In fact you can prove it's not actually exponential, almost trivially:

Compute the probability that a given share is greater than $500$ million. Compare with the probability that an exponential random variable is greater than $500$ million.

However, it's not too hard to see that for your uniform-gap example that it should be close to exponential.

Consider a Poisson process - where events occur at random over along some dimension. The number of events per unit of the interval has a Poisson distribution, and the gap between events is exponential.

If you take a fixed interval then the events in a Poisson process that fall within it are uniformly distributed in the interval. See here.

[However, note that because the interval is finite, you simply can't observe larger gaps than the interval length, and gaps nearly that large will be unlikely (consider, for example, in a unit interval - if you see gaps of 0.04 and 0.01, the next gap you see can't be bigger than 0.95).]

So apart from the effect of restricting attention to a fixed interval on the distribution of the gaps (which will reduce for large $n$, the number of points in the interval), you would expect those gaps to be exponentially distributed.

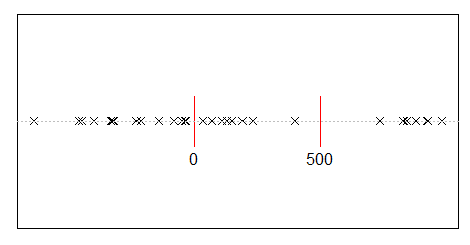

Now in your code, you're dividing the unit interval by placing uniforms and then finding the gaps in successive order statistics. Here the unit interval is not time or space but represents a dimension of money (imagine the money as 50000 million cents laid out end to end, and call the distance they cover the unit interval; except here we can have fractions of a cent); we lay down $n$ marks, and that divides the interval into $n+1$ "shares". Because of the connection between the Poisson process and uniform points in an interval, the gaps in the order statistics of a uniform will tend to look exponential, as long as $n$ is not too small.

More specifically, any gap that starts in the interval placed over the Poisson process has a chance to be "censored" (effectively, cut shorter than it would otherwise have been) by running into the end of the interval.

$\hspace{1cm}$

Longer gaps are more likely to do that than shorter ones, and more gaps in the interval means the average gap length must go down -- more short gaps. This tendency to be 'cut off' will tend to affect the distribution of longer gaps more than short ones (and there's no chance any gap limited to the interval will exceed the length of the interval -- so the distribution of gap size should decrease smoothly to zero at the size of the whole interval).

In the diagram, a longish interval at the end has been cut shorter, and a relatively shorter interval at the start is also shorter. These effects bias us away from exponentiality.

(The actual distribution of the gaps between $n$ uniform order statistics is Beta(1,n). )

