Not necessarily as untreated pulses , level shifts , seasonal pulses or local time trends can severely downwards bias the acf of the model errors leading to an incorrect conclusion that the error process is white noise .

This erroneous conclusion can also be reached if the model parameters or model error variance is not homogeneous through time.

If you post your data I will try to help you further.

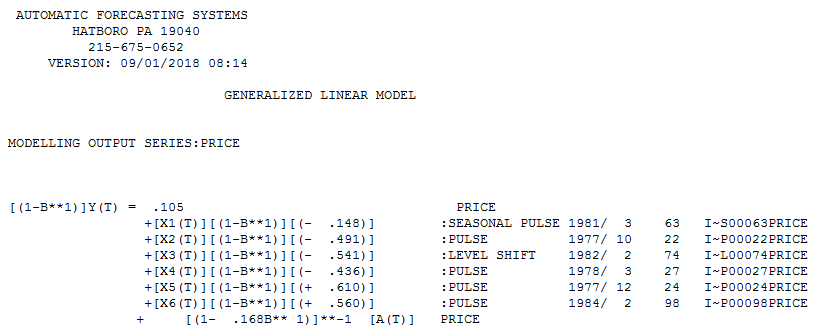

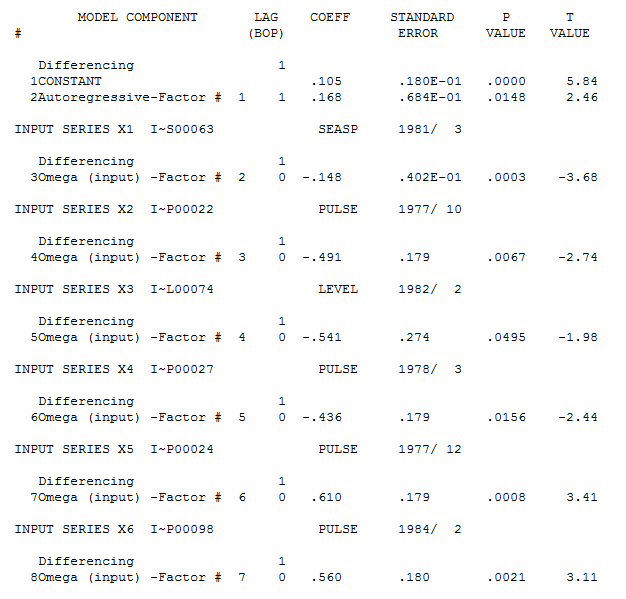

Arima modelling is a sequence of self-checking proceedures designed to extract a minimally sufficient signal and a companion noise process free of evidented structure. Your data (216 monthly values) can be easily described by a (1,1,0) arima structure , 4 pulses ( periods 22.24.27 and 98 ) , 1 intercept change at period 74 , 1 seasonal pulse starting at period 63 (1981/3) and 1 error variance change (down) at period 128 culminating in a GLS model.

The model is here  and here

and here

Arima models like you describe (8,1,8) are artifacts from an incomplete analysis and are fundamentally laughable. The reason EVIEWS fails is because it does not deal with the model in a holistic manner. See my comment and other threads in response to How to determine order of sarima?

Power transforms do not detrend and should only be employed under certain conditions When (and why) should you take the log of a distribution (of numbers)?.

