I am doing my project on forecasting and due to I have limited knowledge in ARIMA, I would like to ask what is the appropriate ARIMA model for these two data. Both data are monthly.

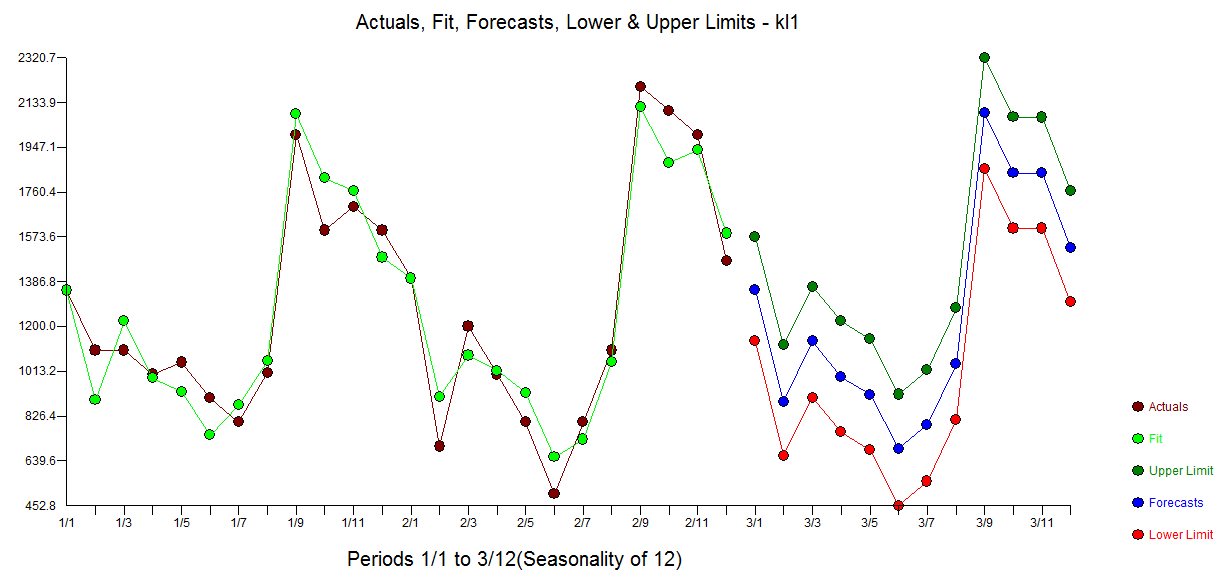

Figure 1

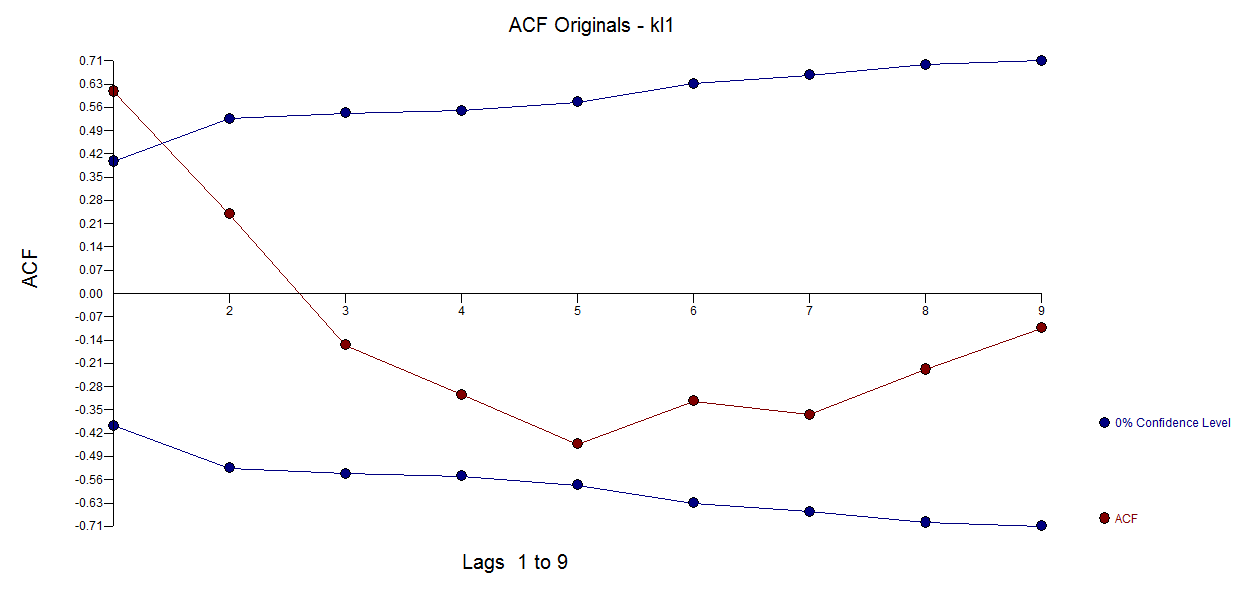

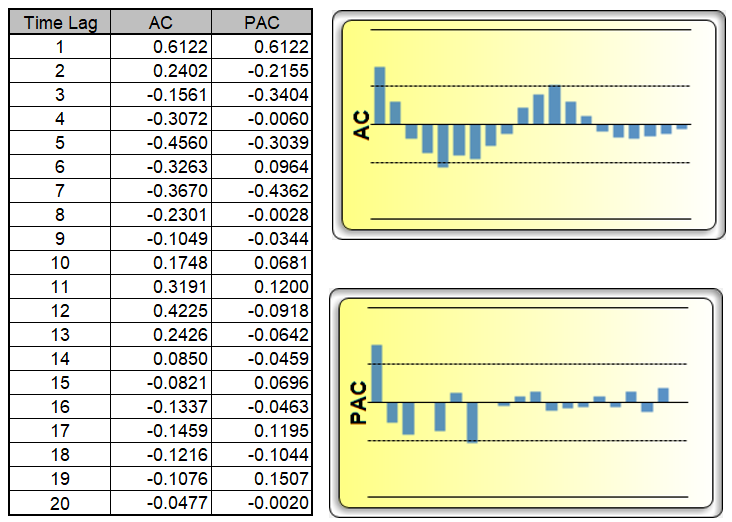

The first data is shown above, i differenced the data once due to stationary problems (as it cuts off slowly, CMIIW), thus the result of differencing is shown below

Figure 2

I have found that the data is under 0.05 on lag 1 and 2. Does it mean that there are 4 available ARIMA model for this data [(1,1,0), (0,1,1), (2,1,0) and (0,1,2)]? I also tried to use ARIMA(1,1,1) but failed since the solution do not converge.

