You asked " how“how do I do this with the log-link function and quasi(Poisson) errors? )" ”. I say put aside your priors suggesting a particular fixed model and use a data-driven empirical process to identify the (possible) memory model , refining parameters and testing both necessity and sufficiency .

W hen

hen

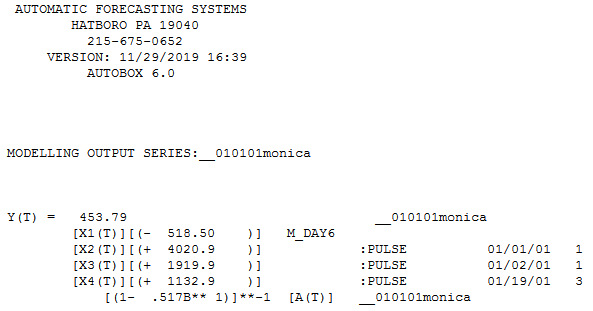

When you only have 29 days ( 44 seasons of daily data ) , I am normally reluctant to enable the automatic process to consider seasonal activity like day 6 as the OP has smartly viewed and pointed out ... a win for the human !

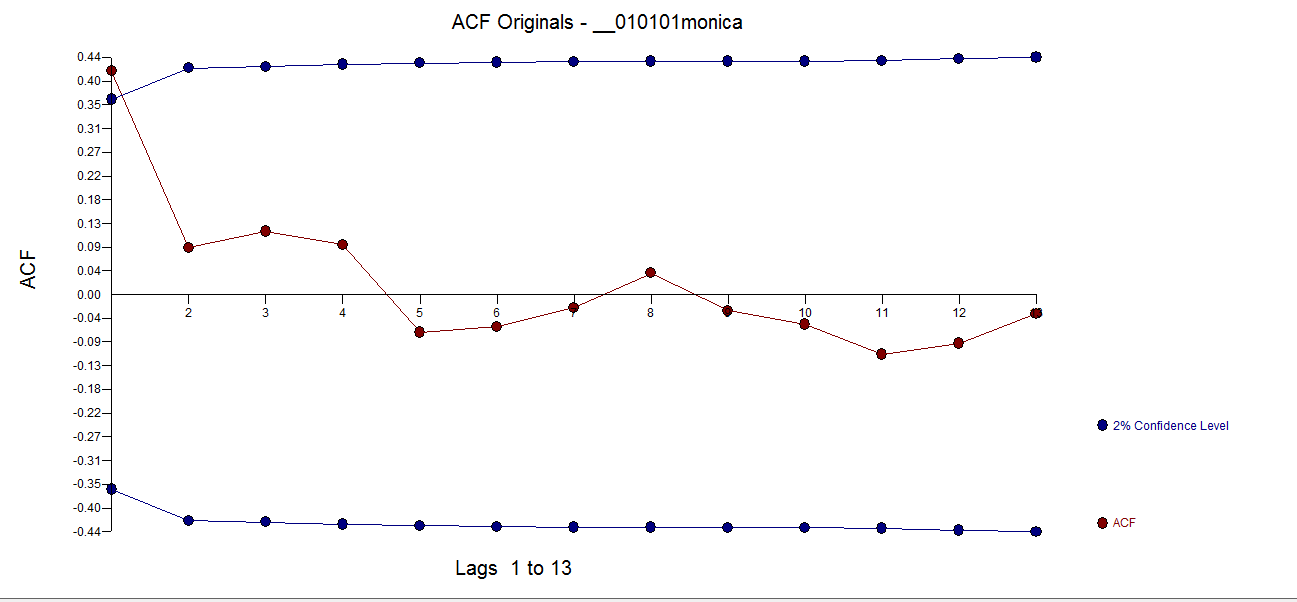

Following is the audit trail .... the ACF of the original series is here :

