Here is an alternative derivation which I find quite intuitive using summations rather than matrix notation. Notation is similar to Stanford CS229 notation with $m$ observations, $n$ features, superscript $(i)$ for the $i$'th observation, subscript $j$ for the $j$'th feature.

Lasso cost function

\begin{aligned}

RSS^{lasso}(\theta) & = RSS^{OLS}(\theta) + \lambda \Vert \theta \Vert_1

\\

&= \frac{1}{2} \sum_{i=1}^m \left[y^{(i)} - \sum_{j=0}^n \theta_j x_j^{(i)}\right]^2 + \lambda \sum_{j=1}^n |\theta_j|

\end{aligned}

Focus on the OLS term

\begin{aligned}

\frac{\partial }{\partial \theta_j} RSS^{OLS}(\theta) & = - \sum_{i=1}^m x_j^{(i)} \left[y^{(i)} - \sum_{j=0}^n \theta_j x_j^{(i)}\right]

\\

& = - \sum_{i=1}^m x_j^{(i)} \left[y^{(i)} - \sum_{k \neq j}^n \theta_k x_k^{(i)} - \theta_j x_j^{(i)}\right]

\\

& = - \sum_{i=1}^m x_j^{(i)} \left[y^{(i)} - \sum_{k \neq j}^n \theta_k x_k^{(i)} \right] + \theta_j \sum_{i=1}^m (x_j^{(i)})^2

\\

& \triangleq - \rho_j + \theta_j z_j

\end{aligned}

where we define $\rho_j$ and the normalizing constant $z_j$ for notational simplicity

Focus on the $L_1$ term

The problem with this term is that the derivative of the absolute function is undefined at $\theta = 0$. The method of coordinate descent makes use of two techniques which are to

- Perform coordinate-wise optimization, which means that at each step only one feature is considered and all others are treated as constants

- Make use of subderivatives and subdifferentials which are extensions of the notions of derivative for non differentiable functions.

The combination of these two points is important because in general, the subdifferential approach to the Lasso regression does not have a closed form solution in the multivariate case. Except for the special case of orthogonal features which is discussed here.

As we did previously for the OLS term, the coordinate descent allows us to isolate the $\theta_j$:

$$ \lambda \sum_{j=1}^n |\theta_j| = \lambda |\theta_j| + \lambda \sum_{k\neq j}^n |\theta_k|$$

And optimizing this equation as a function of $\theta_j$ reduces it to a univariate problem.

Using the definition of the subdifferential as a non empty, closed interval $[a,b]$ where $a$ and $b$ are the one sided limits of the derivative we get the following equation for the subdifferential $\partial_{theta_j} \lambda |\theta|_1$

\begin{equation}

\partial_{\theta_j} \lambda \sum_{j=1}^n |\theta_j| = \partial_{\theta_j} \lambda |\theta_j|=

\begin{cases}

\{ - \lambda \} & \text{if}\ \theta_j < 0 \\

[ - \lambda , \lambda ] & \text{if}\ \theta_j = 0 \\

\{ \lambda \} & \text{if}\ \theta_j > 0

\end{cases}

\end{equation}

Putting it together

Returning to the complete Lasso cost function which is convex and non differentiable (as both the OLS and the absolute function are convex)

$$ RSS^{lasso}(\theta) = RSS^{OLS}(\theta) + \lambda || \theta ||_1 \triangleq f(\theta) + g(\theta)$$

We now make use of three important properties of subdifferential theory (see wikipedia)

A convex function is differentiable at a point $x_0$ if and only if the subdifferential set is made up of only one point, which is the derivative at $x_0$

Moreau-Rockafellar theorem: If $f$ and $g$ are both convex functions with subdifferentials $\partial f$ and $\partial g$ then the subdifferential of $f + g$ is $\partial(f + g) = \partial f + \partial g$.

Stationary condition: A point $x_0$ is the global minimum of a convex function $f$ if and only if the zero is contained in the subdifferential

Computing the subdifferential of the Lasso cost function and equating to zero to find the minimum:

\begin{aligned}

\partial_{\theta_j} RSS^{lasso}(\theta) &= \partial_{\theta_j} RSS^{OLS}(\theta) + \partial_{\theta_j} \lambda || \theta ||_1

\\

0 & = -\rho_j + \theta_j z_j + \partial_{\theta_j} \lambda || \theta_j ||

\\

0 & = \begin{cases}

-\rho_j + \theta_j z_j - \lambda & \text{if}\ \theta_j < 0 \\

[-\rho_j - \lambda ,-\rho_j + \lambda ] & \text{if}\ \theta_j = 0 \\

-\rho_j + \theta_j z_j + \lambda & \text{if}\ \theta_j > 0

\end{cases}

\end{aligned}

For the second case we must ensure that the closed interval contains the zero so that $\theta_j = 0$ is a global minimum

\begin{aligned}

0 \in [-\rho_j - \lambda ,-\rho_j + \lambda ]

\\

-\rho_j - \lambda \leq 0

\\

-\rho_j +\lambda \geq 0

\\

- \lambda \leq \rho_j \leq \lambda

\end{aligned}

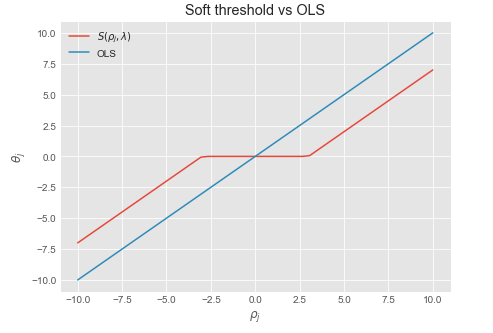

Solving for $\theta_j$ for the first and third case and combining with above:

\begin{aligned}

\begin{cases}

\theta_j = \frac{\rho_j + \lambda}{z_j} & \text{for} \ \rho_j < - \lambda \\

\theta_j = 0 & \text{for} \ - \lambda \leq \rho_j \leq \lambda \\

\theta_j = \frac{\rho_j - \lambda}{z_j} & \text{for} \ \rho_j > \lambda

\end{cases}

\end{aligned}

We recognize this as the soft thresholding function $\frac{1}{z_j} S(\rho_j , \lambda)$ where $\frac{1}{z_j}$ is a normalizing constant which is equal to $1$ when the data is normalized.

Coordinate descent update rule:

Repeat until convergence or max number of iterations:

- For $j = 0,1,...,n$

- Compute $\rho_j = \sum_{i=1}^m x_j^{(i)} (y^{(i)} - \sum_{k \neq j}^n \theta_k x_k^{(i)} ]$

- Compute $z_j = \sum_{i=1}^m (x_j^{(i)})^2$

- Set $\theta_j = \frac{1}{z_j} S(\rho_j, \lambda)$

Soft threshold function

Sources:

{kind=link}