Update to follow-up

Let me rewrite your model one more time $$ Y_i = \beta_0 + \beta_1Z_{1i} + \beta_2 Z_{2i} + \beta_3 X_i + U_{1i} $$ where as before, $Z_{1i}$ and $Z_{2i}$ are exogenous and $X_i$ is endogenous. You assume the data generating process $$ \begin{align} Z_{2i} &= \mathbf{1}_{[i\text{ is odd}]}\\ X_i &= \alpha_0 + \alpha_1Z_{1i} + U_{2i} \end{align} $$ You introduce endogeneity by assuming that $U_{1i}$ and $U_{2i}$ are correlated. $$ \mathbb{C}(U_{1i}, U_{2i}) = \rho $$

Also, you assume that the errors in the reduced form equation are heteroskedastic: $$ \begin{align} \mathbb{V}(U_{2i}\mid Z_{2i} = 0) &= 1 \\ \mathbb{V}(U_{2i}\mid Z_{2i} = 1) &= \tfrac{1}{q} \\ \end{align} $$

Here is the Stata code to simulate this DGP.

clear*

program simcont, rclass

syntax [, Q(real 1.0)]

drop _all

set obs 1000

scalar beta0 = 5

scalar beta1 = 1

scalar beta2 = 2

scalar beta3 = 3

scalar alpha0 = 1

scalar alpha1 = 4

scalar rho = 0.1

g z1 = rnormal()

g z2 = mod(_n, 2)

scalar a11 = 1

scalar a12 = rho*sqrt(1)*sqrt(1)

scalar a13 = rho*sqrt(1)*sqrt(1/`q')

scalar a21 = rho*sqrt(1)*sqrt(1)

scalar a22 = 1

scalar a23 = 0

scalar a31 = rho*sqrt(1)*sqrt(1/`q')

scalar a32 = 0

scalar a33 = 1/`q'

mat corrMatrix= (a11, a12, a13 \ a21, a22, a23 \a31, a32, a33)

drawnorm u1 u3 u4, cov(corrMatrix)

g u2 = cond(z2, u3, u4)

g x = alpha0 + alpha1*z2 + u2

g y = beta0 + beta1*z1 + beta2*z2 + beta3*x + u1

reg y z1 z2 x

mat mA = e(b)

return scalar ols = el(mA, 1, colnumb(mA, "x"))

// return the results of the heteroskedasticity test

qui reg x z2

estat hettest, rhs iid

return scalar hettestPValues = r(p)

end

// simulate to check for heteroskedasticity

simulate olsCoeff = r(ols) hettestPValues = r(hettestPValues), reps(100): simcont, q(5)

su hettestPValues // strong evidence of heteroskedasticity in the reduced form

cap mat drop biasBeta

forvalues q = 2(1)5 {

simulate olsCoeff = r(ols), reps(1000): simcont, q(`q')

qui su olsCoeff

mat biasBeta = (nullmat(biasBeta), r(mean) - 3)

local colNames "`colNames' q:`q' "

}

mat colnames biasBeta = `colNames'

mat list biasBeta

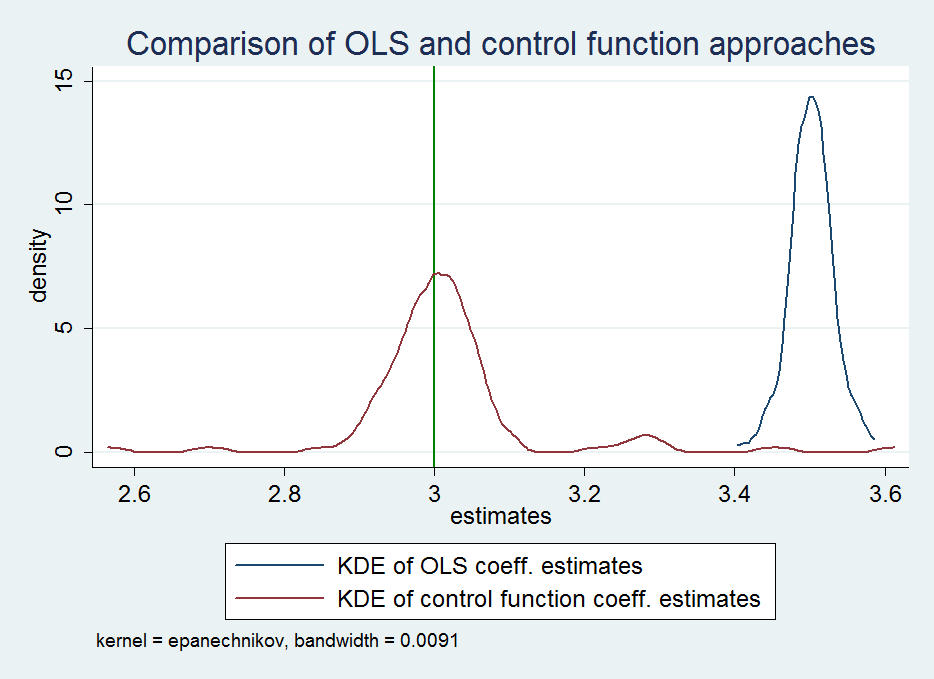

- Note that the heteroskedasticity is where you put it in the model, and the simulation results are now able to find it.

. su hettestPValues // strong evidence of heteroskedasticity in the reduced form Variable | Obs Mean Std. Dev. Min Max -------------+-------------------------------------------------------- hettestPVa~s | 100 1.53e-26 8.12e-26 3.09e-38 6.22e-25

- Also, I can confirm that what you claim is actually true, that as the heteroskedasticity in the reduced form equation increases, the bias in the OLS estimator also increases.

biasBeta[1,4] q: q: q: q: 2 3 4 5 r1 .11242463 .11808594 .12122701 .12210455

A simple explanation of this is that as $q$ increases, the conditional (on $Z_{2i}=1$) and hence the unconditional variance of the reduced form error $U_{2i}$ decreases (check through a variance decomposition) which means that the variance of the endogenous regressor decreases, which means that the $(\mathbf{X}'\mathbf{X})^{-1}$ increases in magnitude, and the overall bias increases (this is a very rough description -- I am sure it can be formalized).