. I suggested the possibility of a day 6 effect to the software which then identified supported that hypothesis while detecting three unusual points while incorporating an ar(1) effect shown here and here  and the companion PACF of the original series here :

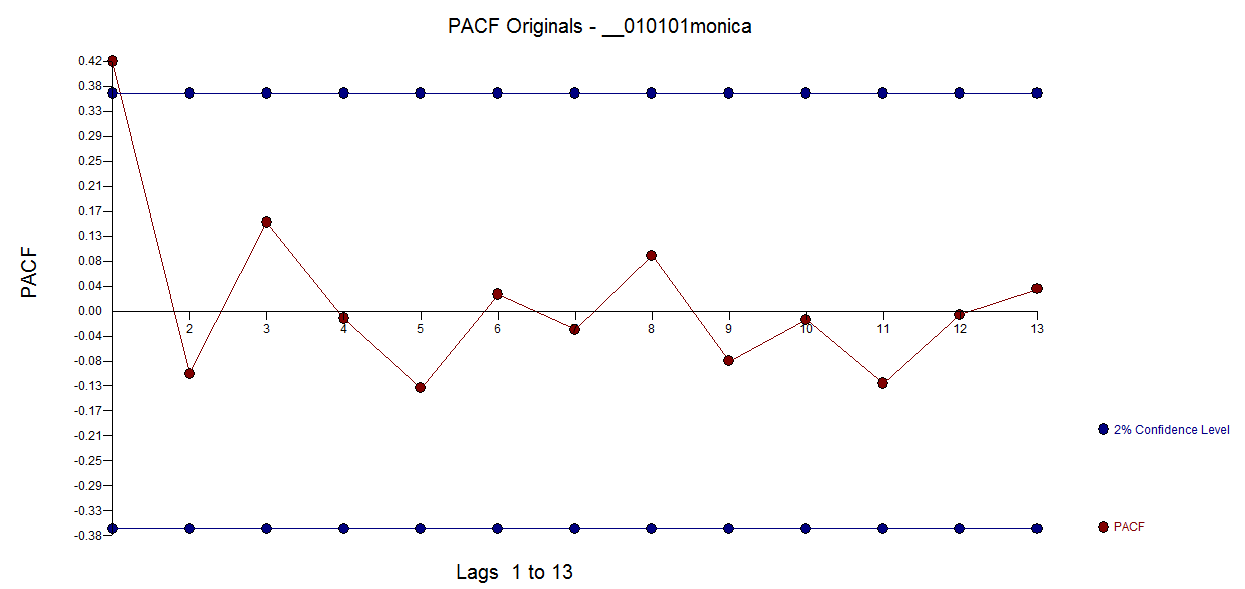

and the companion PACF of the original series here :

.

.