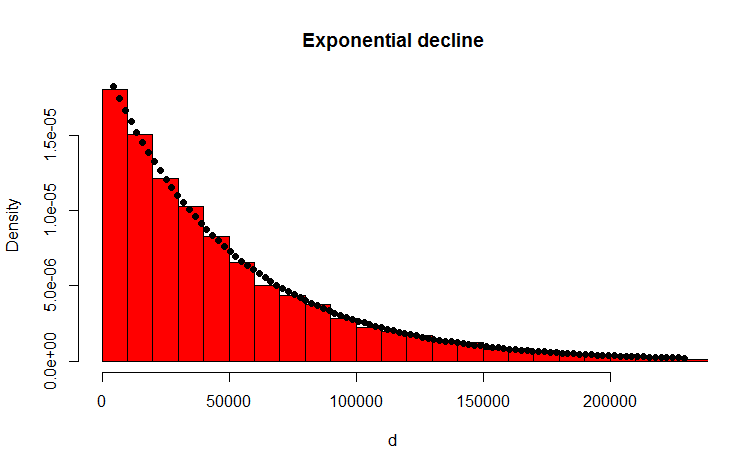

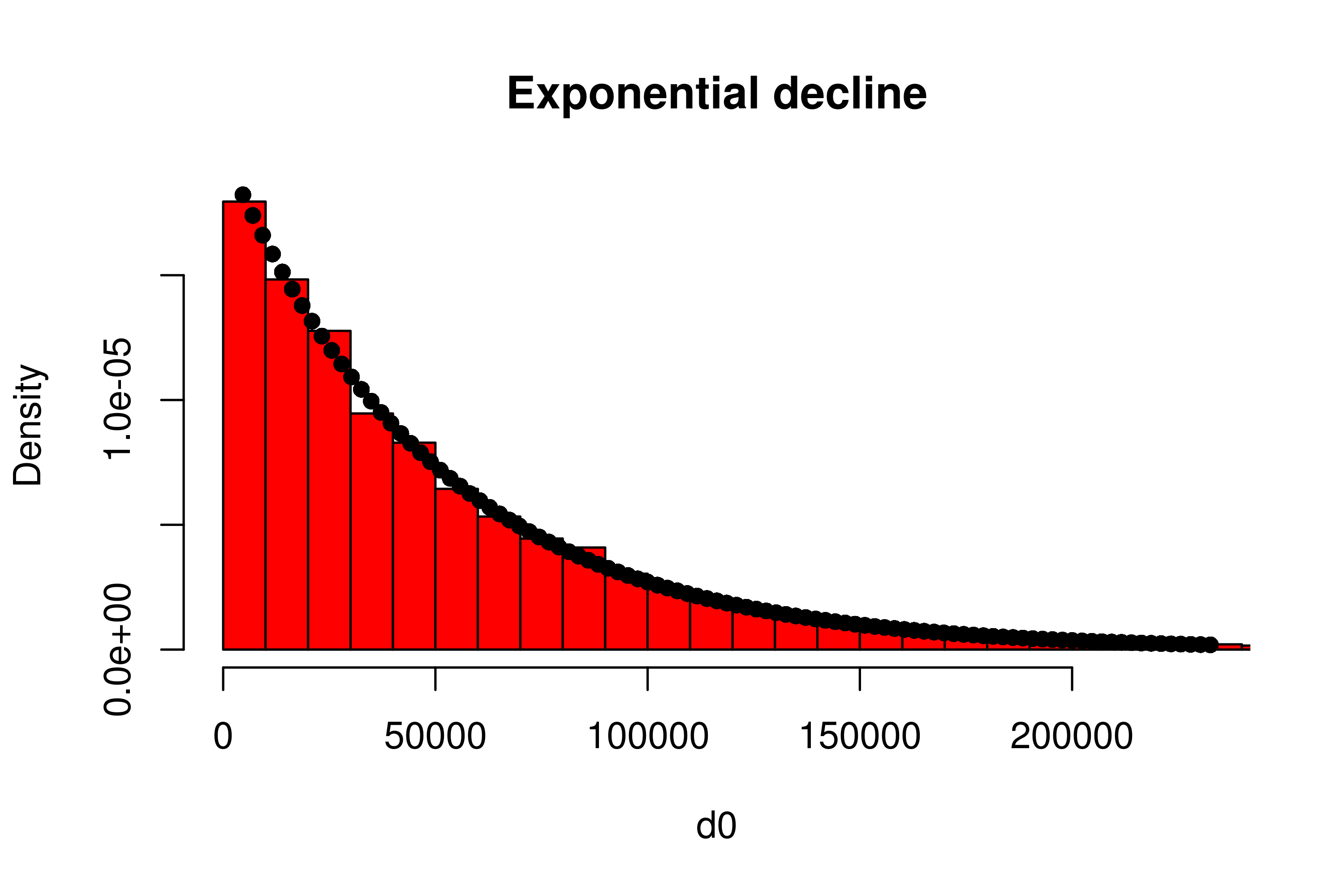

So we should see the distribution at large $n$ look exponential in the small values, and then less exponential at the larger values, since the density at its largest values will drop off more quickly.

