- You say "I am aware that box-cox transformation MAY make data set significantly normal distributed with constant mean and variance."

No it simply decouples a possible relationship between the variance of the errors and the Expected value. Please read my answer to When (and why) should you take the log of a distribution (of numbers)?. It MAY generate a more normal distribution if the series is leptokurtric (fat tails)

- You say/ask "does it is always make variance and mean constant?"

Not necessarily as the error variance may change deterministically over time requiring Generalized Least Squares (Weighted least Squares see http://docplayer.net/12080848-Outliers-level-shifts-and-variance-changes-in-time-series.html ) or stochastically over time requiring a GARCH add-on.

The reason Box-Cox shows up is that in the "old bad days ! " that is all that was known or in textbooks as a way to treat heteroscedastic errors. Textbooks are out of date as soon as they get printed. SE is the true textbook because it is ever evolving to improve the craft .

Also see a number of my posts where the error variance changes and in particular Removing Variance in Time Series After Applying Log Transformation might be of interest and Box Cox Transformation makes Out of sample Forecast Error worse? .

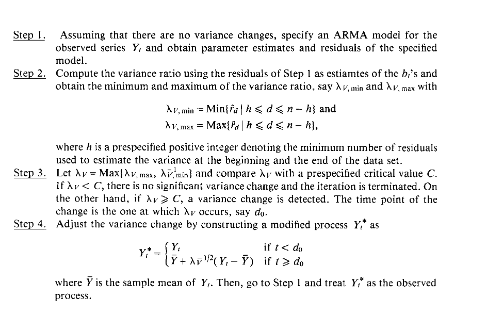

Finally an examination of why intervention detection may be more useful that a box-cox transformation. http://www.autobox.com/pdfs/vegas_ibf_09a.pdf (slide 14 + )

EDITED after remarks