I am struggling to understand when a regression variable that is non-lagged would be beneficial to a forecasting algorithm.

I have been investigating the unobserved component model algorithm. I am finding that even when the non-lagged regression variable is linearly correlated with the response, a better model (lower cross-validated MASE) does not use the regression variable. It seems a 'slope' term within UCM could just as easily be used as the regression variable.

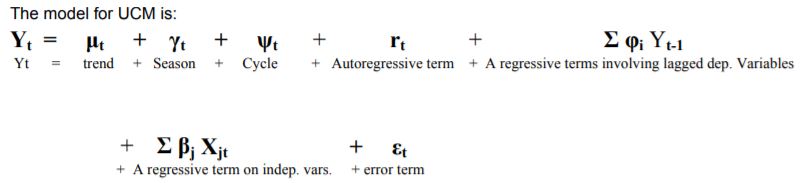

For UCM terms: https://www.lexjansen.com/nesug/nesug04/an/an03.pdf

I am also investigating ARIMA models. I am finding again that if the non-lagged regression variable is linearly correlated with the response that this same trend can be estimated just with an ARIMA model. For example, I could use a difference to de-trend the model so it's now stationary & the linear trend. A transfer function utilizing the correlated regression variable is correlated with is now goneno longer significant.

For ARIMA terms: https://v8doc.sas.com/sashtml/ets/chap7/sect8.htm#:~:text=Thus%2C%20the%20general%20notation%20for,order%20of%20the%20seasonal%20part.

ARIMA Model:

I guess the question boils down to, When is the regression variable explaining variation in the response that couldn't easily be estimated by terms expressed in lags of the response?".

Is there a simple guide during EDA of the y & x that I could use to try & identify patterns that a simple lagged y model could not explain?

Thank you in advance for your help, narnia649