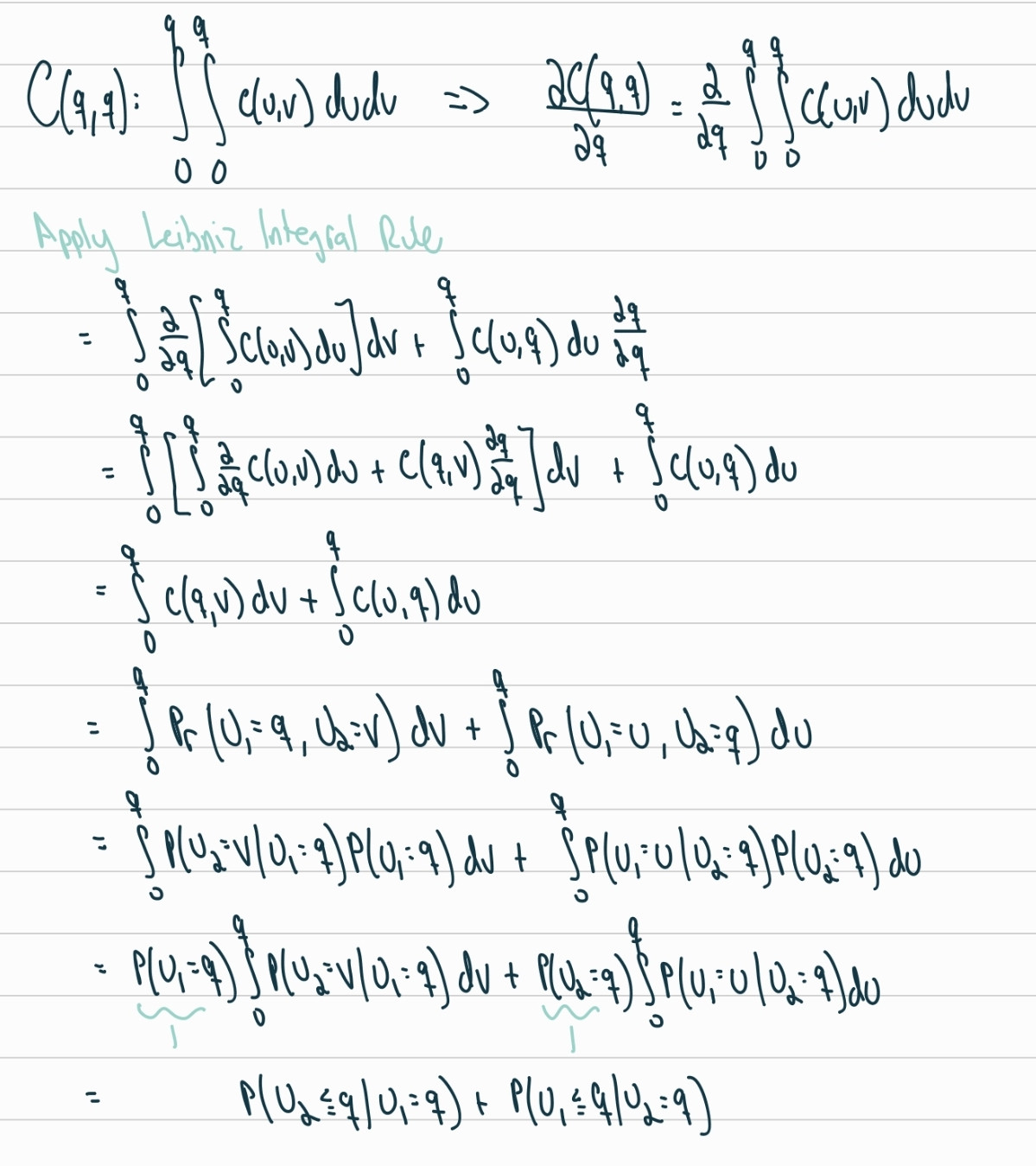

Consider a bivariate Gaussian copula $C(\cdot)$.

Because of the radial symmetry of a Gaussian copula we can consider just the lower tail dependence. We know that the lower tail dependence for this copula is:

$$\begin{align}

\lambda&=\lim_{\,\,q\to 0^{+}} \frac{\partial C(q,q)}{\partial q}\\

&=\lim_{\,\,q\to 0^{+}} \text{Pr}(U_{2}\leq q\,|\,U_{1}=q)+ \lim_{\,\,q\to 0^{+}} \text{Pr}(U_{1}\leq q\,|\,U_{2}=q)

\end{align}$$

Since a Gaussian copula is exchangeable, it follows that:

$$\lambda=2\lim_{\,\,q\to 0^{+}}\text{Pr}(U_{2}\leq q\,|\,U_{1}=q)$$

Now, let:

$$(X_{1},X_{2}):=\Big(\Phi^{-1}(U_{1}),\,\Phi^{-1}(U_{2})\Big)$$

This means that $(X_{1},X_{2})$ has a bivariate normal distribution with standard marginals and correlation $\rho$. Now:

$$\begin{align}

\lambda&=2\lim_{\,\,q\to 0^{+}}\text{Pr}(\Phi^{-1}(U_{2})\leq \Phi^{-1}(q)\,|\,\Phi^{-1}(U_{1})=\Phi^{-1}(q))\\

&=2\lim_{x\to -\infty}\text{Pr}(X_{2}\leq x\,|\, X_{1}=x)

\end{align}$$

Finally, we know that $X_{2}\,|\,X_{1}\sim N(\rho x,1-\rho^{2})$, so:

$$\lambda=2\lim_{x\to -\infty}\Phi\Bigg(x\sqrt{\frac{(1-\rho)}{(1

+\rho)}}\Bigg)=0$$