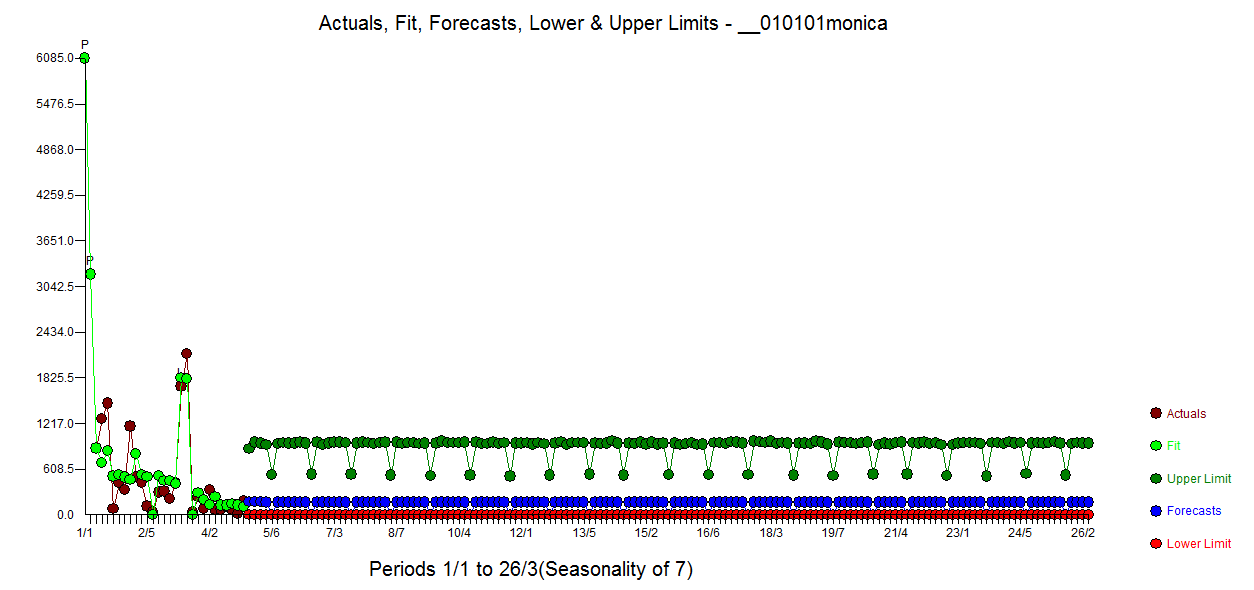

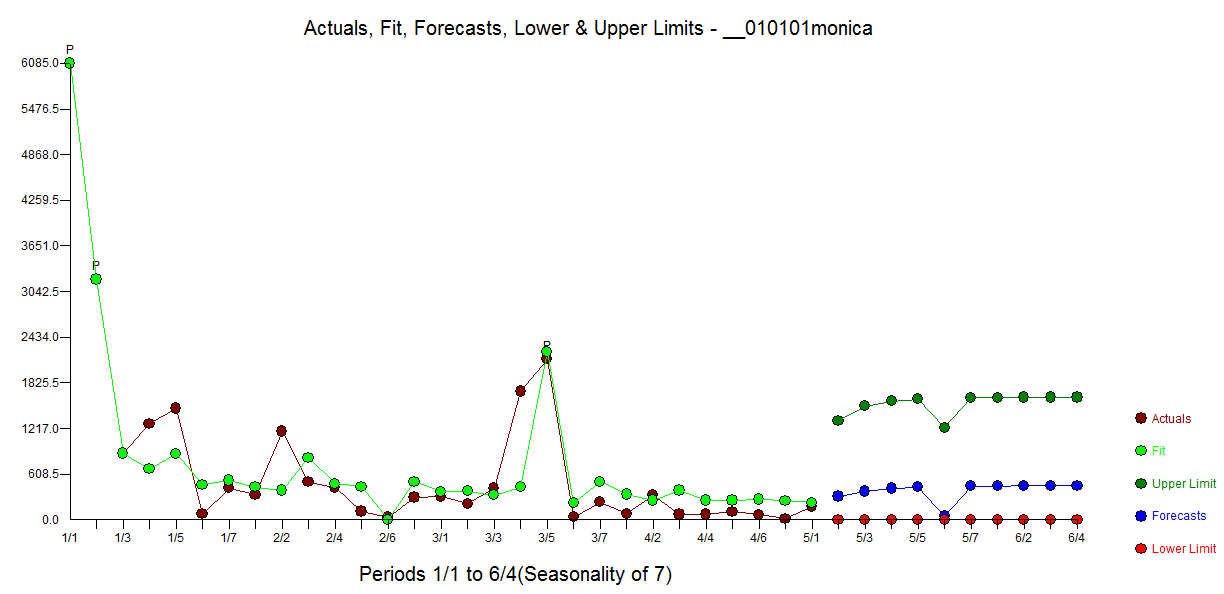

The Actual/Fit and Forecast is here :

