I

I

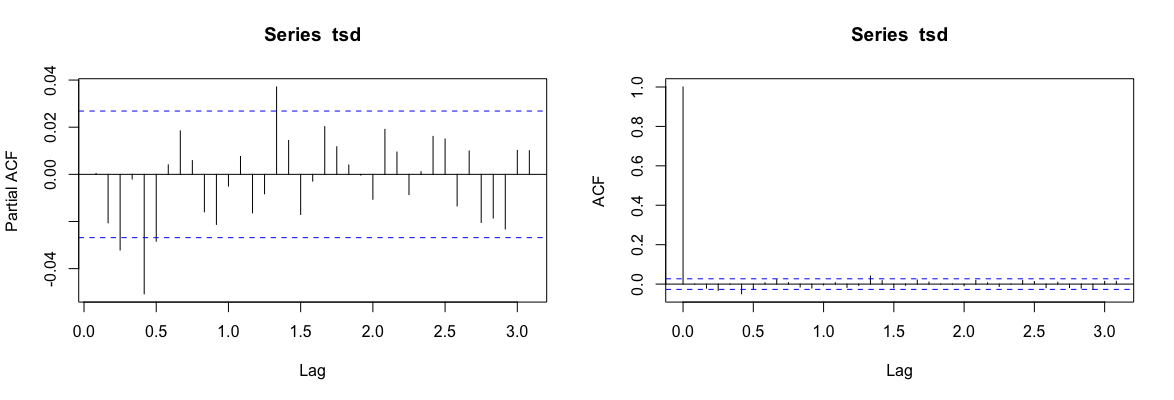

I have converted the stock price indicesindex time series data into stationary series by differencing once so, so $d=1$. I also have removed the seasonal component of the data. I want to develop a model for forecasting future values of SPX. These are PACF and ACF plots obtained. I am not able to determine the values of $p,q$ for ARIMA modeling.

I have read a little about minimum AIC values as wellwell; however, we need a rough estimate of the $p,d,q$ to make guesses towards the correct model in that as well.