undesirable results (do not understand what actually happens here, but it is certainly wrong... probably has something to do with the input class not being a ts?), after getting this output: