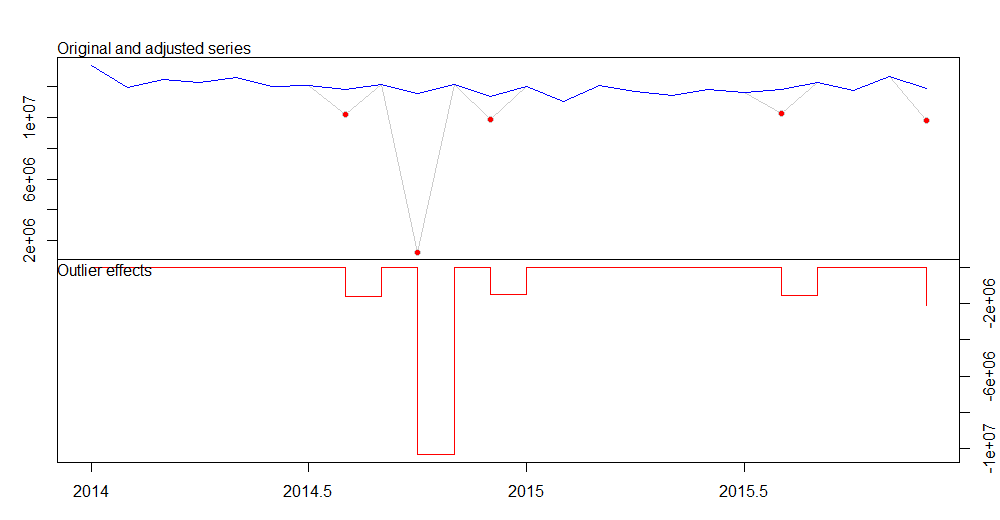

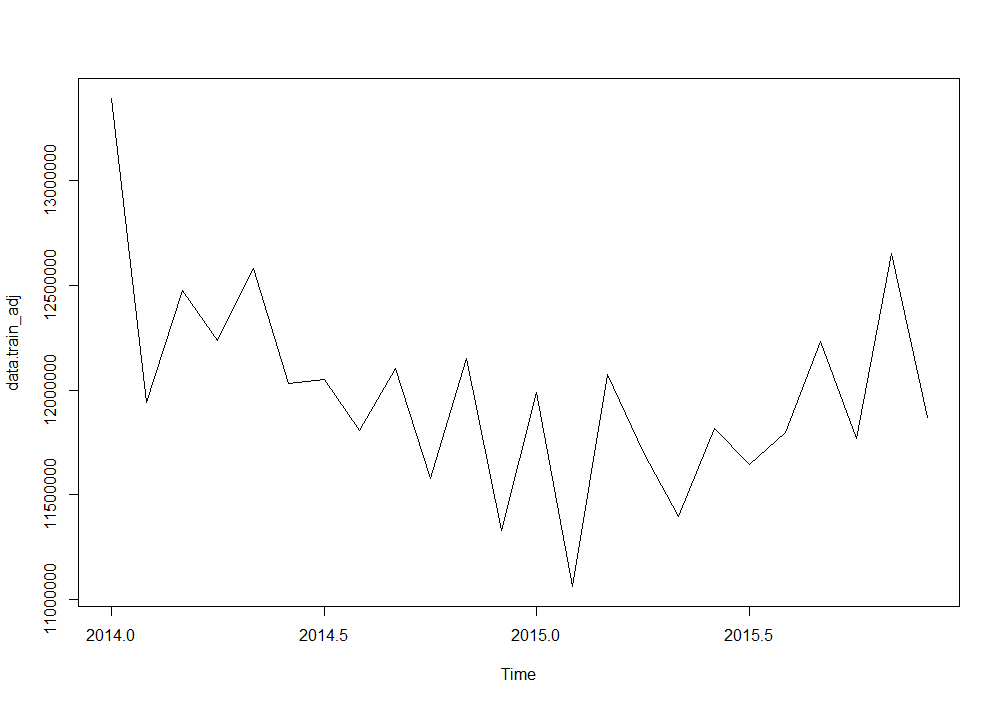

This is the outliers adjusted time series.

data.train_adj <- tso_res$yadj

plot(data.train_adj)

We can see both data.train and data.train_adj.

> data.train

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 13392905 11939873 12473667 12237110 12579693 12030095 12052101 10205025 12102526 1237336 12148331 9842860

2015 11990085 11061740 12076397 11702514 11395657 11817594 11643682 10243241 12233001 11769231 12652418 9774333

> data.train_adj

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2014 13392905 11939873 12473667 12237110 12579693 12030095 12052101 11807296 12102526 11576627 12148331 11329957

2015 11990085 11061740 12076397 11702514 11395657 11817594 11643682 11795494 12233001 11769231 12652418 11869616

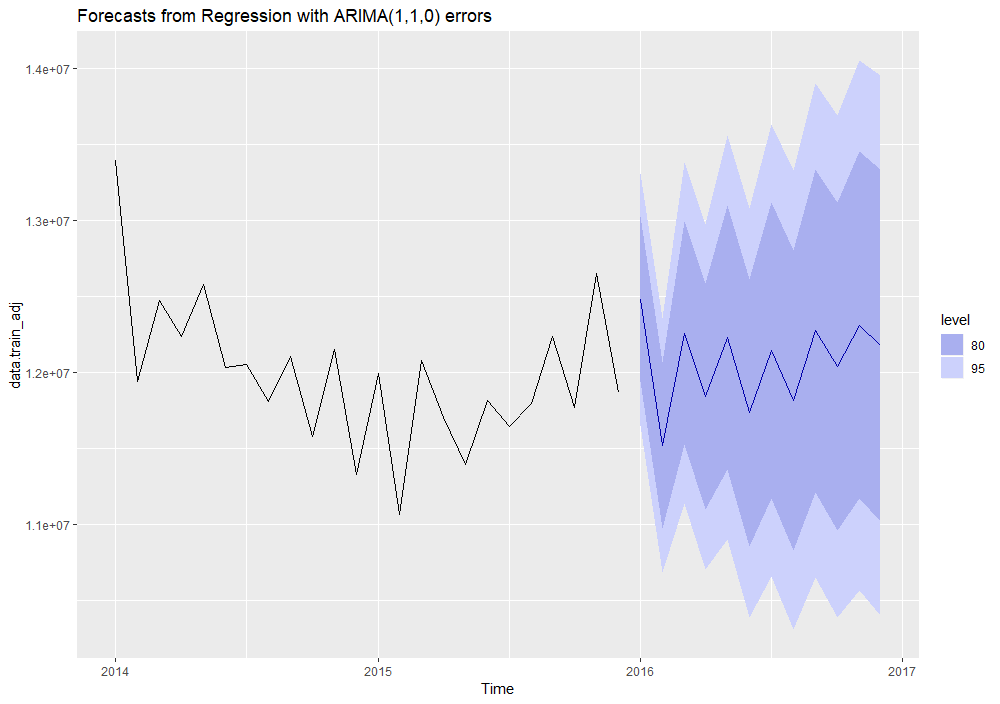

To accomplish with your need to capture seasonality, I take advantage of dynamic harmonic regression within ARIMA modeling. You may determine an optimal number of Fourier sin and cos pairs number (K) by trying out a pool of values for and select the one with minimum AICc. Here I show it with K=4. Please note that Fourier coefficients are actually not statistically significative as their standard deviations compaired to the coefficients value show.