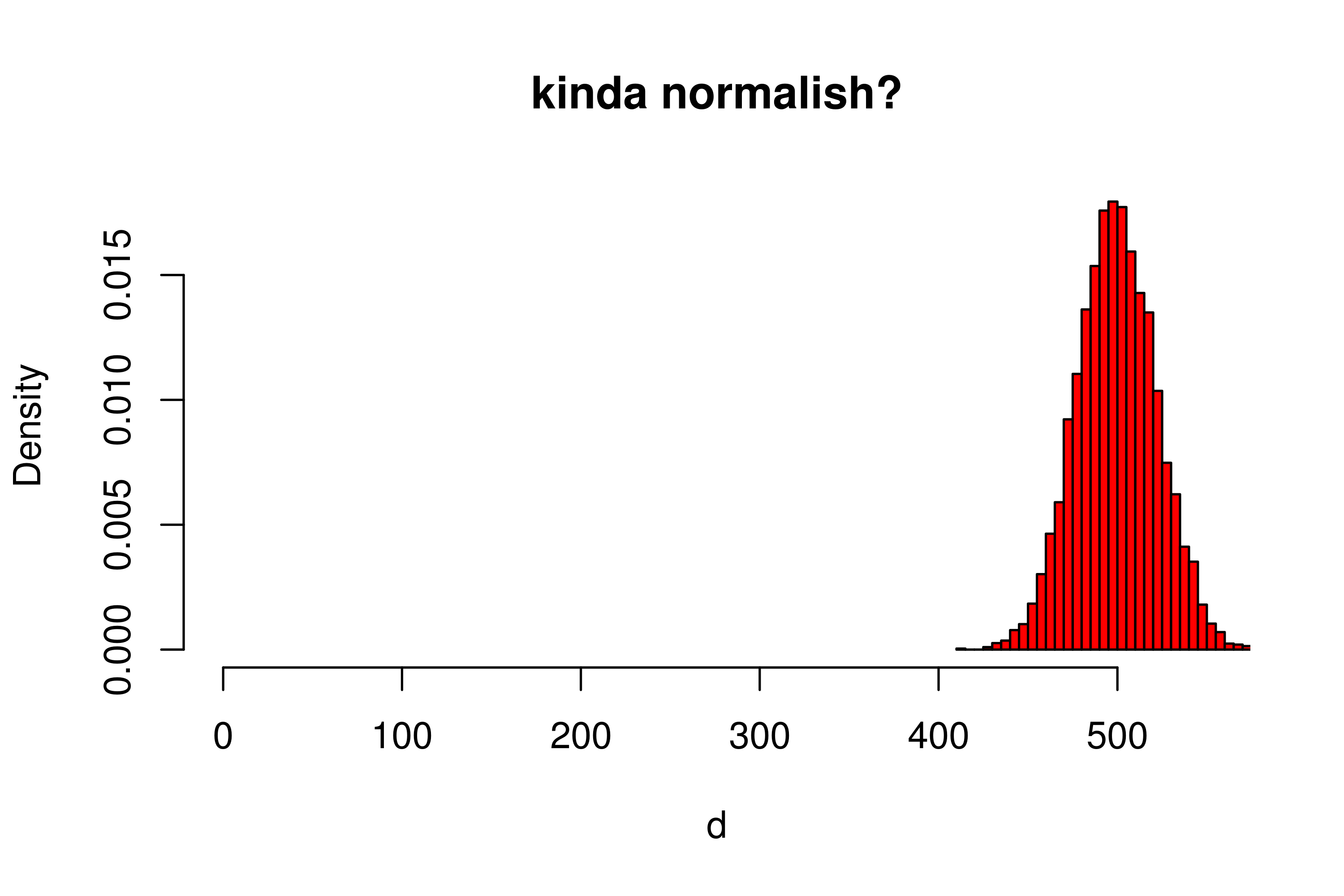

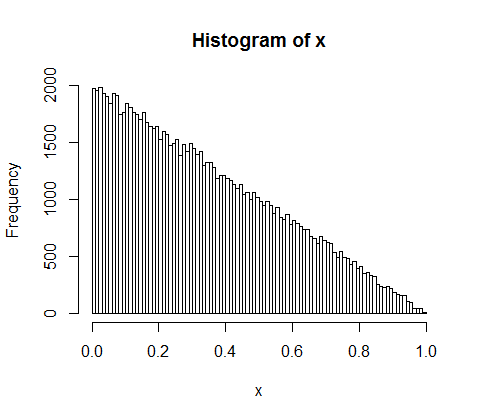

Here's a simulation of the distribution of gaps for n=2:

Not very exponential.

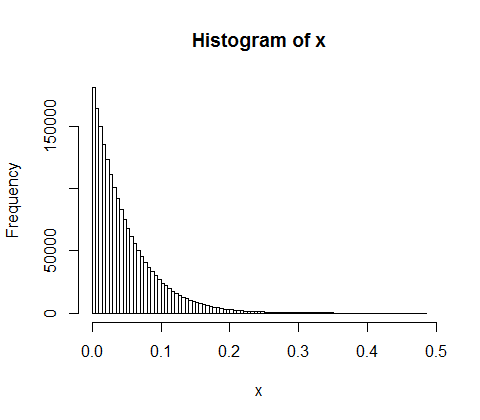

But for n=20, it starts to look pretty close; in fact as $n$ grows large it will be well approximated by an exponential with mean $\frac{1}{n+1}$.

