As this calculation of the t-Stat does not contain a correction for the error in variables problem I looked for a Shanken (1992) adjustment on the standard error. Unfortunately many papers state, that they apply the Shanken adjustments to their t-Stats but do not include a calculation for it. I found a description for the implementation of a Shanken-adjustment adjustment (http://lipas.uwasa.fi/~sjp/Teaching/eaptx/lectures/p5.pdf - slide 41 and following). This example also includes a sample implementation of the Shanken-adjustment adjustment in Stata for a single cross-sectional regression. I used this example and transferred the calculations into Matlab-code code.

The problem now is that I am uncertain how the aggregation of periodic standard error calculations (following the Shanken-adjustments adjustments) into one standard error for the t-test happens. With a single cross-section regression there is no aggregation of values - but for the periodical cross-section regression according to Fama & MacBeth I run monthly cross-sectional regressions.

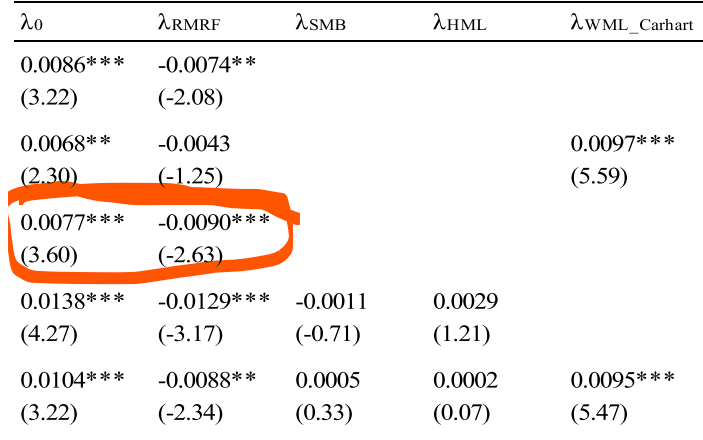

I implemented "my interpretation" of a Shanken-adjustment adjustment in a 60 month rolling regression to reconcile the results of Artmann (2011: https://www.econstor.eu/bitstream/10419/70130/1/736358048.pdf page 36, table 8, panel F) who implemented a Shanken t-stat with Fama & MacBeth-MacBeth implementation.

I can reconcile the paper's factor loadings approximately but the calculated t-stats a far off.

Whereas the paper arrives at a t-stat of 3.6 for the intercept my t-stat is only 1.28. Hence I assume my implementation of the Shanken-adjustment adjustment for the rolling beta estimation Fama/Macbeth-MacBeth procedure is faulty. My code works as follows:

Do you know how to properly implement the Shanken-adjustments adjustments for the Fama/-MacBeth approach? Many thanks!