I have 30 pairs of observations $(x_i, y_i)$ and hypothesize that in the observed range of $x$ a non-monotone relationship $y_i = f(x_i) + \epsilon$ may hold. I am willing to assume that $\text{Var}(\epsilon | x_i) =\sigma^2$.

I am interested in

- Testing if $f(x_i)$ is non-monotone, and if I reject monotonicity then

- Estimating $ x^* = \text{argmin} f(x)$.

Approach so far

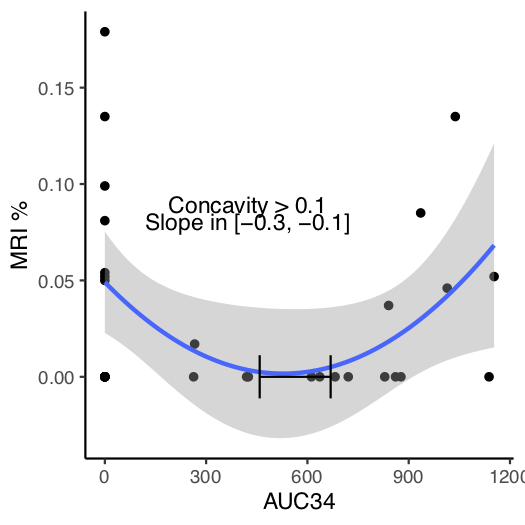

My approach has been to use linear regression with a quadratic basis expansion of $x$ thus $$ E(Y|x) = a + bx + cx^2, $$ and then conduct inference on $\hat c$ and $\hat x^* = -\hat{b}/(2\hat{c})$ . If $\hat c>0$, and $\hat x^* = -\hat{b}/(2\hat{c})$ lies in the range of the observed data with 95% confidence, I conclude that $f$ is concave and that a sign change in the derivative of $f$ occurred. For $\hat x^*$ I am using the bootstrap, since the delta-method doesn't seem reliable for a ratio of estimators. In the figure below, see an example of such a quadratic fit and the 95% confidence interval on $x^*$, a one-sided CI on $c$, and a 95% CI on $b$, which gives the slope at $x=0$ if the quadratic model holds.

Questions

I am looking for references to a principled treatment of this problem (maybe in response surface modeling?) I am nervous about inventing a wheel here.

Although I doubt I can do more than fit a quadratic since I only have 30 data points, there is something alarming about assuming a polynomial holds. I am vaguely aware of non-parametric convex regression, could it be used somehow here?

f(assuming its regular enough). And you can use any base to do your estimation (here you use polynomial, it could be any functional base, as long as you have few parameter to estimate this is not a problem). I don't have time to dig further, but i can say one last important thing. Its always better to directly estimate what we want to estimate and not do multiple estimation step, its less precise and hide many problems. $\endgroup$