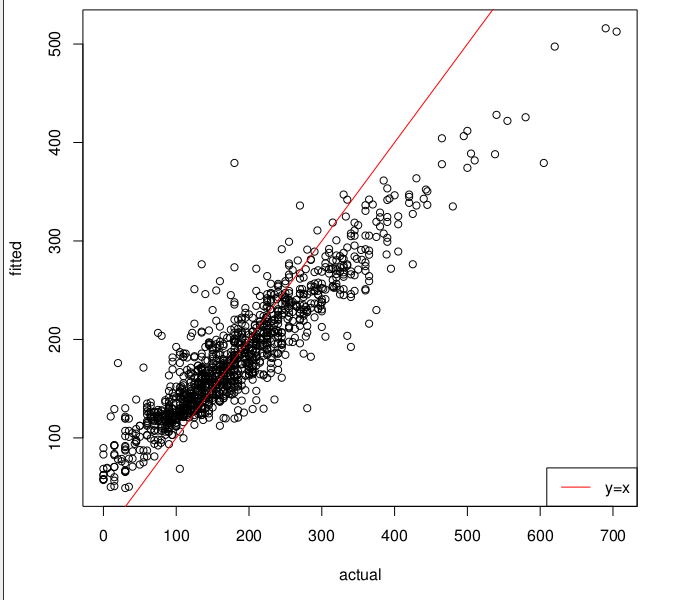

I have often found in practice, using nonlinear regression techniques such as feedforward neural nets or random forests, that the resulting actual-vs-fitted plot (on training set) seems obviously sub-optimal, eg. like this:

Here the model under-estimates high values of $y$, and under-estimates low values. It would seem natural to me "shift" these predictions using linear regression of the observed $y$ over the predicted $y$:

I'd first run a nonlinear regression model, and obtain a first training-set prediction $\hat y_{train} = f(X_{train})$

then I'd run a linear regression of $y_{train}$ on $\hat y_{train}$, and get $y_{train} = \hat a + \hat b \times \hat y_{train} + \hat \epsilon$

then for any prediction set $X_{test}$, I'd output a re-scaled prediction: $\hat y_{test} = \hat a + \hat b \times f(X_{test})$.

It seems obvious that this yields lower error on the training set, but does anyone know whether it hurts generalization error?