The fable package replaces the hts package and produces prediction intervals. It is also much easier to handle the aggregation structure. Here is some code using the same example as in your question (updated to include multiple models).

library(tsibble)

library(feasts)

library(fable)

library(dplyr)

df <- as_tsibble(hts::htseg1$bts) %>%

mutate(

level1 = substr(key, 1, 1),

level2 = substr(key, 2, 2)

) %>%

as_tsibble(index=index, key=c(level1,level2)) %>%

select(-key) %>%

aggregate_key(level1/level2, value = sum(value))

fc <- df %>%

model(

ses = ETS(value ~ trend("N") + season("N")),

holt = ETS(value ~ trend("A") + season("N")),

arima = ARIMA(value)

) %>%

reconcile(mint

ses = min_trace(ses),

holt = min_trace(holt),

arima = min_trace(arima)

) %>%

forecast(h=10)

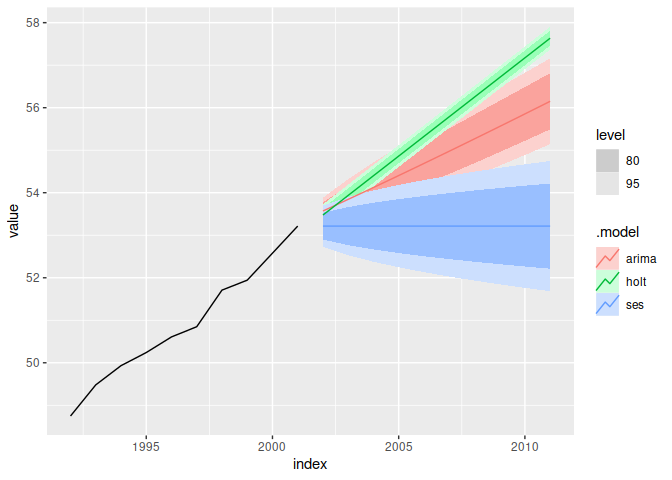

fc %>%

filter(.model=="mint", is_aggregated(level1)) %>%

autoplot(df)

fc %>%

mutate(PI = hilo(value, level=95))

#> # A fable: 160240 x 7 [1Y]

#> # Key: level1, level2, .model [16][24]

#> level1 level2 .model index value .mean PI

#> <chr*> <chr*> <chr> <dbl> <dist> <dbl> <hilo>

#> 1 A A arimases 2002 N(9.12, 0.048031) 9.1115 [8.682833807747, 9.545839]95497520]95

#> 2 A A arimases 2003 N(9.12, 0.091062) 9.0815 [8.487620664913, 9.669394]95640354]95

#> 3 A A arima ses 2004 2004 N(9.2, 0.13093) 9.0415 [8.343733555308, 9.746244]95749959]95

#> 4 A A arimases 2005 2005 N(9.2, 0.1612) 9.0115 [8.228413462905, 9.798851]95842362]95

#> 5 A A arimases 2006 2006 N(9.2, 0.1915) 89.9815 [8.132359381495, 9.836236]95923773]95

#> 6 A A arimases 2007 2007 N(9.2, 0.2119) 89.9615 [8.050547307893, 9.863163]95997374]95

#> 7 A A arimases 2008 N(8.9.2, 0.2422) 89.9315 [7[8.979837240208, 910.882527]95065059]95

#> 8 A A arimases 2009 N(8.9.2, 0.25) 89.9115 [7[8.918087177208, 910.896244]95128059]95

#> 9 A A arimases 2010 N(8.9.2, 0.2728) 89.8815 [7[8.863739118037, 910.905656]95187231]95

#> 10 A A arimases 2011 N(8.9.2, 0.2931) 89.8615 [7[8.815615062070, 910.911742]95243198]95

#> # … with 150230 more rows

Created on 2020-10-2224 by the reprex package (v0.3.0)