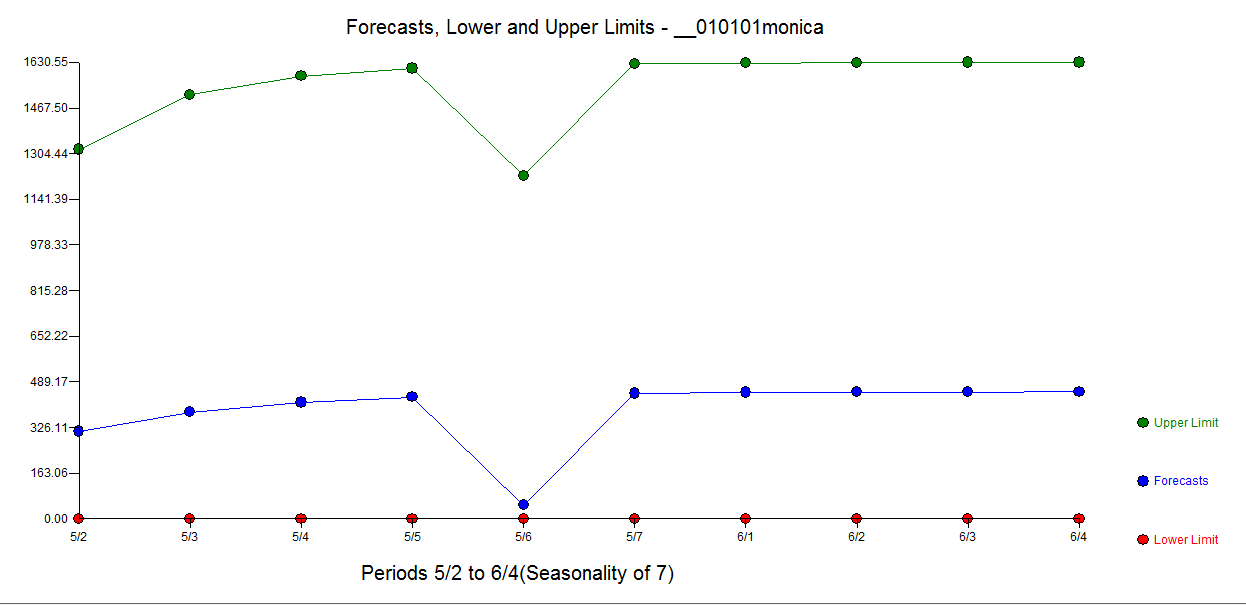

with forecasts here :

... all without assuming logarithms or any other possible unwarranted transformation.

Logs can be useful but the suggestion for a power transform for an atheoretica theoretic model should never be made based upon the original data but on the residuals from a model which is where all the assumptions are placed that need to be tested. When (and why) should you take the log of a distribution (of numbers)?

