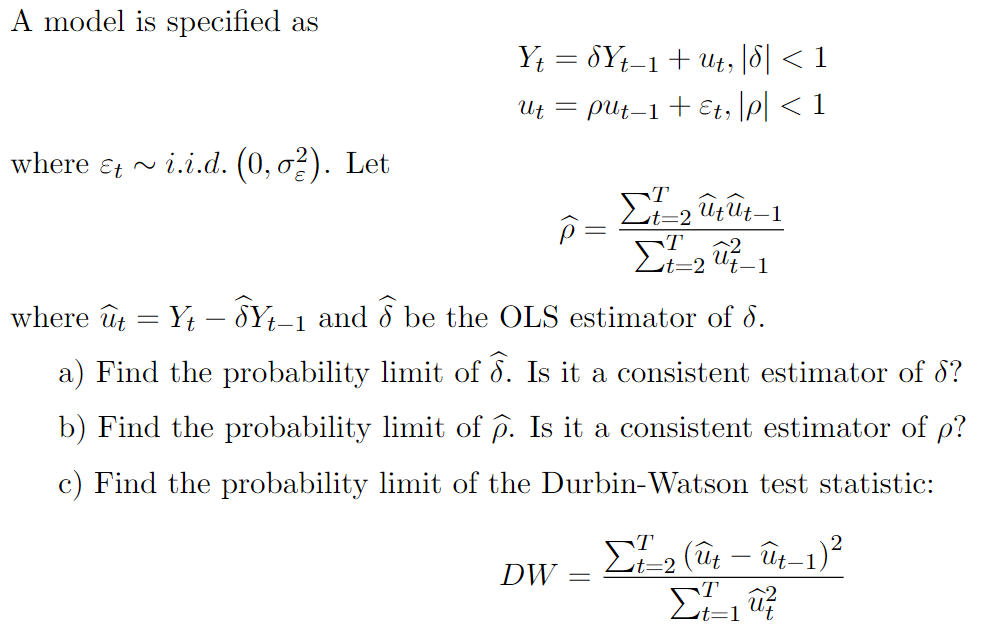

Given the model: \begin{aligned} Y_t &= \delta Y_{t-1}+u_t, \\ u_t &= \rho u_{t-1}+\epsilon_t, \end{aligned} where $\epsilon_t\sim i.i.d. (0,\sigma^2)$, $|\delta|,|\rho|<1$. Then how to find the prob. limit of the OLS estimator $\hat\delta$?

I have tried to use WLLN, since the $Y_t$ is not i.i.d., however the variance of $Y_t$ doesn't converge to 0. WLLN doesn't applies. So how to find the prob. limit of the OLS estimator $\hat\delta$?

Actually i calculated $\hat\delta$ directly using OLS estimator formula, and get \begin{equation} \hat\delta=\delta+\sum_{t=2}^T y_tu_{t-1}/\sum_{t=2}^Ty_{t-1}^2 \end{equation}. I wonder if i can expand $Y_t$ to infinite horizon to conclude $Y_t$ as covariance-stationary process or i can just expand $Y_t$ to finite horizon as $Y_t=\sum_{j=0}^{t-1}\delta^ju_{t-j}$. In order to use WLLN, I also used the above finite horizon expansion to calculate the $E(\sum_{t=2}^Ty_{t-1}^2/T-2)$ and find the probability limit is $\frac{(1+\rho \delta)\sigma^2}{(1-\rho \delta)(1-\delta^2)(1-\rho^2)}$. However, if i just consider the finite horizon expansion,then the fourth moment expection $E[(\sum_{t=2}^Ty_{t-1}^2/T-2)^2]$ is evidently doesn't converge to zero. So now i am quite confused. Is the OLS estimator $\hat\delta$ converge to some distribution in probability?

Thanksupdate: uploaded the full question

Thanks for everyone, i'd appreciate it if you can add your comment to this question.

Thanks for everyone, i'd appreciate it if you can add your comment to this question.