I am confused with the “autocovariance” in time series. In textbooks it says that it: “measures the linear dependence between two points on the same series observed at different times”.

Why “two points”? When I see the definition of covariance it is: “measure of the tendency of two random variables to vary in the same direction“.

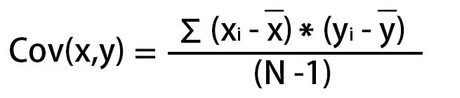

When I use covariance I do not do a calculation for "two points" I do it for all the points:

And also I do not understand the logic… I do know cov(X,X)=var(X) … And in the time series I am looking I work with only one random variable? Isn’t the “autocovariance” just the “variance”?

In stats I use covariance to know what trend X vs Y has… Positive, negative or no trend. What information the “autocovariance” gives me?

If I check the correlation on a random variable against the same random variable, it is gonna be 1, what is the benefit of calculating it on a single variable in time series? isn't it always 1?