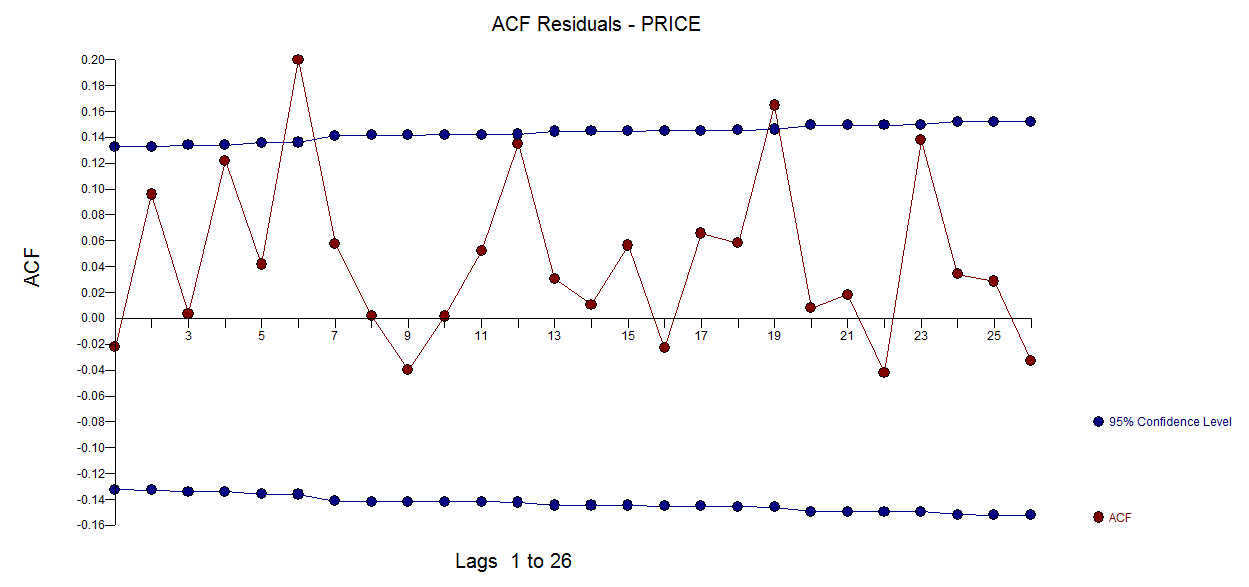

The acf of the model residuals is here

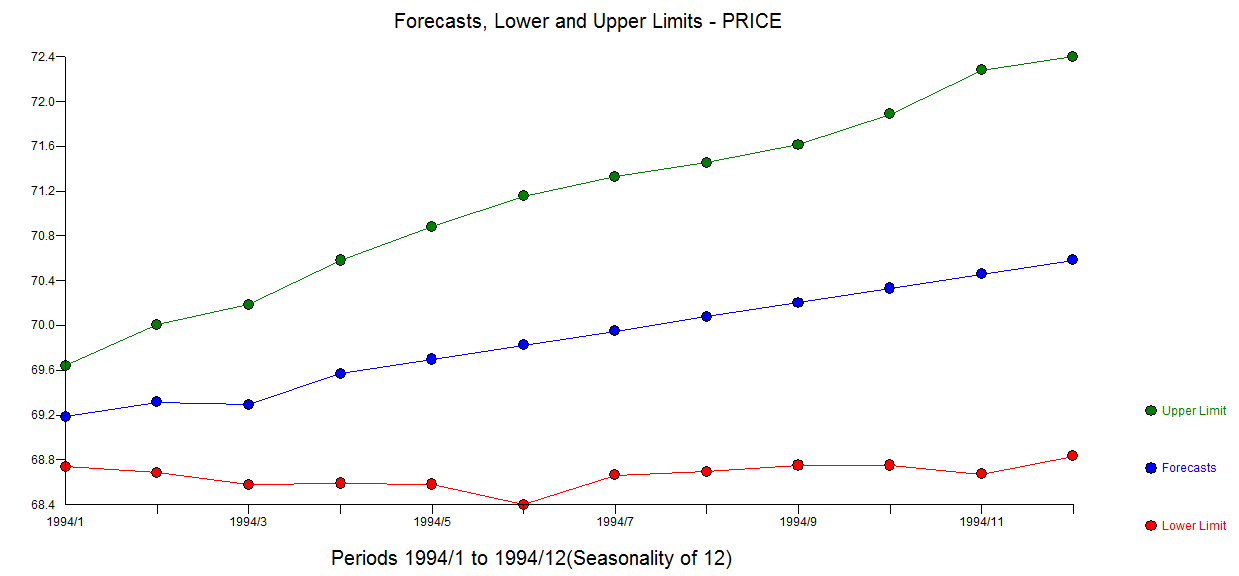

and forecasts with confidence limits are here  . using monte-carlo simulation (bo0tstrap) where future anomalies are explicitely allowed for.

. using monte-carlo simulation (bo0tstrap) where future anomalies are explicitely allowed for.

Finally the confidence limits around acf/pacf are VERY VERY VERY approximate as they are purely based on the sample size (+/- t/sqrt(216 where t is the normal deviate) and should not be over-believed.

Another way to answer this question .. is for you to post your residuals and to see if model structure can be found/verified.