I am conducting an empirical study of the relation between earnings and returns.

I have an unbalanced panel with $N=449$ firms and $T=36$ time periods. Regarding the estimation methods I am confused:

- In most of the papers they account for firm clustering and time issues and therefore cluster for firms and introduce time-dummy variable using OLS.

=> Is that the simple pooled OLS?

If there are entity and time issues I thought that one should use the within (Fixed effects) or at least a weighted average of within and between (Random effects) estimator.

I have run some diagnostic test: a) the Hausman test favors the fixed effects b) the Breusch-Pagan Lagrange Multiplier (LM) favors the OLS over the Random Effects

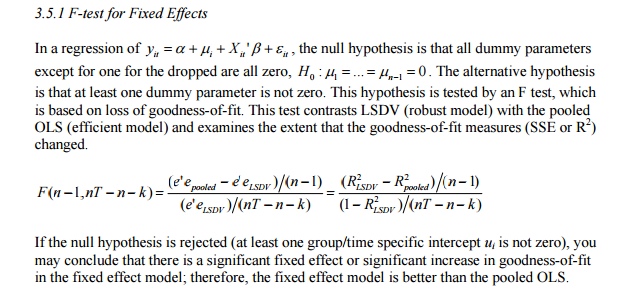

So the first question that appears is: How can I check pooled OLS vs Fixed Effects?

Additionally, my panel is unbalanced: firms in my panel might get bankrupt or merge with other companies. therefore, the question arises: In case of correlation of these pattern with the idiosyncratic errors, which is best to avoid biased estimtators?

The next issue regards Stata.I do not fully understand the difference of the following regressions:

1) reg y x i.time, cluster(id)

2) xtreg y x i.time, fe cluster(id) dfadj

3) xtreg y x i.time, re cluster(id)

Is the only difference the used estimator?

In most of the studies version 1) is used although I do not really get the advantage of version 1) over 2) or 3).

In which case is pooled OLS preferred over the other methods? I´ve noticed that the SE are largest when fixing for firm and time using the fe-estimator.

And the last question arises: If there are unobserved effects - firm and time: how can I determine if these effects are permanent or temporary (die away over time)?

Important for me is to get an inference robust result.