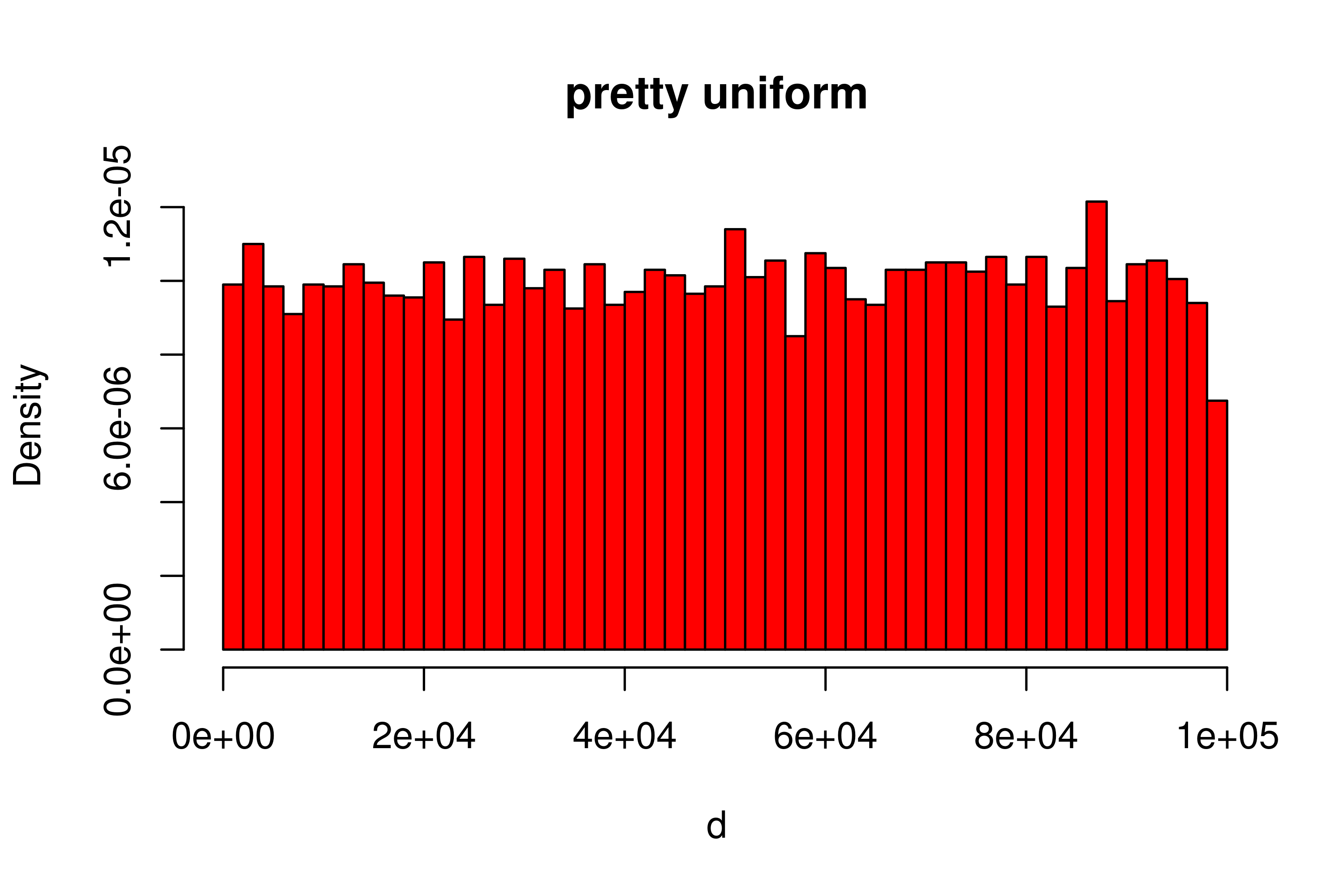

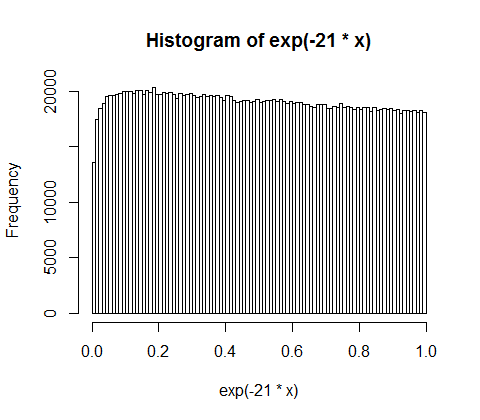

If that was actually exponential with mean 1/21, then $\exp(-21x)$ would be uniform... but we can see it isn't, quite:

The non-uniformity in the low values there corresponds to large values of the gaps -- which we'd expect from teh above discussion, because the effect of the "cutting off" the Poisson process to a finite interval means we don't see the largest gaps. But as you take more and more values, that goes further out into the tail, and so the result starts to look more nearly uniform. At $n=10000$, the equivalent display would be harder to distinguish from uniform - the gaps (representing shares of the money) should be very close to exponentially distributed except at the very unlikely, very very largest values.