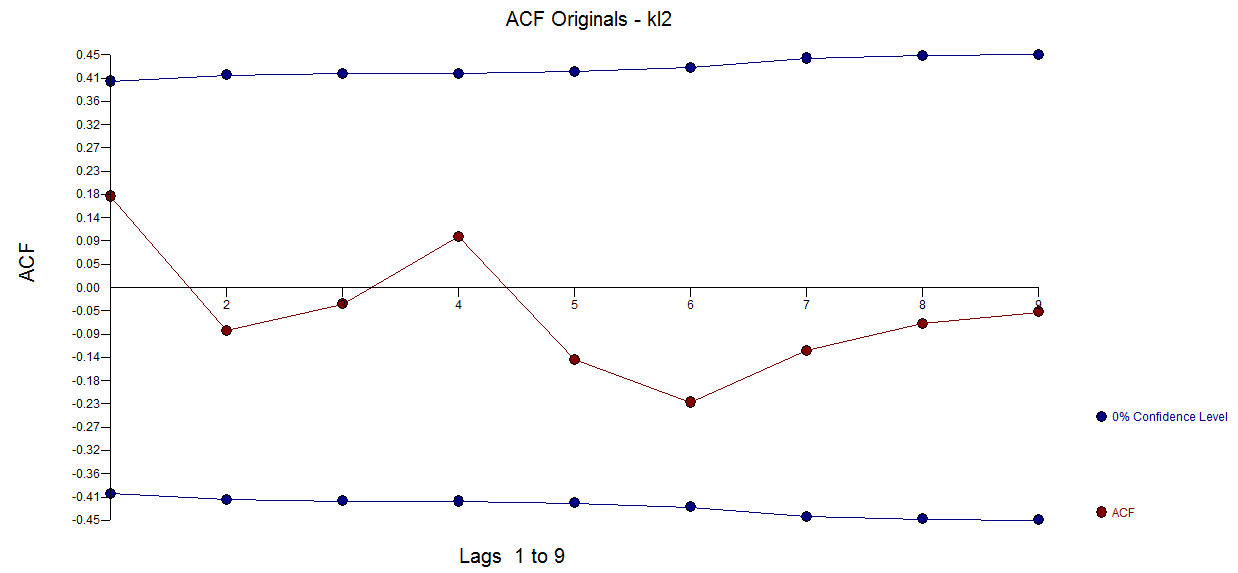

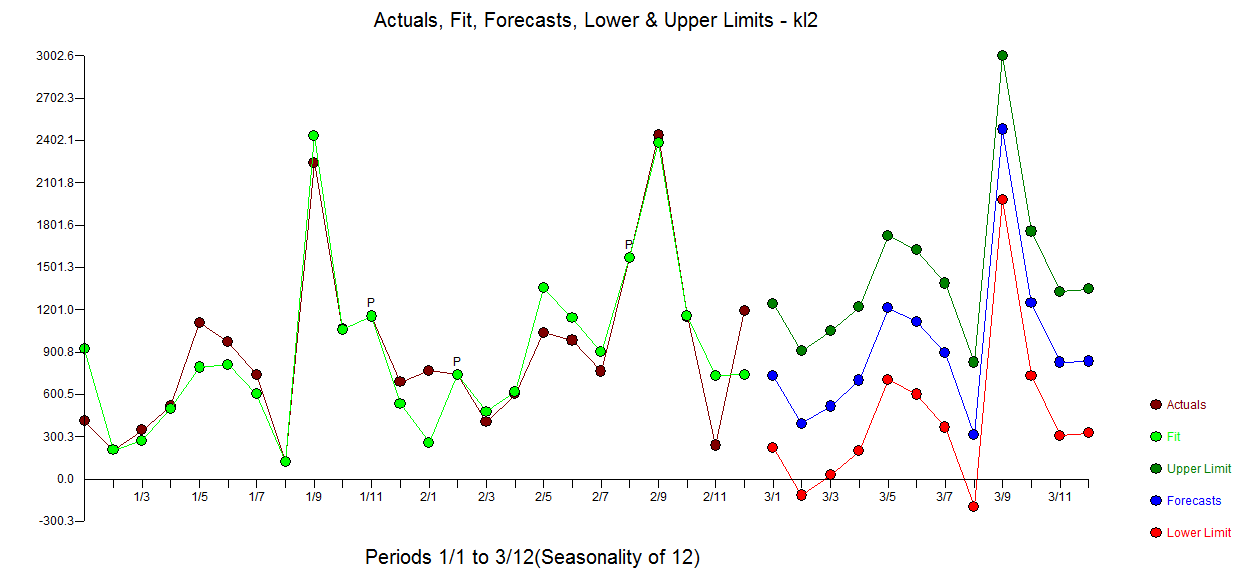

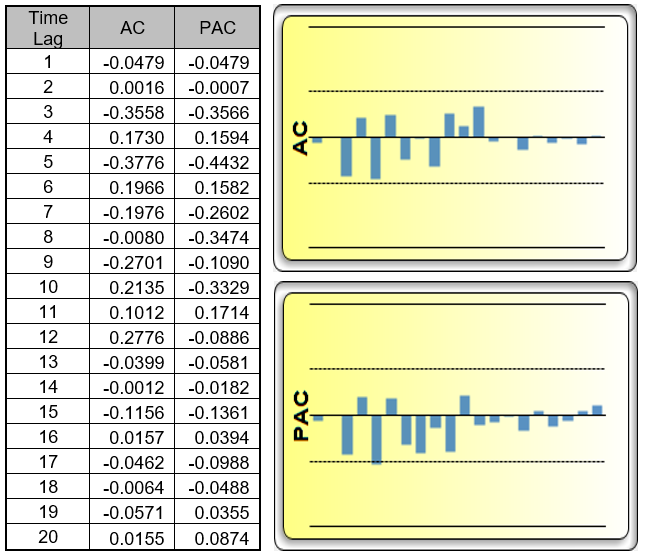

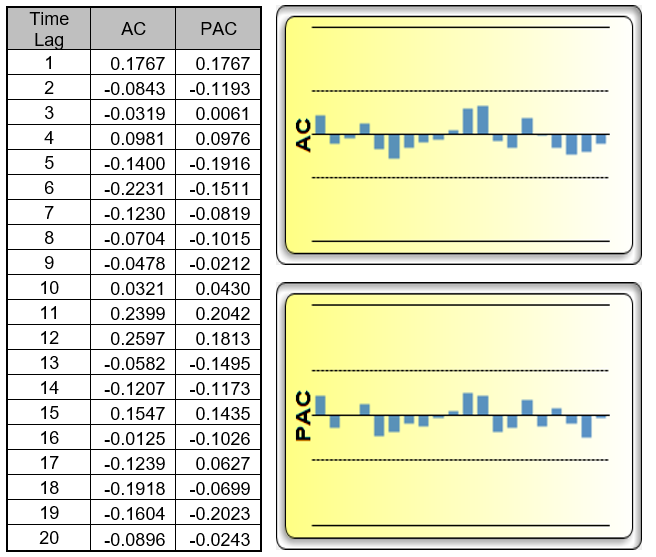

Another one is another data below without differencing (different training data), i found that both ACF and PACF cuts off at lag 3 (with 95% confidence level). Thus are ARIMA(2,0,0) and ARIMA (0,0,2) applicable for this or do i need to do differencing first? The reason i am putting MA(2) and/or AR (2) is that some resources found that the sum of p & q should not exceed 2 to prevent overfitting the model.

Figure 3

Thank you very much for your help :D