I would like to know how to find out the analytical solution of a simple linear regression with fixed intercept = 0:

$$ s = e^{-ht}$$ $$ y = -ln(s) = h\cdot t$$

Here ist the background: I have three survival probabilities $s$ at 30, 90 and 180 days. Obviously, I have at day = 0 100% survival, so I include this observation. I know that this is contested (here) but I think in this special case it makes sense. The data I use for fitting the linear regression:

> obs

t s y

1 0 1.00 0.00000000

2 30 0.98 0.02020271

3 90 0.90 0.10536052

4 180 0.80 0.22314355

If I fit with simple regression I get this:

> (fit1 <- lm(y~t, data=obs))

Call:

lm(formula = y ~ t, data = obs)

Coefficients:

(Intercept) t

-0.008464 0.001275

This can be obtained analytically if the following function is derived:

$$f(h) = \sum (y_i - ht_i)^2$$

which gives:

$$ \frac{\sum (y_i-\bar{y})\cdot (t_i-\bar{t})}{\sum (t_i-\bar{t})^2}$$

UPDATE 1: This is the result of the minimization of $$f(h) = \sum (y_i - c - ht_i)^2$$. The correct result (see answers): $$ \frac{\sum (y_i\cdot t_i)}{\sum t_i^2}$$

The analytical results is:

yc <- with(obs,y-mean(y))

tc <- with(obs, t - mean(t))

sum(yc*tc)/sum(tc^2)

[1] 0.001275204

The same as coefficient in the fit1. Now, if I fix intercept to intercept=0 I get this:

> (fit2 <- lm(y~0+t, data=obs))

Call:

lm(formula = y ~ 0 + t, data = obs)

Coefficients:

t

0.001214

I'm wondering how I can get an analytical solution for this. How I have to consider the fix intercept in the function $f(h)$ above?

Any idea is appreciated.

Here is the way I constructed the data:

set.seed(123)

# Hazard ratio

h <- 0.7

# Number of observation

n <- 50

# Model: exponential

t <- rexp(n,h)

# scale to days

t <- t*365.25

hist(t)

t <- sort(t)

# Put data into a dataframe

df0 <- data.frame(t=t)

head(df0)

# Compute probablities

df0$s <- 1 - c(1:n)/n

head(df0)

# Extract survival probabilities at 30,90 and 180 days

df0$t2 <- ceiling(df0$t/30)*30

# Select survival probablity 30, 90, 180 days

library(sqldf)

obs <- sqldf("SELECT t2 t, MAX(s) s FROM df0 WHERE t2 IN (30,90,180) GROUP BY t2")

# Add survival probability=1 at day 0

obs <- rbind(data.frame(t = 0, s = 1), obs)

# s = e^(-ht) => y = -ln(s) = h*t

obs$y <- -log(obs$s)

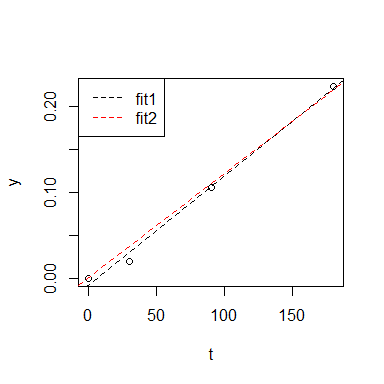

plot(y~t, data=obs)

fit1 <- lm(y~t, data=obs)

abline(fit1,lty=2)

fit2 <- lm(y~0+t, data=obs)

abline(fit2,lty=2, col="red")

legend("topleft", legend=c("fit1","fit2"), col=c(1,2), lty=c(2,2))