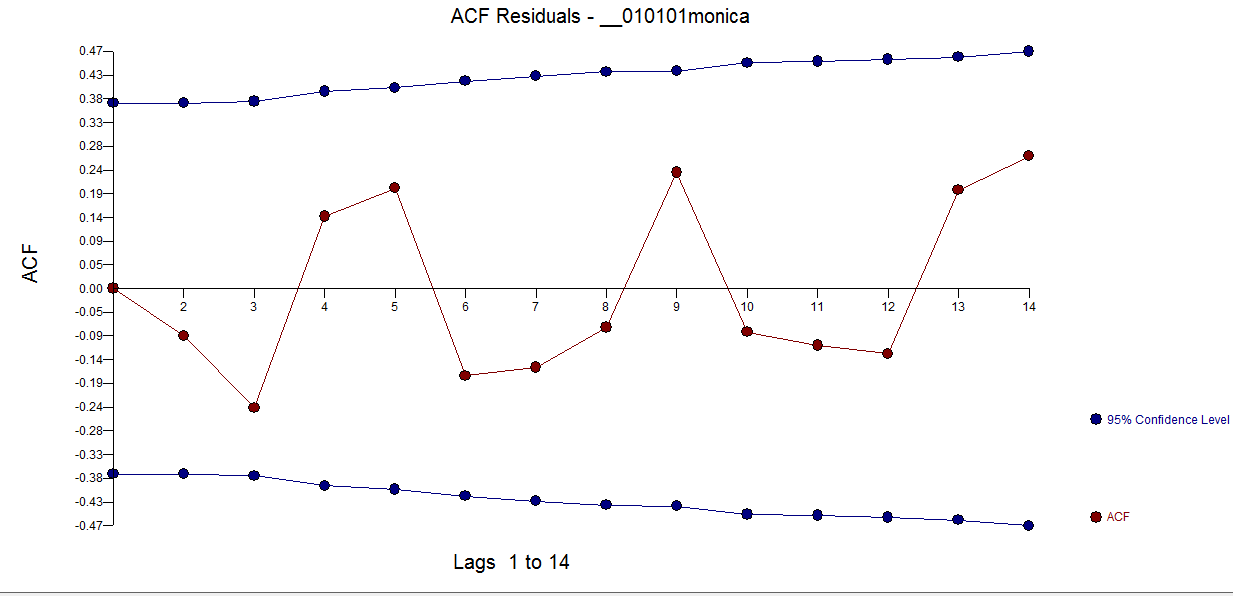

Notice the ACF of the residuals series suggesting that it that the model can not be proven to be insufficient .

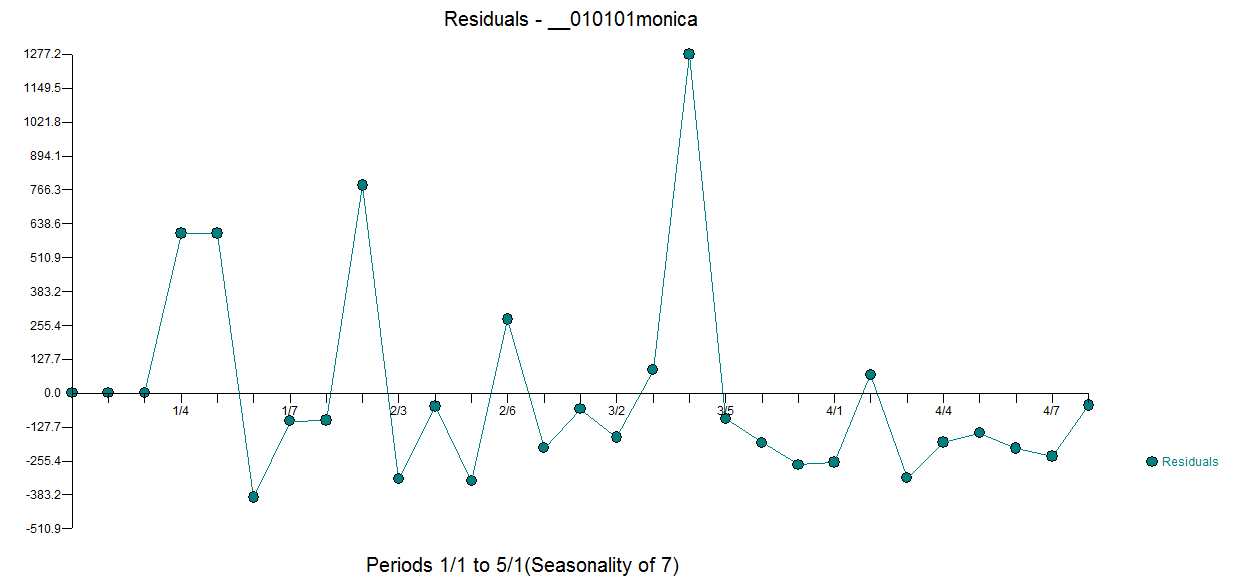

and a supporting (not quite perfect !) residual plot here :

As Isaac Asimov said "the“the only education is self-education"education” and your question is certainly in that spirit.